Savings Rate Crucial for Early Retirement

The percentage of income saved each month, known as the savings rate, is the most critical factor determining financial independence and retirement timing. Consistently saving a higher portion of income, even with lower investment returns, can lead to greater wealth and earlier retirement compared to lower savings rates with higher returns. Addressing lifestyle creep and creating financial margin are key to increasing savings.

Savings Rate Crucial for Early Retirement

Two individuals, earning the same salary and working in the same city, can experience vastly different financial outcomes by retirement. One may achieve financial independence by age 55, while the other might still be working at 75 out of necessity, not desire.

This divergence isn’t due to higher income, better investment returns, luck, or market timing. Instead, it hinges on a single, recurring decision made consistently throughout their careers: their savings rate.

The percentage of income saved and invested each month is the most critical decision impacting financial well-being. It determines the size of your ‘army of dollar bills’ that works for you through compound growth. A higher savings rate not only leads to greater wealth but also significantly shortens the timeline to financial independence.

Comparing Savings Strategies

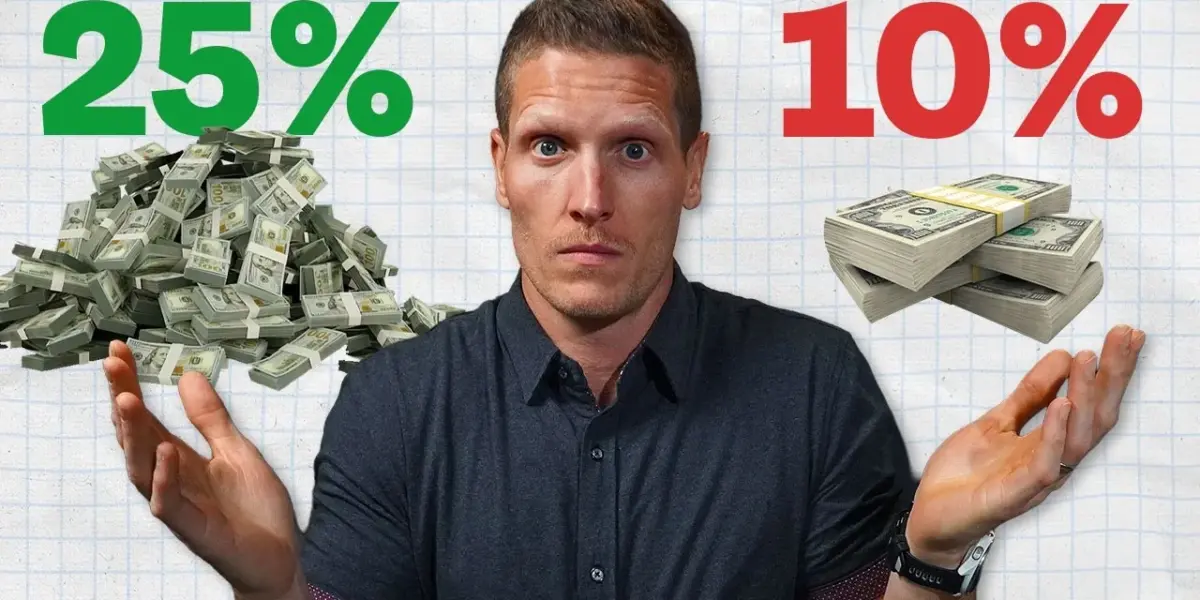

Consider two hypothetical individuals, Manny the Mutant and Average Alan, both earning $100,000 annually. Average Alan saves 10% of his income and achieves an impressive 10% average annual return. Over 30 years, Alan accumulates $1.8 million.

Manny the Mutant, however, saves 25% of his income but earns a more modest 6% average annual return. Despite lower investment returns, Manny’s higher savings rate allows him to amass over $2 million in the same 30-year period. Manny reached the $1 million milestone four years earlier than Alan, demonstrating how a higher savings rate accelerates the path to financial freedom.

The core lesson is clear: you can overcome lower investment returns with a higher savings rate, but a poor savings rate cannot be compensated for by high returns.

No investment strategy, however complex, can replace the foundational need for adequate savings. Compounding growth requires a base amount to work with. A low savings rate not only costs you potential wealth but also valuable time, potentially forcing you to work longer than planned.

Retirement Timeline Decisions

Every major financial choice, from buying a house to planning a vacation, effectively becomes a decision about your retirement timeline. These choices often involve trading immediate comfort or pleasure for future financial freedom. This trade-off appears to be a challenge for many Americans.

Data from the Federal Reserve indicates that the median retirement account balance for Americans aged 55 to 64 is approximately $185,000. Using the common 4% withdrawal rule, this sum would generate only about $7,400 in annual retirement income, highlighting a significant savings shortfall for many nearing retirement age.

Recommended Savings Rate and Its Impact

A recommended benchmark for retirement savings is 25% of gross income. This rate generally puts individuals on a solid path toward financial independence.

For instance, saving 25% annually by age 30, with a 6% average annual return, could allow someone retiring at 65 to replace nearly 120% of their pre-retirement income. This scenario offers a ‘pay raise’ in retirement.

The ideal savings rate can vary based on individual factors like age, lifestyle, goals, and current financial standing. Someone starting to invest at 22 has considerably more flexibility than someone beginning at 42. Resources are available to help individuals determine appropriate savings targets based on their age.

Creating Financial Margin

A significant obstacle preventing many from increasing their savings rate is a lack of financial margin. This margin is the difference between income earned and expenses spent. Without this gap, it’s difficult to allocate more money towards savings and investments.

MarketWatch reports that 57% of Americans live paycheck to paycheck, leaving little room for additional savings. Creating margin involves two primary strategies: spending less or earning more. For many, addressing lifestyle creep—where spending increases proportionally with income—is a crucial first step.

Strategies for Increasing Savings

Automating investments is a powerful tool to combat lifestyle creep. By setting up automatic contributions to retirement accounts like 401(k)s and Roth IRAs, money is saved before it can be spent. This ‘out of sight, out of mind’ approach helps ensure consistent saving.

Another effective method is the 60/40 rule for raises and bonuses. This strategy suggests allocating 60% of any additional income towards savings and investments, while dedicating the remaining 40% to lifestyle upgrades. This balanced approach allows for enjoying rewards while still progressing toward financial goals.

Conclusion: The Power of Consistent Savings

Ultimately, the savings rate is the single decision that shapes one’s financial future. The consistent allocation of income to investments, month after month, year after year, is the key differentiator between early retirement and prolonged work.

Even with a strong savings rate, understanding which accounts to use and in what order is vital. A structured approach like the financial order of operations can guide these decisions. The journey toward a ‘great, big, beautiful tomorrow’ is built on the foundation of consistent, strategic savings.

Source: This One Decision Determines Your Financial Future (YouTube)

Related Articles

Energy Stocks Surge as Geopolitical Tensions Rise

Energy stocks are showing strength as geopolitical tensions rise and key shipping routes face disruption. Companies providing essential services like backup power and natural gas are seeing increased investor interest. Strategists advise focusing on fundamental value and timing investments to navigate market volatility.

Borrow Smart, Earn More: Real Estate Arbitrage Wins

Smart real estate investors are using arbitrage to profit by borrowing at low rates and investing for higher returns. This strategy focuses on controlling assets and maximizing capital growth. Understanding interest rates and regional market differences is key to successful arbitrage.

2025 Crash: How Investors Stayed Calm

The 2025 market crash tested investor resolve, but a consistent strategy of dollar-cost averaging helped many stay calm. This method of investing a fixed amount regularly proved effective in smoothing out market volatility and reducing emotional decision-making.