Small Savings Jump Could Yield Millions More

A modest increase in savings rate, from 4.6% to potentially 25%, can result in millions more dollars by retirement. The analysis shows that even small, incremental savings boosts can dramatically alter long-term wealth accumulation.

Small Savings Jump Could Yield Millions More

A modest increase in your savings rate, even starting small, can lead to millions more dollars by retirement. New analysis reveals that consistently saving just a bit more each year can dramatically alter your financial future, potentially adding millions to your nest egg.

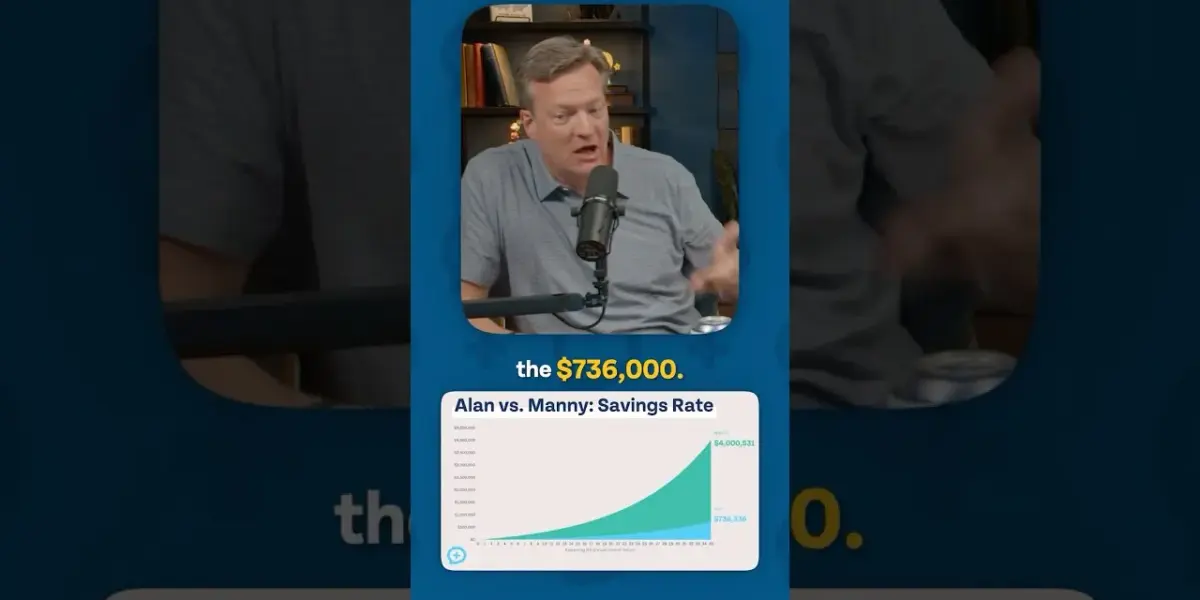

Consider two savers, both starting at age 30. One saves 4.6% of their income, a rate mirroring what many Americans might aim for or achieve. The other saves a more aggressive 25% of their income. By retirement, the 25% saver could amass over $4 million. This significant difference highlights the power of consistent, higher savings.

The situation for the average saver, however, is often less optimistic. The analysis suggests that many typical Americans don’t even reach the $736,000 mark. This figure itself is based on a saving rate that is already considered low. The reality is that many Americans struggle to save consistently, falling short even of this modest goal.

The challenge for many is the perceived leap from a low savings rate, like 4.6%, to a much higher one, such as 25%. It can seem impossible to jump that far all at once. However, the strategy doesn’t require such a drastic immediate change. Instead, it focuses on incremental increases.

Imagine starting by increasing your savings from 4.6% to 5.6%. That’s just a 1% boost. Then, over time, you aim to increase it again, perhaps from 5.6% to 6.6%. This step-by-step approach makes the goal of significantly higher savings much more attainable. You would likely be amazed at how much a little bit extra saved today can grow over time.

Market Impact

This principle has broad implications for personal finance and long-term wealth building. The core idea is that compounding, the process where your earnings also start earning money, works best with time and consistent contributions. Even small amounts, saved regularly and earning returns, can grow exponentially.

For instance, if you earn a consistent return on your investments, say 7% per year, that money starts working for you. Saving an extra 1% of your income might seem small now, but over 30 or 40 years, that extra 1% can translate into tens or even hundreds of thousands of dollars more in retirement. This is because the money you save early has more time to compound.

What Investors Should Know

The key takeaway for investors is the critical importance of starting early and being consistent. The difference between saving 4.6% and aiming for 15% or 20% is substantial. While 25% might be aspirational for many, even aiming for 10% or 15% can make a world of difference.

Consider the time value of money. This financial concept states that money available at the present time is worth more than the same amount in the future. This is due to its potential earning capacity. By saving and investing more now, you maximize this potential. The earlier you start saving, the less you need to save each year to reach the same goal, thanks to the power of compounding.

For example, saving $100 a month for 40 years at a 7% annual return yields significantly more than saving $200 a month for only 20 years. The first scenario benefits from 40 years of compounding, while the second benefits from only 20. This illustrates why starting early is so powerful, even with smaller initial amounts.

The analysis suggests that the biggest hurdle is often psychological – believing that a significant increase is too difficult. Breaking down the goal into smaller, manageable steps can overcome this. Automating these small increases, perhaps by adjusting your 401(k) contribution by 1% each year, can make the process seamless. Many employers offer plans that allow for automatic increases, which can be a powerful tool for long-term savers.

Ultimately, the message is one of empowerment. You don’t need a massive income or a sudden windfall to build substantial wealth. Consistent, disciplined saving, with a focus on gradual increases, is a proven path to financial security. The small changes you make today can indeed add up to a very big difference tomorrow.

Source: The Small Saving Change That Adds Up Big (YouTube)

Related Articles

Couple Balances Separate Finances, Builds Joint Wealth

Nathan and Crissi are navigating a complex financial landscape with separate accounts, newborn twins, and a new business. Their unique approach to wealth building involves adapting the Financial Order of Operations to align individual financial habits with shared goals for independence.

Invest Now: Earnings Growth Signals Buying Opportunities

Strong earnings growth is signaling a prime investment opportunity, urging investors to 'be cool' and avoid market timing pitfalls. Companies like NVIDIA and Apple are highlighted as key players in the AI revolution, while infrastructure plays such as Applied Digital offer further potential.

Your Boring Finances Are Key to Wealth

Building wealth often involves a "mundane middle" phase that, while boring, is crucial for success. Experts advise focusing on consistent saving, tracking progress, celebrating milestones like the "crossover point," and understanding your personal financial 'why' to stay motivated.