Unlock Home Equity: Your Guide to HELOCs

Unlock the power of your home's value by understanding home equity and how it translates into Home Equity Line of Credit (HELOC) limits. Learn how to calculate your usable equity and what factors influence your borrowing potential.

Unlock Home Equity: Your Guide to HELOCs

Homeowners looking to tap into their property’s value are increasingly exploring Home Equity Lines of Credit (HELOCs). Understanding how much equity you have available is the first crucial step. This article breaks down the concept of home equity and how it relates to HELOC limits, offering a practical perspective for homeowners.

What is Home Equity?

Home equity is the difference between your home’s current market value and the amount you owe on your mortgage. Essentially, it’s the portion of your home that you truly own outright. For example, if your home is appraised at $500,000 and you still owe $250,000 on your mortgage, your total home equity is $250,000 ($500,000 – $250,000).

Calculating Your Usable Equity for HELOCs

While total equity is important, lenders consider ‘usable’ or ‘loanable’ equity when determining HELOC limits. Most lenders will allow you to borrow up to a certain percentage of your home’s value, often referred to as the Combined Loan-to-Value (CLTV) ratio. A common threshold is 90% CLTV.

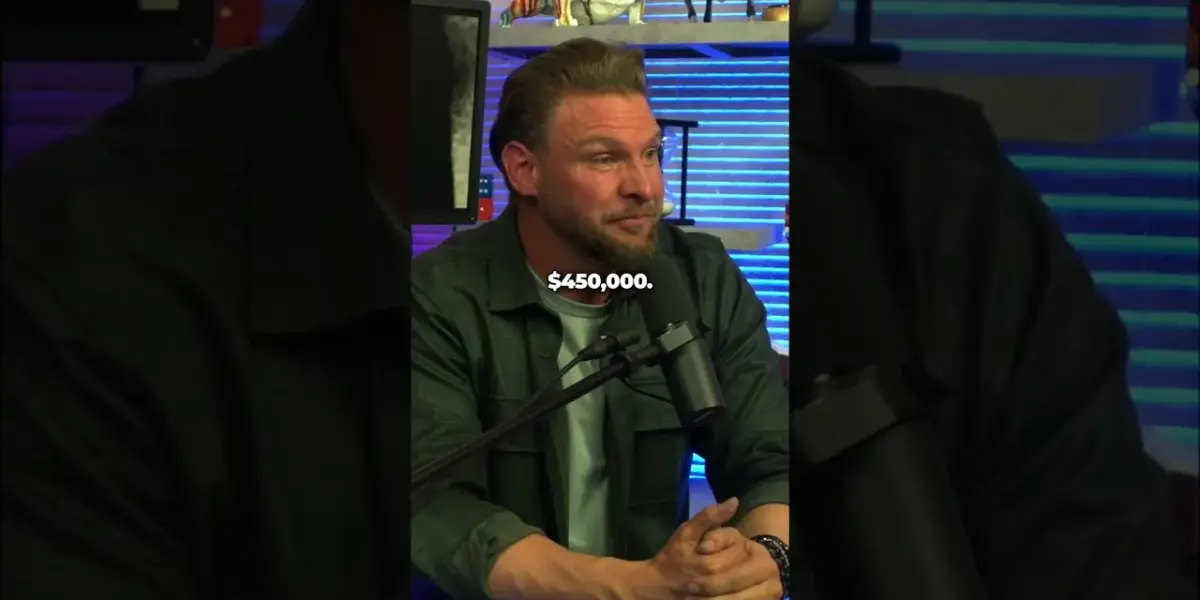

Let’s use our previous example: a home valued at $500,000.

- Maximum Loan-to-Value (LTV): If a bank allows up to 90% LTV, they are willing to lend up to $450,000 against your property (90% of $500,000).

- Calculating Available Equity: From this maximum loanable amount ($450,000), you subtract what you currently owe on your mortgage ($250,000).

- Result: The difference, $200,000 ($450,000 – $250,000), represents your usable equity available for a HELOC. This is the amount a lender might consider lending you through a HELOC, subject to their specific underwriting criteria.

