Housing Market Correction: Why Sellers Are Staying Put

The housing market is currently undergoing a correction, not a crash, according to recent data. Inventory levels are flat or declining as sellers hold back, indicating a rational market response rather than panic. Delinquency rates remain below pre-pandemic levels, suggesting widespread financial distress is not imminent.

Housing Market Correction: Sellers Hold Back, Inventory Stays Low

The current housing market is not heading for a crash, but rather a correction. This means prices might not drop dramatically, but the market will adjust. Understanding this difference is key for buyers and sellers navigating today’s real estate.

The number of homes for sale, known as inventory, is a crucial indicator. It has remained flat over the past year and might even decrease.

This is because sellers are not rushing to list their homes. They are waiting for better selling conditions instead of accepting lower prices.

Why Inventory Levels Matter

A housing crash typically happens when there are many more homes for sale than people want to buy. This oversupply forces sellers to lower their prices significantly. However, the current low inventory shows sellers are acting cautiously.

Sellers are behaving rationally in this market. They are choosing not to sell if they cannot get a good price. This is a clear sign of a correction, not a panic-driven sell-off.

Delinquency Rates Offer Clues

Another important metric is the delinquency rate. This tracks how many homeowners are struggling to make their mortgage payments. These homeowners might be forced to sell or face foreclosure.

Current delinquency rates are close to, but still below, pre-pandemic levels. This suggests that widespread financial distress among homeowners is not an immediate threat. There isn’t a large group of people being forced to sell their homes at any moment.

Correction vs. Crash: What’s the Difference?

A housing crash is a sudden, sharp drop in home prices. This usually happens due to economic collapse or a flood of foreclosures. A correction, on the other hand, is a more gradual adjustment in prices and market activity.

In a correction, the market finds a new balance. Prices might stabilize or see modest declines.

Inventory levels typically stay low as sellers wait for better times. This is the scenario the data currently supports.

Regional Market Variations

While the overall trend points to a correction, different regions may experience unique market conditions. Some areas with high demand might see prices hold steady or even rise slightly. Other areas with less demand could experience minor price decreases.

Buyers in high-demand areas might face continued competition. Sellers in these markets could still achieve good prices. Buyers in slower markets might find more options and less competition.

Economic Factors at Play

Broader economic conditions influence the housing market significantly. Factors like interest rates, job growth, and inflation all play a role. Higher interest rates can make mortgages more expensive, affecting buyer demand.

Stable job growth supports housing demand. Inflation can impact the cost of building new homes and overall affordability. Policymakers’ actions also influence the economic environment.

What This Means for You

For potential buyers, a correction means patience may be rewarded. You might find more homes to choose from over time. However, waiting too long could mean facing slightly higher prices if demand picks up.

For sellers, it’s important to have realistic expectations. If you need to sell, focus on making your home attractive to buyers. Consider current market values rather than hoping for peak pandemic prices.

Looking Ahead

The data suggests the housing market is adjusting, not collapsing. Inventory levels remain tight, and homeowner distress is low. Keep an eye on delinquency rates and overall economic health for future market shifts.

The next official housing market report is scheduled for release in early July.

Source: 2026 Housing Market Explained in 90 Seconds 🏡 (YouTube)

Related Articles

War Fuels Inflation, Squeezes Housing Market

Geopolitical conflict has driven inflation up, pushing mortgage rates higher and signaling a slowdown in the housing market. While a crash is unlikely, savvy investors can find opportunities by focusing on cash flow and buying below market value.

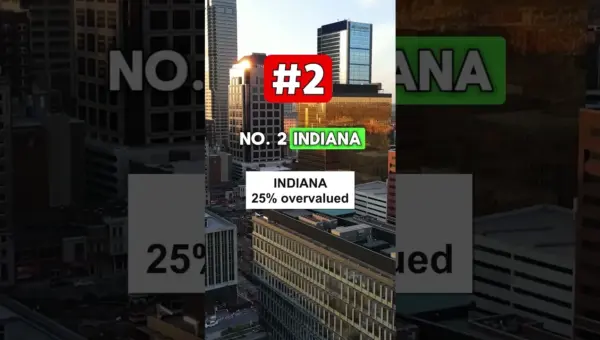

Top States Show Housing Bubble Risk

Several states show significant housing overvaluation in 2026, with home prices far exceeding local incomes. New Hampshire, Indiana, and Michigan are among the most overvalued markets, signaling potential price corrections. This trend highlights the importance of income-price balance for market stability.

Rent vs. Buy: New Data Reveals Shifting Housing Landscape

Recent financial analysis indicates that renting may be more financially advantageous than buying a home in 2026, challenging the traditional American dream. Rising costs and interest rates have widened the gap between homeownership and rental expenses.