Trump Tax Law Boosts Refunds, But Stimulus Questions Linger

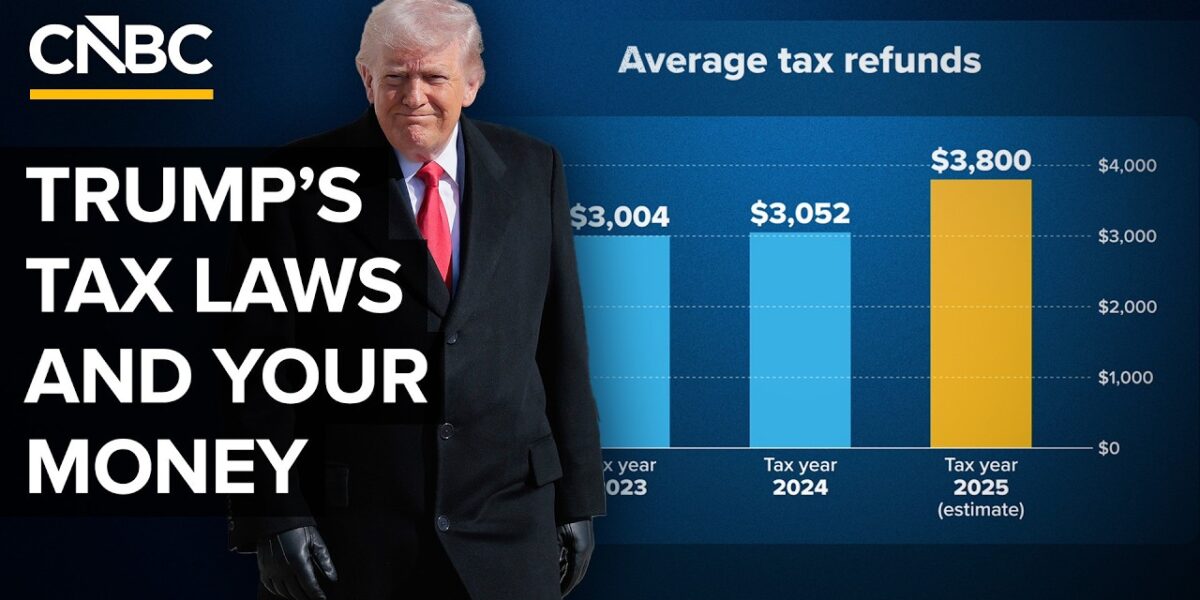

New tax legislation is set to increase average taxpayer refunds by an estimated $800 this year, reaching $3,800. While touted as historic cuts, many benefits are deductions, and economic stimulus hinges on consumer affordability amid rising costs.

Trump Tax Law Boosts Refunds, But Stimulus Questions Linger

The recent passage of significant tax legislation, touted as the largest tax cuts in American history, is poised to alter taxpayer refunds for the upcoming filing season. While the administration highlights benefits such as potential tax exemptions on tips and overtime, and a reprieve for Social Security recipients, a closer examination reveals that the primary impact of the new bill for 2025 largely maintains the status quo from 2025, with many of the lauded benefits manifesting as deductions rather than outright tax eliminations. This nuanced reality has led to an estimated average refund of $3,800 for the current year, an increase of $800 compared to the previous year, with millions of Americans anticipated to receive larger payouts.

Key Deductions and Credits Under the New Legislation

A cornerstone of the new tax law is the substantial increase in the standard deduction, a fixed dollar amount that reduces an individual’s taxable income. This adjustment, part of what has been referred to as the “One Big Beautiful Bill Act,” is expected to benefit the vast majority of taxpayers who opt for this simplified deduction method.

Beyond the enhanced standard deduction, the legislation introduces several new or expanded deductions and credits:

- Senior Bonus Deduction: A new $6,000 deduction is available for individuals aged 65 or older. However, this benefit is subject to income limitations, phasing out for single filers earning over $75,000 and joint filers exceeding $150,000.

- Tip Income Deduction: Restaurant workers and others receiving tips may be able to deduct up to $25,000 in tip income. This deduction also has income phase-outs, beginning at $150,000 for single filers and $300,000 for joint filers.

- Overtime Pay Deduction: A portion of overtime pay can be deducted, capped at $12,500. Crucially, only the ‘premium’ portion of overtime pay—the amount exceeding the regular hourly rate—is eligible for this deduction. For example, if the standard rate is $20/hour and overtime is $30/hour, only the additional $10/hour is deductible. This deduction also comes with income phase-outs.

