Americans Fall Short: Savings Lag Behind Benchmarks

Many Americans are falling short of recommended savings benchmarks for their age, with net worth figures often lagging behind targets. Key challenges include lifestyle inflation and the need for consistent saving habits across different decades of life. Addressing these gaps is crucial for long-term financial security and retirement.

Americans Fall Short: Savings Lag Behind Benchmarks

Many American households are not saving enough to meet financial benchmarks for their age, a trend that could impact retirement security. While specific targets exist for different age groups, a significant portion of the population finds itself falling behind. This disparity highlights common financial challenges like lifestyle inflation and the need for consistent saving and investing habits.

Understanding net worth is key to grasping personal finance. Net worth is simply what you own (assets) minus what you owe (liabilities).

This includes everything from savings accounts and retirement funds to cars and homes, offset by debts like student loans or credit card balances. It offers a snapshot of your overall financial health, much like a scale shows your weight.

Savings Goals by Age

For those in their 20s, the focus should be on building a solid financial foundation. Experts suggest saving at least 10% to 15% of your income.

If that’s not possible, starting with 5% and increasing it over time is a good strategy. Taking full advantage of employer 401(k) matches is crucial, as it provides an immediate, unmatched return on investment.

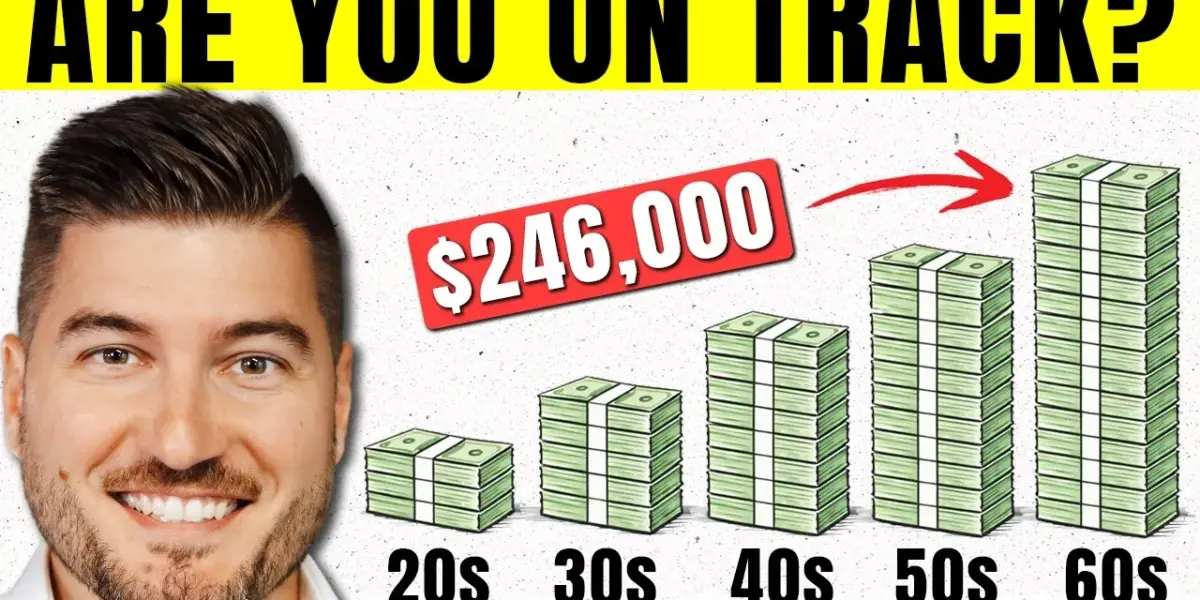

By the time Americans reach their 30s, financial progress should become more noticeable. The benchmark is to have saved an amount equal to your annual salary by age 30. This target increases significantly by age 40, aiming for three times your annual salary.

For example, someone earning $70,000 a year should aim to have $70,000 saved by age 30 and $210,000 by age 40. A major pitfall during this decade is lifestyle inflation, where increased income leads to increased spending rather than increased savings.

