Oil Surge Rattles Housing: Rates Climb, Market Slows

Escalating tensions in Iran have sent oil prices soaring, pushing mortgage rates higher and potentially slowing the spring housing market. Buyers face increased borrowing costs, while sellers may see less demand.

Oil Surge Rattles Housing: Rates Climb, Market Slows

The ongoing geopolitical tensions in Iran have sent shockwaves through global markets, and the U.S. housing sector is no exception. A recent surge in oil prices, directly linked to the conflict, has pushed mortgage rates upward, potentially dampening the expected spring housing market recovery.

Oil Prices Spike, Fueling Inflation Fears

In a significant development, crude oil prices have experienced a dramatic increase, jumping over 50% in a matter of just two weeks to hover around $100 a barrel. This sharp rise is a direct consequence of the escalating conflict in Iran, a major oil-producing region. The ripple effect of higher oil prices extends far beyond the energy sector, often leading to increased costs across the broader economy. This inflationary pressure is a key concern for bond markets.

The Chain Reaction: Oil to Mortgage Rates

The connection between oil prices, inflation, and mortgage rates can be understood through a clear economic chain reaction:

- Rising Oil Prices: Increased geopolitical instability in oil-producing regions disrupts supply, driving up the cost of crude oil.

- Increased Inflation Expectations: Higher energy costs translate into higher prices for goods and services throughout the economy, leading investors to anticipate greater inflation.

- Bond Yields Rise: In response to inflation expectations, investors demand higher yields on bonds to compensate for the decreasing purchasing power of their money.

- Mortgage Rates Climb: Mortgage rates are closely tied to the yields on longer-term bonds, particularly the 10-year Treasury note. As bond yields rise, so do the rates lenders offer for mortgages.

Mortgage Rates Rebound After Brief Dip

For a brief period in early March, there was a glimmer of hope for prospective homebuyers as mortgage rates dipped to around 6%. This offered a potential catalyst for a more active spring housing market. However, this trend was short-lived. Following the escalation of the conflict and the subsequent rise in oil prices, mortgage rates have climbed back up to approximately 6.35%. This increase, while seemingly small, can have a significant impact on monthly payments and overall affordability for buyers.

Impact on the Spring Housing Market

The anticipated boost to the spring housing market from falling mortgage rates may now be significantly slowed. Higher borrowing costs can deter potential buyers, leading to a less frenzied market than some had predicted. This could translate into:

- Slower Sales Volume: Fewer buyers may be willing or able to enter the market at higher interest rates, potentially leading to a decrease in the number of transactions.

- Downward Pressure on Pricing: With reduced buyer demand, sellers may need to adjust their price expectations. While a significant price crash isn’t necessarily indicated, a slowdown in appreciation or even modest price corrections in some areas could occur.

- Extended Market Cycles: Homes may take longer to sell as buyers become more cautious and re-evaluate their purchasing power.

Regional Variations and Economic Outlook

The impact of these market shifts will likely vary by region and property type. Markets that are more sensitive to interest rate fluctuations or those that have seen rapid price appreciation in recent years may experience a more pronounced slowdown. Buyers in these areas might find slightly more negotiating power, while sellers might need to be more flexible. Investors will be closely monitoring cash flow and potential returns, as higher financing costs can impact profitability. Concepts like capitalization rates (cap rates), which represent the potential rate of return on an investment property, and loan-to-value ratios (LTV), which compare the loan amount to the property’s value, become even more critical in assessing investment viability in a rising rate environment.

Uncertainty Remains

The duration of the conflict in Iran and its continued impact on oil prices and inflation remain uncertain. If oil prices stabilize or decline, and inflation expectations cool, mortgage rates could potentially decrease, offering some relief to the housing market. However, as long as geopolitical instability persists and oil prices remain elevated, the housing market is likely to face continued headwinds, characterized by slower activity and increased pressure on pricing.

Source: How The War in Iran Impact Real Estate ⛽️🏡 (YouTube)

Related Articles

Iran Missile Strikes Injure US Troops, Raise War Concerns

Iranian missile strikes have injured U.S. service members, escalating tensions as the conflict nears one month. The attacks are raising concerns about the effectiveness of U.S. military strategy and the depletion of crucial missile stockpiles. Global oil prices have surged, impacting economies worldwide.

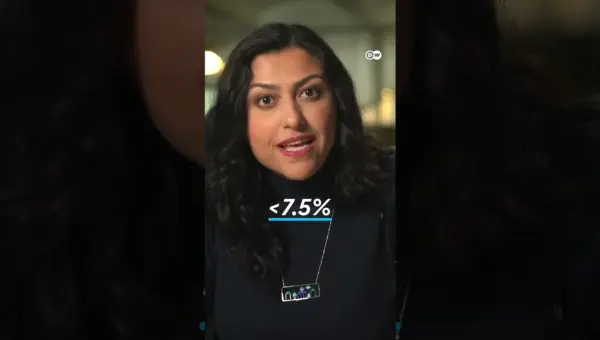

Strait of Hormuz Blockade: Insurance Costs Soar, Ships Stuck

The Strait of Hormuz remains largely blocked despite Iran's claims of openness, with soaring insurance costs acting as a major deterrent for ships. Skyrocketing premiums, from less than 1% to potentially 7.5% of a vessel's value, make transit financially unviable for many. This situation impacts global oil prices and the broader economy, highlighting the complex interplay of geopolitical tensions, insurance markets, and international trade.

Iran Tensions Send Oil Prices Soaring; Farmers Seek Relief

Escalating tensions with Iran are driving oil prices higher, while U.S. troop deployments to the Middle East increase. Meanwhile, American farmers are receiving relief from rising costs through regulatory changes and support measures, as devastating wildfires impact Nebraska's cattle industry.