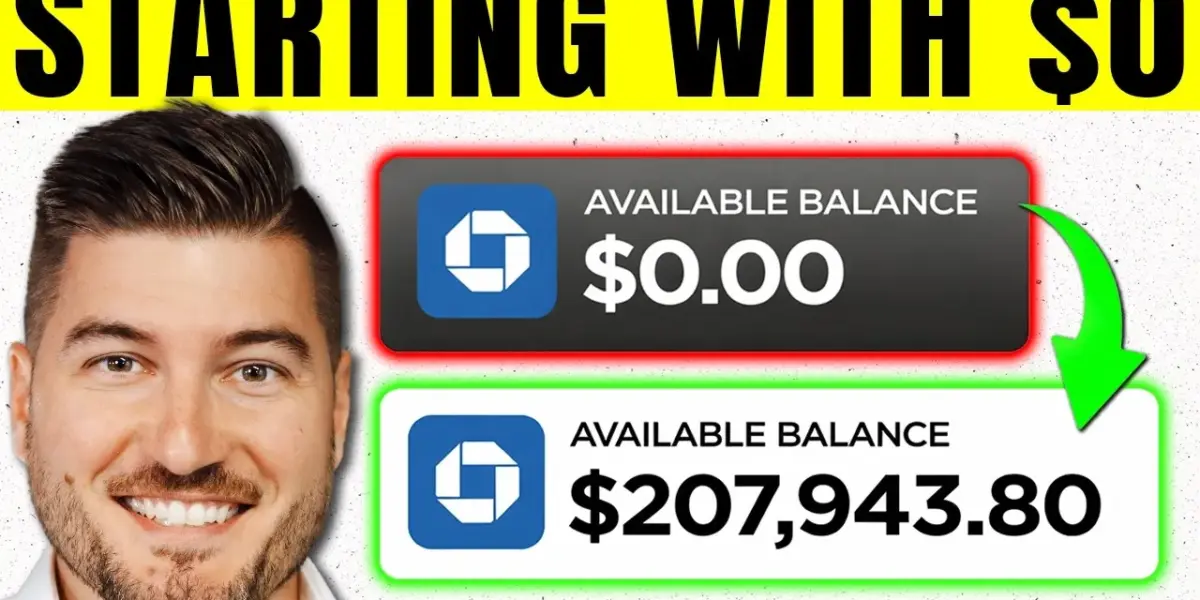

$0 to $96K: Millionaire Reveals Simple Investing Plan

A millionaire investor shared a strategy to build wealth from $0, emphasizing the importance of starting early and investing in low-cost index funds. The plan prioritizes paying off high-interest debt and building an emergency fund before investing. Key recommendations include broad market ETFs like VTI for long-term growth and diversification.

Millionaire Investor Outlines Path from Zero to $96,000 Using Simple Strategy

Starting with no money, a millionaire investor detailed a straightforward strategy that could turn an initial investment into nearly $96,000 over time. This method bypasses the need for stock picking or constant market monitoring. The key, he explains, is to simply begin investing and allow compounding to work its magic.

Many people lose potential gains simply by not starting. By the time they decide to invest, years of compounding growth may have already passed them by, representing a loss they cannot recover. The first crucial step for any investor is understanding how money loses value while sitting idle.

Inflation Erodes Bank Account Savings

Money kept in a standard bank account is steadily losing purchasing power due to inflation. Inflation means that prices for goods and services rise over time, causing each dollar to buy less than it did before. For example, if an orange cost $2 last year and now costs $3, that $1 increase reflects inflation.

In the United States, inflation has averaged about 3% annually. Most savings accounts offer interest rates that do not keep pace with this inflation rate. Therefore, keeping money in a bank account, while feeling safe, actually means accepting a gradual decrease in what that money can buy.

Understanding Investment Growth: Appreciation and Compounding

Investing in the stock market offers two primary ways for money to grow. The first is appreciation, where the value of an asset increases over time. If you own a piece of a company and that company becomes more successful, your share of ownership becomes more valuable.

The second, and often more powerful, growth mechanism is compounding. This is often described as a snowball rolling downhill, gathering more snow as it goes. If you invest $1,000 and earn a 10% return in the first year, you have $1,100.

In the second year, you earn 10% on the new total of $1,100, resulting in $1,210. This process repeats, with earnings generating further earnings, leading to significant growth over extended periods without adding new money.

Avoiding Common Beginner Mistakes

A frequent error made by new investors is chasing stocks that have recently surged in price. While it might seem logical that a rising stock will continue to climb, this approach often backfires, particularly in fast-moving sectors like technology. History shows that the top companies can change significantly over a decade.

Companies like Nokia, once a dominant force in the mobile phone market, saw their market share and stock price plummet. Similarly, the leading companies of the 1980s, 2000s, and today are vastly different. Relying on past performance of the current leaders can leave investors behind as the market evolves.

The Power of Index Funds

For beginners, index funds offer a recommended path to investing. An index fund is a type of mutual fund or exchange-traded fund (ETF) with a portfolio constructed to match or track the components of a financial market index, such as the S&P 500. The S&P 500 includes the 500 largest publicly traded companies in the U.S.

By investing in an S&P 500 index fund, an investor buys a small piece of all 500 companies simultaneously. This diversification spreads risk, meaning that the failure of one company has a minimal impact on the overall investment. Warren Buffett, a highly successful investor, has recommended low-cost index funds as the best approach for most investors.