- New Vehicle Loan Deduction: For new vehicles purchased last year for personal use, a deduction of up to $10,000 may be available, provided the vehicle is manufactured in America. This deduction is also subject to income limitations.

- Child Tax Credit: The maximum benefit for the Child Tax Credit has been increased by $200, bringing it to $2,200 per child. This credit is available for children under 17 at the end of the tax year, provided they have a Social Security number. A significant feature is that it is an “above the line” deduction, meaning it can be claimed in conjunction with the standard deduction, without requiring taxpayers to itemize their deductions. As with other provisions, this credit also phases out for higher earners.

The Role of Withholding and Potential Surprises

The anticipated increase in refunds is partly attributed to an IRS decision to not adjust withholding tables following the implementation of the new tax law. This means that many individuals have been having less tax withheld from their paychecks throughout the year, leading to a larger refund upon filing. However, this also creates a potential pitfall: taxpayers who do not review their withholding might face an unexpected tax bill next April if their withholding was insufficient to cover their final tax liability.

“It’s very important for taxpayers to check what the president has said. What the tax breaks do is reduce your taxable income, and perhaps you will pay less tax, but it’s not an outright elimination of tax for any of those things.”

Financial experts emphasize the importance of proactive tax planning. “To save taxes, you really have to start early in the year and think about the following April 15th,” advises one analyst. “If you do that, then you can save a lot of money.” Checking withholding and adjusting it as necessary is a key step in avoiding surprises and managing tax liabilities effectively.

Market Impact and Economic Outlook

The stated goal behind these tax reforms is to stimulate economic growth. Proponents argue that increased disposable income, reflected in larger refunds and potentially lower tax burdens, will boost consumer spending. The average refund increase of $800, coupled with the prospect of millions receiving more money back, suggests a potential short-term uplift in consumer demand.

However, the broader economic impact remains a subject of debate. The effectiveness of these tax changes in stimulating the economy is closely tied to the persistent issue of affordability facing millions of Americans. If consumers are struggling with the rising costs of everyday goods and services, the additional funds from tax refunds may be absorbed by essential expenses rather than discretionary spending that drives economic expansion.

The legislation’s focus on deductions, particularly those benefiting higher earners, also raises questions about the distributional effects of the tax cuts. While the increased standard deduction and specific credits aim to provide relief across various income brackets, the long-term impact on economic inequality and overall economic stimulus will depend on a complex interplay of consumer behavior, inflation, and broader economic conditions.

What Investors Should Know

For investors, the new tax landscape presents several considerations. The potential for increased consumer spending, particularly if inflation moderates, could benefit sectors reliant on discretionary income. However, the effectiveness of this stimulus is uncertain given current affordability challenges. Investors should monitor economic indicators, such as inflation rates and consumer sentiment, to gauge the real impact of these tax changes on spending patterns.

Furthermore, the complexity of the new deductions and credits underscores the importance of tax-efficient investing strategies. Understanding how these changes might affect individual tax liabilities can inform investment decisions, particularly concerning capital gains and dividend income. The “made in America” provision for the car loan deduction, while specific, signals a potential trend toward incentivizing domestic production, which could be a factor for investors to consider in certain industries.

Ultimately, while the immediate effect of the tax law is likely to be larger refunds for millions, the sustained economic stimulus and its impact on markets will hinge on a broader economic recovery and the ability of consumers to translate their tax benefits into meaningful spending power amidst ongoing affordability concerns.

Source: How Trump's Tax Laws Affect Your Refund (YouTube)

Related Articles

Standard Deduction Dominates: Simplify Your Taxes

A vast majority of taxpayers, 91%, are opting for the standard deduction, highlighting a trend towards tax simplicity. Recent legislative changes have increased the standard deduction threshold, making it the most advantageous choice for most individuals, especially those early in their financial careers.

Tariffs Reignite, Supreme Court Ruling Sparks New Legal Path

Former President Trump's economic address highlighted a renewed focus on tariffs, citing their success in generating revenue and securing trade deals. Despite a Supreme Court ruling, alternative legal avenues are expected to maintain tariff implementation. The speech also detailed tax reforms, investment initiatives, and efforts to control inflation and reduce consumer costs.

AI Picks Surge 14.5% in 6 Months, New Strategy Boosts Gains

An experimental AI stock-picking strategy yielded a 14.5% return in six months, with a new approach of holding winners longer showing even greater profit potential. The experiment highlights AI's market prediction capabilities and the benefits of a diversified, long-term investment outlook.