Economy’s Hidden Dangers: Why Wall Street’s Optimism Deceives

Despite record highs on Wall Street, everyday Americans face financial strain, rising debt, and falling real income. A deep dive into economic data and historical parallels with 2007-2008 reveals that misleading signals and a weakening U.S. Treasury market point to hidden dangers beneath the surface of market optimism.

Economy’s Hidden Dangers: Why Wall Street’s Optimism Deceives

Right now, many people feel a strain on their finances, a feeling that doesn’t match the positive signals coming from financial markets and some government reports. This difference between everyday experience and market performance can be confusing. We’re going to look at why things feel so off, comparing current events to past economic troubles, and examine data that might tell a different story than what we’re being told.

A Warning from the Past

Henry “Hank” Paulson, who was the Treasury Secretary during the 2008 financial crisis, recently spoke about the economy. He warned that we might be heading into a crisis that feels similar to 2008, and that when we hit a wall, it could be severe. Paulson has a deep understanding of financial crises, having spent 32 years at Goldman Sachs and playing a key role in managing the 2008 meltdown, including orchestrating the $700 billion TARP bailout.

In 2008, Paulson and the Federal Reserve chairman Ben Bernanke urgently pushed for a bailout package, fearing the collapse of the entire economy. They even had a secret contingency plan called the “break the glass memo.” This historical context makes Paulson’s current warnings about a potential crisis especially significant, even if some criticize his past actions and the benefits of bailouts.

Echoes of 2007

The situation today shows striking similarities to the period before the 2008 crisis. In late 2007, the common belief on Wall Street was that the economy would experience a “soft landing” despite signs of a slowing housing market. Major financial institutions predicted stock market gains, and most money managers expected prices to rise.

During this time, the stock market reached record highs. However, many were overlooking serious issues. Home sales and housing starts were dropping significantly, and homebuilder confidence was at a low not seen in decades.

Oil prices had doubled, and gas prices hit $3 a gallon for the first time. Despite these warnings, the market continued to climb, much like it is doing now.

Officials at the time, including Bernanke and Paulson, downplayed the impact of problems in the subprime mortgage market, calling it “contained” and the global economy “robust.” Today, similar phrases are used to describe issues in private credit and manufacturing, even as underlying problems persist. This pattern of optimism despite negative indicators feels uncomfortably familiar.

Misleading Economic Signals

Current economic data presents a confusing picture. For instance, manufacturing surveys, like the Empire State and Philly Fed surveys, have shown surprising jumps in activity. However, a closer look reveals these numbers might be misleading.

In the Empire State survey, while activity appeared to rise, the cost of materials surged, and future optimism actually fell. Similarly, the Philly Fed survey showed negative employment figures, with many firms cutting jobs. The reported increase in manufacturing activity seems to be driven by companies “front-loading” orders to get ahead of expected price increases, especially due to tariffs and rising fuel costs.

This means that reported growth in these sectors is not a sign of a healthy economy but rather a symptom of inflation and anticipation of higher costs. The International Monetary Fund (IMF) also lowered its global growth forecast due to oil shocks. When oil prices dropped and the stock market hit new highs, it seemed like a positive sign, but this was largely influenced by geopolitical events and temporary market reactions.

Tax Refunds vs. Rising Costs

The administration has pointed to record-high tax refunds as evidence of economic strength. While the average refund has increased, the real value of these refunds is significantly reduced when adjusted for inflation. Economists have noted that the rise in gas prices, largely due to global events, has almost completely offset the benefit of these refunds for the average household.

For lower-income Americans, who spend a larger portion of their income on fuel, the increase in gas costs has actually cost them more than they received back in refunds. This disparity highlights how the official economic numbers may not reflect the financial reality for many citizens.

The Core Problem: A Weakening Treasury Market

The key difference between today’s economic situation and 2008 is the state of the U.S. Treasury market. In 2008, the U.S. government’s balance sheet was relatively strong, with a national debt of about $9.5 trillion. During the crisis, investors flocked to U.S. Treasuries as a safe haven, allowing the government to borrow trillions at low interest rates to fund bailouts.