Understanding Expense Ratios

Index funds, like all funds, have an expense ratio. This is an annual fee charged to manage the fund.

For instance, a $100,000 investment in a fund with a 1% expense ratio would cost $1,000 per year in fees. However, many index funds offer very low expense ratios, some as low as 0.02%, which would only be $20 per year on the same $100,000 investment.

Prerequisites for Investing: Debt and Emergency Funds

Before beginning to invest, two critical steps should be addressed. First, pay off any high-interest debt, typically anything above 10%, such as credit card debt.

The interest paid on such debt can easily outweigh potential investment gains. Paying off 25% interest credit card debt is equivalent to a guaranteed, tax-free 25% return.

Second, establish an emergency fund covering three to six months of living expenses. This fund acts as a safety net for unexpected events like job loss or medical emergencies. Without it, investors might be forced to sell investments at a loss to cover immediate needs, negating the benefits of investing and potentially creating taxable events.

Choosing the Right Investment Vehicle

There are two main types of investment accounts: retirement accounts and taxable brokerage accounts. Retirement accounts, like 401(k)s or Roth IRAs, offer significant tax advantages and are ideal for long-term wealth building. However, they often have contribution limits and penalties for early withdrawal.

Taxable brokerage accounts, offered by firms like Fidelity, Schwab, and Robinhood, provide more flexibility with no contribution limits and easier access to funds. These accounts are suitable for investing beyond retirement savings goals.

Executing Your First Investment

Opening a brokerage account is the first step to buying investments. Platforms allow investors to purchase stocks, ETFs, and mutual funds. Investors can place a market order to buy at the current trading price or a limit order to buy at a specific lower price.

Many modern platforms also allow the purchase of fractional shares. This means an investor can buy a portion of a share, even if they don’t have enough money to buy a full share. For example, with Apple trading at over $260 per share, someone with $100 could buy about a third of a share.

The Importance of Time in the Market

A common pitfall for new investors is making emotional decisions during market downturns. For instance, investing $10,000 in an index fund like QQQ (tracking the top 100 tech companies) at its 2007 peak could have seen the investment drop by 50% during the 2008 financial crisis. The instinct might be to sell and cut losses.

However, holding onto the investment through market volatility can lead to substantial long-term gains. The same $10,000 investment, if held through the downturn and subsequent recovery, could grow to nearly $96,000 by 2025.

Research indicates that missing even the 10 best trading days in a decade can significantly reduce overall returns. This highlights that staying invested through ups and downs, known as ‘time in the market,’ is more effective than trying to predict market movements (‘timing the market’).

Recommended Index Funds for Beginners

For those starting out, three specific index funds are recommended for their diversification and low costs:

- Vanguard Total Stock Market ETF (VTI): This ETF offers broad exposure to the entire U.S. stock market, covering approximately 3,700 companies. It has an extremely low expense ratio of 0.03% and is considered a ‘set it and forget it’ option for maximum diversification.

- Vanguard Growth ETF (VUG): This fund focuses on companies expected to grow faster than the market average, often in technology sectors. It has an expense ratio of 0.04% and is suitable for investors with a longer time horizon who can tolerate higher volatility.

- Schwab U.S. Dividend Equity ETF (SCHD): This ETF invests in large, established companies that pay regular dividends. With an expense ratio of 0.06%, it appeals to investors seeking passive income or those nearing retirement who prioritize cash flow.

Understanding Capital Gains Taxes

When selling an investment for a profit, the gain is subject to capital gains tax. If an investment is held for less than one year, short-term capital gains apply, taxed at ordinary income rates. Holding an investment for over a year qualifies for lower long-term capital gains rates, which are 0%, 15%, or 20%, depending on the investor’s tax bracket.

This tax structure incentivizes long-term investing. Conversely, selling an investment at a loss (a capital loss) can be used to reduce taxable income, softening the financial impact.

A Patient, Diversified Approach Wins

The most effective investing strategy for long-term success is often described as boring: it’s diversified, consistent, and patient. Building a solid financial foundation by paying off high-interest debt and establishing an emergency fund is paramount. Automating investments and allowing time to work through compounding is key.

While speculative trading like day trading might seem appealing, studies show that a vast majority of participants lose money. The most successful investors focus on understanding their investments, holding them for the long term, and minimizing emotional decisions. The strategy of buying and holding diversified assets, like VTI, is the foundation for building lasting wealth.

Source: MILLIONAIRE EXPLAINS: If I Started Investing With $0, This Is Exactly What I'd Do (YouTube)

Related Articles

Comedian Bobby Lee Avoids His Finances; What Investors Should Know

Comedian Bobby Lee admits he doesn't know how much money he makes, relying entirely on a financial manager. While this works for him, financial experts stress that for most people, understanding personal income and expenses is crucial for sound investing and financial stability.

Market Sees Historic Rally: Experts Advise Staying Invested

The stock market is experiencing a historic rally with significant returns, leading experts to advise investors to stay invested. Key sectors like AI infrastructure, semiconductors, industrials, and healthcare are showing strong growth potential. Investors should focus on companies with high demand and strategic market positioning.

GOP Lawmaker Warns of Socialist Policies Derailing Dems

A Republican lawmaker warns that the Democratic Party's embrace of "socialist policies" could lead to political downfall. He uses the analogy of a bus losing its wheels to describe the potential negative consequences of this ideological shift.