Tap Home Equity for Real Estate Profits

Homeowners can leverage their equity through cash-out refinances or HELOCs to invest in real estate. The key is ensuring investment returns significantly outweigh borrowing costs. Understanding cash flow and appreciation is vital for profitable strategies.

Unlock Real Estate Returns by Using Home Equity

Many homeowners have a valuable, often untapped, resource sitting in their property: home equity. This is the difference between what your home is worth and what you still owe on your mortgage. Tapping into this equity can be a powerful strategy for real estate investors looking to expand their portfolios. Two popular methods are cash-out refinances and Home Equity Lines of Credit (HELOCs).

Cash-Out Refinance: Trading Up Your Mortgage

A cash-out refinance involves replacing your current mortgage with a new, larger one. You then receive the difference in cash. For example, if your home is worth $400,000 and you owe $200,000, you have $200,000 in equity. You could get a new mortgage for $300,000, taking $100,000 in cash. However, this new mortgage will likely have a higher monthly payment than your old one.

The key to making a cash-out refinance work for investing is ensuring the new investment generates enough income to cover the increased payment. The transcript suggests that borrowing at interest rates below 8% can be profitable if invested wisely. If you take out $60,000 from your equity, you need to invest it in real estate that brings in more than the cost of that borrowed money. This means the property’s rental income should exceed your new, higher mortgage payment plus any other costs associated with the loan.

Home Equity Line of Credit (HELOC): Flexible Access to Funds

A HELOC works differently. It’s like a credit card secured by your home equity. You get approved for a certain amount, and you can draw from it as needed. A major benefit is that you only pay interest on the money you actually use. If you only need $30,000 for a down payment on a property, you only pay interest on that $30,000, not the full amount you were approved for.

This flexibility is crucial. You might find a great deal on a property that requires less capital than you initially anticipated. With a HELOC, you can use just what you need, keeping the rest of your credit line available for future opportunities. You avoid paying interest on unused funds, which can significantly reduce your borrowing costs compared to a cash-out refinance where you pay interest on the entire lump sum from day one.

Understanding Investment Returns: Cash Flow and Appreciation

When considering real estate investments, investors look at several factors to measure success. One is cash flow, which is the money left over after all expenses are paid from rental income. Another is cash-on-cash return. This measures the annual return on the cash invested. For example, if you invest $50,000 in a property and it generates $5,000 in cash flow per year, your cash-on-cash return is 10% ($5,000 / $50,000).

The transcript highlights markets where investors can achieve cash-on-cash returns around 9%. This is considered a strong return in real estate. But the potential gains don’t stop there. Investors also benefit from property appreciation, where the value of the real estate increases over time. Additionally, a portion of each mortgage payment goes towards paying down the principal loan amount, which builds equity and increases your net worth. When these factors are combined—cash flow, appreciation, and principal paydown—the total return can be significantly higher.

The Math Behind Profitable Borrowing

The core principle for profitable real estate investing using borrowed funds is simple: the return on your investment must be greater than the cost of borrowing. The transcript uses an example where money is borrowed at a 6% interest rate. If this money is invested in properties yielding a 9% cash-on-cash return, the investor is making a 3% spread (9% – 6%).

When you factor in appreciation and principal paydown, the total return could reach 25%. In this scenario, you are borrowing at 6% and earning potentially 25%. The difference, or arbitrage, is substantial. Arbitrage is the simultaneous buying and selling of securities, futures, or other financial instruments that profits from a difference in the price. In this real estate context, it means profiting from the difference between your borrowing cost and your investment’s earning potential.

As long as the total return from your real estate investment (cash flow, appreciation, principal paydown) exceeds the interest rate on the money you borrowed to acquire it, you are likely to be in a profitable position. This strategy allows you to make money on the spread, effectively earning more than you pay for the loan. For instance, if your total return is 25% and your borrowing cost is 6%, you have a 19% advantage.

Who Benefits Most?

This strategy primarily benefits homeowners with significant equity who are looking to invest in real estate. It can be particularly attractive to those who understand their local or target investment markets well and can identify properties offering strong cash flow. Buyers seeking to enter the real estate investment market may find these methods useful for securing down payments or purchasing additional properties.

Sellers might benefit indirectly if increased investor activity drives up demand and prices in certain areas. However, the direct advantage lies with the investor who can skillfully use their home’s equity to acquire income-generating assets. It’s crucial for potential investors to understand their risk tolerance and the specific dynamics of the markets they are considering.

Considerations for Investors

While using home equity can be a smart move, it’s not without risks. Borrowing money means taking on debt. If the real estate investment doesn’t perform as expected, you could face financial difficulties. It’s essential to conduct thorough due diligence on any potential property, analyze the numbers carefully, and ensure you have a buffer for unexpected expenses or vacancies.

Understanding concepts like loan-to-value (LTV) ratios, which lenders use to assess risk, and having a clear grasp of potential cash flow versus actual cash flow is vital. Always ensure that the income generated by your investment property comfortably covers your mortgage payments, property taxes, insurance, maintenance, and potential vacancies. The goal is to create positive cash flow that not only covers expenses but also provides a healthy return on your invested equity.

Source: Leverage Your Home Equity: Cash Out Refinance vs HELOC for Real Estate Investing (YouTube)

Related Articles

Buy, Live, Rent: Your Path to Real Estate Wealth

Discover a real estate strategy where you buy a home, live in it, and have tenants pay your mortgage. Learn how instant equity, rental income, and strategic partnerships can turn a small investment into significant wealth.

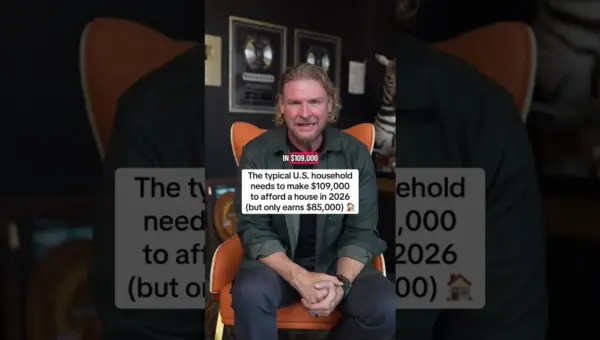

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.

Master 6 Skills for Real Estate Investing Success

Real estate investing doesn't have to be hard. Mastering six key skills—vision, deal flow, underwriting, networking, negotiating, and operations—can transform the process from overwhelming to achievable. Focusing on these fundamentals allows investors to build wealth more effectively.