The 40s represent a critical decade for evaluating the impact of earlier financial decisions. Benchmarks suggest saving four times your annual salary by age 45 and six times your salary by age 50. For an $85,000 earner, this means having $340,000 saved by 45 and $510,000 by 50.

It’s also vital to pay attention to investment fees, which can significantly erode returns over time. High fees, even 1% on a large portfolio, can cost thousands annually, while low-cost index funds can save substantial amounts.

The years leading up to retirement are often termed the “catch-up decade.” By age 55, the goal is to have saved seven times your salary, increasing to eight times by age 60. The government allows for higher “catch-up” contributions to retirement accounts for individuals aged 50 and older, which can help close previous savings gaps. Earnings typically peak between ages 35 and 44, so the 50s offer a final window to significantly boost income through raises or promotions before earnings begin to decline.

Common Roadblocks to Savings

Several factors contribute to why many people fall short of their savings goals. These include a lack of financial literacy, procrastination, high-interest debt, lifestyle inflation, unexpected life events like illness or divorce, and the general erosion of purchasing power due to inflation. Addressing these issues is essential for building long-term financial security.

Paying off high-interest debt, such as credit cards with 25% interest, can be seen as a guaranteed tax-free return on investment. Avoiding lifestyle inflation, where spending grows with income, is crucial for allowing savings to outpace expenses.

Unexpected life events, while often uncontrollable, can be mitigated with emergency funds and insurance. Inflation, a “stealth tax,” diminishes the value of cash savings over time, making investing essential.

Approaching Retirement

By the 60s, the goal is to have saved approximately 10 times your mid-career salary. For someone earning $100,000, this translates to a $1 million portfolio. However, the median net worth for households aged 65 to 74 is significantly lower, around $49,000, often including home equity.

Key considerations in the 60s include Social Security and retirement account withdrawals. Claiming Social Security before the full retirement age (67 for those born in 1960 or later) permanently reduces monthly benefits.

Delaying until age 70 can increase benefits substantially. Withdrawals from Roth IRAs and Roth 401(k)s are tax-free after age 59 and a half, offering significant tax savings over a long retirement.

Market Impact and Investor Takeaways

The data suggests a widespread savings gap across age groups. This could lead to increased reliance on Social Security, potential difficulties in retirement, and a higher demand for financial advisory services. For investors, it highlights the importance of starting early and being consistent.

The power of compounding returns over decades is significant. Low-cost investing in tax-advantaged accounts remains a cornerstone of long-term wealth building.

Investors should regularly review their investment fees and consider shifting to low-cost index funds if expense ratios exceed 0.2%. Maintaining an emergency fund is vital to avoid costly early withdrawals from retirement accounts. The final working years, particularly the 50s, offer a critical opportunity to increase savings and income through career advancement.

Financial success ultimately comes down to fundamental principles: spending less than you earn, saving consistently, increasing savings rates as income grows, investing wisely in low-cost, tax-advantaged accounts, and allowing investments to compound. Discipline is the main challenge, especially when faced with constant pressure to spend.

The year 2028 is targeted for commercial production of deep-sea mineral deposits, highlighting emerging investment opportunities in critical minerals and the ongoing efforts to onshore supply chains.

Source: The Exact Amount You Should Have Saved At Every Age (YouTube)

Related Articles

Young Investor Builds $91K in 5 Years Through Smart Savings

A young investor built a nearly $91,000 portfolio in just five years by consistently saving 25% of his income and maximizing employer retirement plan matches. Starting at age 25 with a $50,000 salary, his disciplined approach, including a 5% annual raise, led to substantial tax-free growth by age 29.

Most Crypto Traders Lose Money: Skills & Patience Win

The cryptocurrency market is challenging, with most traders losing money due to a "get-rich-quick" mindset. Long-term Bitcoin holders and those who develop specialized skills, such as trading or on-chain analysis, have the highest probability of success. Patience and continuous learning are crucial for navigating the crypto space effectively.

Schemes Fall Short: Experts Debunk Wild Money-Making Ideas

Financial advisors dissect popular money-making schemes, from day trading to "infinite banking," finding most fall short. They advocate for proven, simple strategies like index fund investing and consistent financial planning over risky, unproven ideas.