Median Home Price Now Out of Reach for Median Income

The median home price in the U.S. has now surpassed what the median household income can afford, creating a significant barrier to homeownership. Analysis shows a required salary of over $112,000 for the median home price, far exceeding the median income of $84,000. This affordability gap challenges the traditional dream of owning a home for many Americans.

Homeownership Dream Fades as Prices Soar Past Salaries

Buying a home in America feels more like a distant dream than an achievable goal for many. New analysis reveals a stark reality: the median home price in the U.S. has climbed to a point where the median household income can no longer comfortably afford it. This widening gap is making the path to homeownership incredibly difficult for a significant portion of the population.

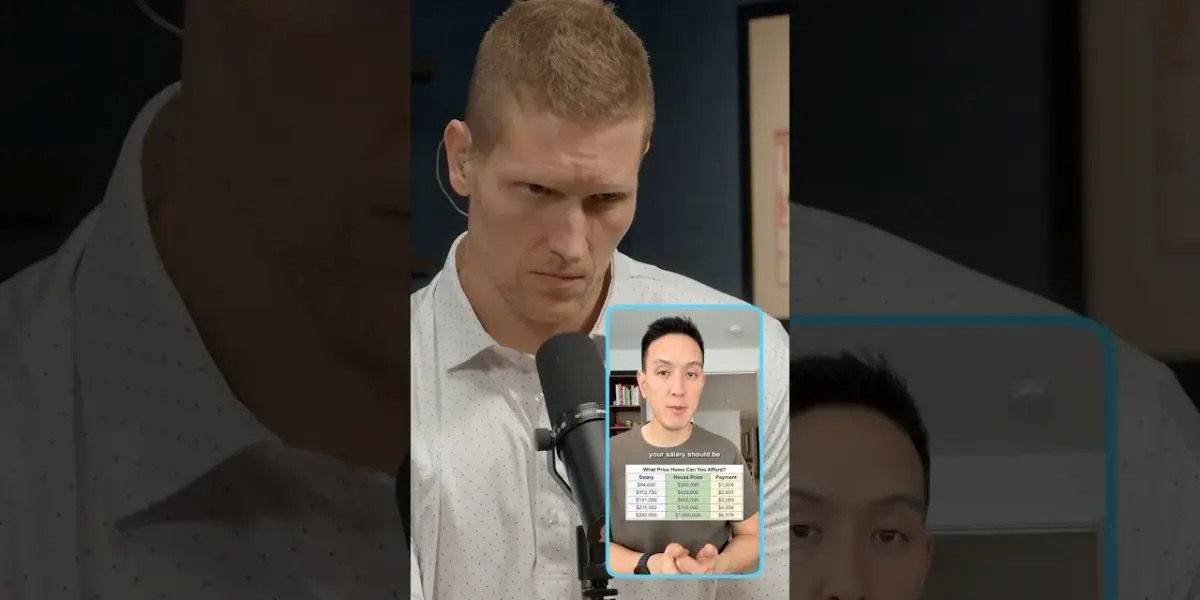

Consider the numbers: the median home price in America recently stood at approximately $410,000. To afford a home of this value with a 6% 30-year mortgage, property taxes, and insurance, a person would need a yearly salary of around $112,750. This calculation uses a common guideline known as the 28% rule, which suggests that your total housing expenses shouldn’t exceed 28% of your gross monthly income. This figure assumes a substantial 20% down payment.

The Income Gap Widens Significantly

The median household income in the U.S. hovers around $84,000 per year. When compared to the $112,750 salary needed for the median-priced home, a clear shortfall emerges. This means that the average American family is now priced out of buying the average American home, a significant shift from previous decades.

This disparity highlights a major challenge for aspiring homeowners. The dream of owning a piece of property, often seen as a key component of financial stability, is becoming increasingly elusive. The financial requirements are simply too high for a large segment of the population.

Affordability Rules: Traditional vs. First-Time Buyers

Financial experts often point to various rules to gauge home affordability. One common guideline is the 28% rule, which advises keeping total housing costs, including mortgage payments, property taxes, and insurance, below 28% of your gross monthly income. For a $400,000 home with a 6% mortgage and 20% down, the monthly payment would be about $2,631, requiring that $112,750 salary.

However, a slightly different approach, often called the 3-5-25 rule, suggests that first-time homebuyers may not need to put down 20%. This rule recommends a down payment of 3% to 5% and aims to keep total housing expenses at or below 25% of gross income. The idea is to make homeownership accessible while ensuring buyers can manage payments long-term.

The 3-5-25 Rule Explained

The 3-5-25 rule is designed with the realities of first-time buyers in mind. It acknowledges that saving a 20% down payment can be a major hurdle. By allowing for a smaller down payment, like 3% or 5%, more people can enter the housing market sooner.

The key to this rule is the 25% cap on total housing expenses. This means that your monthly mortgage payment, plus property taxes and homeowner’s insurance, should not eat up more than a quarter of your monthly income. This strategy aims to prevent financial strain and ensure buyers can comfortably stay in their homes for a reasonable period, ideally five to seven years.

Market Impact and Investor Considerations

The current housing market dynamics have significant implications for both individuals and the broader economy. When a large portion of the population struggles to afford homes, it can affect consumer spending, demand for home-related goods and services, and overall economic growth.

For potential investors, understanding these affordability trends is crucial. Sectors tied to housing, such as construction, real estate, and home improvement, can be impacted by shifts in demand. While higher prices might seem beneficial for existing homeowners, they create barriers for new entrants and can slow down market activity.

Long-Term Outlook for Homebuyers

The long-term outlook for aspiring homeowners hinges on several factors. These include future interest rate movements, the pace of new home construction, and the growth of wages relative to home price appreciation. If incomes do not keep pace with housing costs, the dream of homeownership will remain out of reach for many.

Government policies and economic conditions will play a role in shaping the housing market. Strategies to increase housing supply or provide more financial assistance for buyers could help ease the affordability crisis. Without such interventions, the gap between housing prices and incomes is likely to persist.

What Investors Should Know

The current housing market presents a complex picture for investors. While home prices have risen significantly, the ability of the average person to purchase a home is declining. This could lead to a slowdown in home sales volume, even if prices remain high or continue to climb slowly.

Investors might look for opportunities in areas that benefit from the current situation, such as rental markets, or companies focused on affordable housing solutions. Understanding the financial constraints of the majority of potential buyers is key to making informed investment decisions in the real estate sector and related industries.

The affordability challenge in the U.S. housing market is a pressing issue. As median home prices continue to outpace median incomes, the path to homeownership becomes steeper. Future trends will depend on economic growth, wage increases, and policies aimed at addressing housing affordability. The next major report on housing starts is expected in mid-November.

Source: This Is Why Buying a Home Feels Impossible (YouTube)

Related Articles

Wall Street Landlords Slash Rents Amid Oversupply

Wall Street landlords are cutting rents by up to 10% in cities like Atlanta due to a surge in accidental landlords and market oversupply. This trend is leading to significant discounts on homes, impacting both renters and sellers.

AI Spots Top 5 Housing Markets for Investors

Artificial intelligence identifies top real estate investment markets like Charlotte, Dallas-Fort Worth, Raleigh-Durham, Columbus, and Indianapolis. While AI highlights growth, experts caution that appreciation may slow, and finding cash flow requires careful analysis, especially in competitive markets.

Real Estate Expert: Affordability Policies Will Worsen Crisis

Manhattan rents have surged to $4,083 for a one-bedroom, far exceeding the national average. Real estate experts warn that proposed affordability policies may worsen the crisis. A significant housing shortage and high mortgage rates continue to challenge buyers and the market.