Fed’s Inflation Target: Misinformation vs. Reality

Federal Reserve Chair Jerome Powell's recent speech at Jackson Hole was misconstrued, leading to widespread misinformation about abandoning the 2% inflation target. The reality is a shift away from average inflation targeting, not a departure from the core goal.

Fed Reaffirms Inflation Target Amidst Market Misinterpretation

In a notable turn of events that rippled through financial markets and social media, Federal Reserve Chair Jerome Powell’s recent keynote speech at the Jackson Hole Symposium became the subject of widespread misinformation. Contrary to sensational online claims that the Fed had abandoned its long-standing 2% inflation target, a closer examination of Powell’s remarks and the underlying policy updates reveals a significant reaffirmation of the target, alongside a nuanced shift in policy considerations.

The Genesis of Misinformation

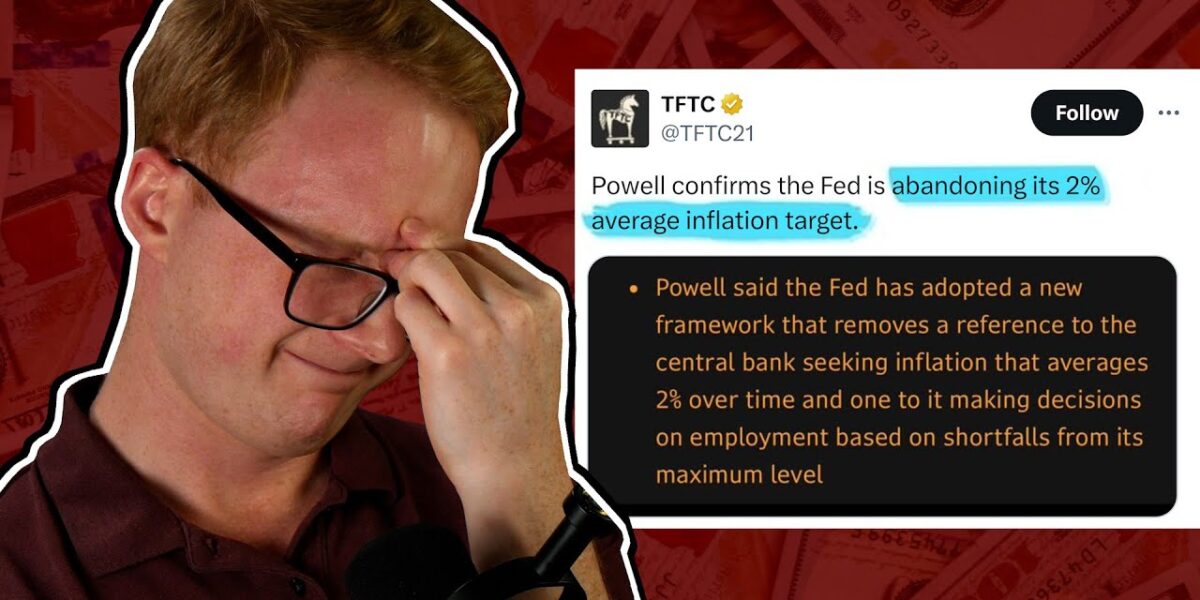

The confusion originated from an unsourced screenshot circulating online, purportedly indicating that the Federal Reserve was moving away from its 2% inflation target to prioritize employment. This seemingly drastic announcement led to a flurry of alarmist posts on platforms like ‘Finance X,’ warning of impending hyperinflation and the devaluation of the U.S. dollar. However, investigative work, including a thorough review of the 20-minute speech transcript, debunked these claims, highlighting a severe misinterpretation of the Fed’s actual policy direction.

Decoding Powell’s Jackson Hole Address

During his speech, Powell acknowledged the current environment of relatively tame inflation and low unemployment rates but characterized the economic situation as ‘curious.’ He pointed to several factors influencing the economy, including slowing GDP growth and shifts in both labor supply and demand. The speech also touched upon risks to inflation, particularly those stemming from tariffs, which could potentially lead to more persistent price increases than initially anticipated.

A key statement that likely fueled the misinterpretation was Powell’s remark: “The baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” This sentence, in the context of the Fed’s dual mandate of price stability and maximum employment, suggested a potential recalibration of monetary policy. However, it did not signal an abandonment of the inflation target.