Today, the national debt has ballooned to nearly $39 trillion, with a projected annual deficit of $1.9 trillion. Interest payments alone on this debt have exceeded $1 trillion, surpassing spending on defense and Medicare. The debt-to-GDP ratio is projected to reach 120% by 2036, a level not seen since World War II.

This massive debt, coupled with years of deficits, trade wars, and other policies, has weakened confidence in the Treasury market. Credit rating agencies have downgraded the U.S., and foreign holdings of Treasuries have fallen significantly. New buyers, like hedge funds and money market funds, are purchasing Treasuries not for safety but for yield, meaning they could leave quickly if better opportunities arise.

This fragile demand for Treasuries is evident in recent weak auction results. The Federal Reserve is also limited in its ability to help, as current interest rates are too high to stimulate the economy through rate cuts, unlike in 2008.

This situation leads to Paulson’s warning: what happens when the “fire extinguisher is on fire”? If central banks and foreign investors abandon U.S. Treasuries during a crisis, the market that once saved the global economy could become the source of the next crisis.

The Reality for Most Americans

The disconnect between Wall Street’s performance and the everyday experience of most Americans is stark. Personal income dropped in February, and real disposable income has fallen. The personal savings rate is low, while household debt and credit card delinquencies are at record highs, surpassing levels seen during the 2008 crisis.

When stock markets hit records, it primarily benefits the wealthiest segment of the population. The vast amounts of stimulus money injected into the economy over the past 14 years, totaling between $17 and $19 trillion, have largely been absorbed by corporate America rather than benefiting consumers long-term. The Federal Reserve’s balance sheet has expanded dramatically, and tax cuts and deregulation have further fueled this.

Ultimately, real-world numbers—supply and demand, inflation, personal income, and household debt—tell a different story than the stock market. With savings at a low, credit card debt soaring, and the U.S. Treasury market showing signs of weakness, the economic situation is far from stable. As Paulson warned, the very instrument that rescued the global economy in 2008 is now showing cracks, suggesting that the current optimism is built on shaky ground and nothing is as it seems.

Source: Trump ECONOMIC COLLAPSE Hidden in Plain Sight (YouTube)

Related Articles

Military Certainty Needed for Gas Prices to Fall

Experts state that military certainty in key regions is essential for gas prices to fall consistently. Recent price swings highlight market volatility, driven by concerns over the Strait of Hormuz. High diesel and fertilizer costs also pose a risk of future food price inflation.

Gas Prices Won’t Fall for Months, Economist Warns

Economist Henrietta Trace warns that gas prices are unlikely to return to pre-war levels for months due to significant disruptions in global fuel supply. Damaged facilities and logistical challenges mean consumers will likely face elevated prices for an extended period. This economic pressure is also influencing political campaign strategies as elections approach.

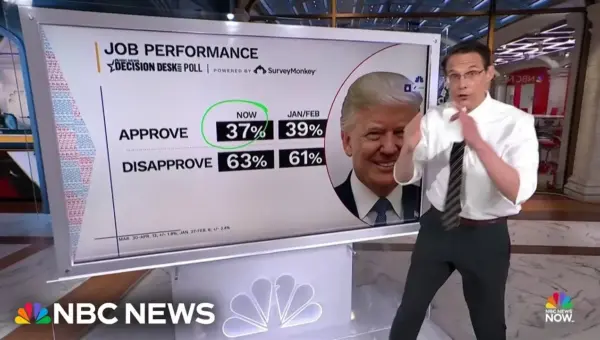

Trump Approval Dips to New Low Amid War and Rising Costs

President Trump's approval rating has dropped to a new low of 37%, with the ongoing war in Iran and rising inflation cited as key reasons. Young voters, particularly Generation Z, are showing significant disapproval, with 76% expressing negative views of his job performance. Student interviews reveal widespread frustration with economic conditions and foreign policy decisions.