Understanding HELOCs

A Home Equity Line of Credit (HELOC) is a revolving line of credit that allows you to borrow money against the equity in your home. Unlike a home equity loan, which provides a lump sum, a HELOC functions more like a credit card. You can draw funds as needed up to your credit limit during a draw period, and you typically make interest-only payments during this time. After the draw period ends, a repayment period begins, during which you’ll pay back both principal and interest.

Factors Influencing HELOC Approval and Limits

Several factors influence how much you can borrow and whether you’re approved for a HELOC:

- Credit Score: Lenders assess your creditworthiness. Higher scores generally lead to better terms and higher borrowing limits.

- Income and Debt-to-Income Ratio (DTI): Your ability to repay the loan is critical. Lenders will examine your income and existing debt obligations to ensure you can manage the additional payments.

- Home Appraisal: The current market value of your home, as determined by an appraisal, is the foundation for calculating your equity. Fluctuations in the real estate market can impact this value.

- Lender Policies: Each financial institution has its own specific policies regarding CLTV ratios, interest rates, and fees.

The Broader Economic Context

While understanding your home’s equity is a personal financial exercise, it’s influenced by broader economic trends. Interest rates, for instance, play a significant role. Rising interest rates can make HELOCs more expensive, impacting the affordability of drawing from your equity. Conversely, lower rates can make them more attractive. Inflation and the overall health of the housing market also affect home valuations, which in turn impacts the amount of equity available.

Regional Variations and Impact

The real estate market is not monolithic. Home values and equity levels can vary significantly by region. In areas with rapidly appreciating home values, homeowners may have substantial equity built up, making HELOCs a viable option for renovations, debt consolidation, or other large expenses. In slower markets, equity might be less, and borrowing against it could be more challenging.

For Buyers: Understanding equity is crucial even before purchasing. A larger down payment means more initial equity, potentially opening up future borrowing options. For those looking to purchase investment properties, understanding the potential for equity buildup and borrowing capacity is key to financial modeling.

For Sellers: While not directly related to HELOCs, understanding your equity is vital when determining your net profit from a sale, especially after accounting for mortgage payoffs and selling costs.

For Investors: Real estate investors often use equity strategically. Leveraging equity through HELOCs can provide capital for acquiring new properties, funding renovations to increase value (value-add strategies), or managing cash flow. Understanding the maximum loanable amount allows for better financial planning and deal analysis, similar to understanding a property’s potential capitalization rate (cap rate) or cash-on-cash return.

Conclusion

Calculating your home equity and understanding usable equity for HELOCs is a straightforward process that empowers homeowners to make informed financial decisions. By grasping these concepts and considering the broader economic landscape, individuals can better assess if and how tapping into their home’s equity aligns with their financial goals.

Source: How To Quickly Calculate Home Equity and HELOC Limits (YouTube)

Related Articles

Couple Balances Separate Finances, Builds Joint Wealth

Nathan and Crissi are navigating a complex financial landscape with separate accounts, newborn twins, and a new business. Their unique approach to wealth building involves adapting the Financial Order of Operations to align individual financial habits with shared goals for independence.

Buy, Live, Rent: Your Path to Real Estate Wealth

Discover a real estate strategy where you buy a home, live in it, and have tenants pay your mortgage. Learn how instant equity, rental income, and strategic partnerships can turn a small investment into significant wealth.

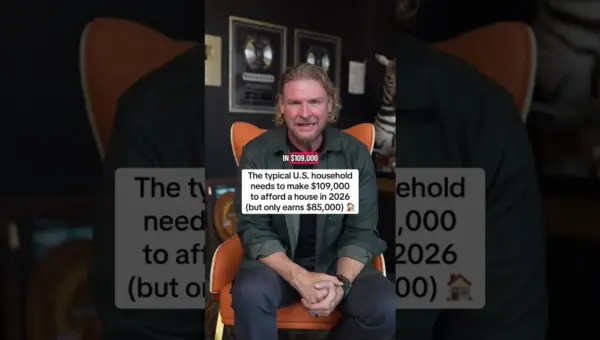

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.