The ‘Average Inflation Targeting’ Clarification

The core of the misunderstanding appears to stem from a misreading of an update to the Federal Reserve’s statement on longer-run goals and monetary policy strategy. Following the 2008 financial crisis, the Fed adopted an ‘average inflation targeting’ framework. This strategy aimed to allow inflation to moderately exceed 2% for a period if it had previously run below the target, ensuring that inflation would average 2% over the long term. This approach was intended to provide greater flexibility in monetary policy, especially when interest rates were already near their lower bound.

However, the recent update announced at Jackson Hole signaled a move *away* from this ‘makeup strategy’ or average inflation targeting. The Federal Reserve decided to revert to its previous approach of targeting 2% inflation on an annual basis. This change means the Fed will no longer seek to compensate for periods of below-target inflation by allowing inflation to overshoot in subsequent years. The statement that the Fed was “moving away from its makeup strategy around inflation” and focusing more on employment was technically correct but was profoundly misinterpreted in isolation.

Market Reaction and Investor Implications

The initial market reaction on Friday saw a jump in both traditional markets and the cryptocurrency sector, likely driven by the erroneous belief that the Fed was shifting to a more dovish stance and preparing for imminent rate cuts. However, the clarification that the Fed is merely reverting to a simpler, year-on-year 2% inflation target, rather than abandoning it, is crucial for investors to understand.

What Investors Should Know

- Reaffirmation of 2% Target: The Federal Reserve has not abandoned its 2% inflation target. Instead, it is moving away from the ‘average inflation targeting’ framework adopted in 2020.

- Nuanced Policy Stance: While Powell’s speech suggested a willingness to consider adjusting policy based on evolving economic data and risks (particularly to employment), this does not equate to an immediate pivot to easing monetary policy.

- No Commitment to Rate Cuts: The speech did not commit to any specific timeline for rate cuts. Future policy decisions will remain data-dependent.

- Liquidity Considerations: The discussion around the draining of the reverse repo facility and ongoing quantitative tightening (QT) highlights broader concerns about liquidity in the financial system. While these factors can exert downward pressure, they do not automatically translate into immediate stimulus measures from the Fed.

- Beware of Misinformation: The incident underscores the importance of verifying information from primary sources, especially in the financial domain, where sensationalized or misinterpreted claims can significantly influence market sentiment and investment decisions.

Broader Economic Context

The Federal Reserve operates under a dual mandate: to promote maximum employment and maintain price stability. Powell’s speech emphasized the need to balance these objectives in the face of conflicting economic signals. While inflation risks remain, the Fed is also mindful of potential weakness in the labor market and the broader economic slowdown. The mention of potentially restrictive interest rates remaining above the ‘neutral rate’—the level at which monetary policy neither stimulates nor restricts the economy—suggests that even if rate cuts occur, they may not signify a complete reversal of the Fed’s anti-inflationary stance in the short to medium term.

Conclusion

The misinterpretation of Jerome Powell’s Jackson Hole speech serves as a potent reminder of the challenges in navigating financial news and social media. The narrative of the Fed abandoning its inflation target was a fabrication based on a misunderstanding of a technical policy adjustment. While the Fed’s rhetoric may have subtly shifted to acknowledge a wider range of economic risks and a potential flexibility in policy adjustments, the commitment to controlling inflation remains a central pillar of its strategy. Investors should focus on the actual policy statements and economic data rather than succumbing to sensationalized online narratives.

Source: Clearing Up the Inflation Target Misinformation (YouTube)

Related Articles

High Debt Forces Fed’s Hand, Paving Way for Rate Cuts

Massive U.S. debt is limiting the Federal Reserve's ability to fight inflation, potentially forcing interest rate cuts. This delicate balancing act risks higher inflation and impacts the real estate market, creating both challenges and opportunities.

Trump Threatens Fed Chair Powell, Faces Nomination Blockade

President Trump is threatening to fire Fed Chair Jerome Powell over a renovation probe, creating a political stalemate. Senator Tom Tillis is blocking Trump's nominee, Kevin Warsh, until the investigation concludes. Warsh himself faces scrutiny over his vast personal wealth, estimated between $135-226 million, raising conflict of interest concerns.

Trump Threatens to Fire Fed Chair Powell Over Building Project

Former President Donald Trump issued a strong ultimatum to Federal Reserve Chair Jerome Powell, threatening to fire him over perceived incompetence and excessive spending on a building project. Trump also expressed support for lowering interest rates and the confirmation of Kevin Warsh.