IRS Boosts AI Audits Despite Agent Cuts

The IRS is significantly increasing its use of AI for tax audits, despite cutting human agents. New AI systems will scan all financial data, including crypto, potentially leading to more audits. Taxpayers need to be aware of red flags like improper deductions, side hustle reporting, and crypto transactions to avoid scrutiny.

IRS Boosts AI Audits Despite Agent Cuts

The Internal Revenue Service (IRS) is set to increase its audit activity, despite a significant reduction in human agents. This shift is powered by new Artificial Intelligence (AI) systems designed to scrutinize tax returns with greater precision. These AI agents will scan W2s, 1099s, bank records, and cryptocurrency exchange data, aiming to identify discrepancies that human agents might miss. This technological leap means taxpayers can expect stricter compliance checks and a higher likelihood of audits, even with fewer human personnel.

Understanding the Audit Process: The DI Score

The IRS uses a system called the DI score to flag tax returns for potential audits. Every tax return receives a DI rating based on factors like income level, how expenses and deductions are claimed, the type of work performed, and its location. Approximately 10% of returns with the highest DI scores are selected for review by IRS agents, and from this group, about 1% are ultimately audited. This DI score is the central mechanism guiding the IRS’s audit selection process.

Key Areas of IRS Scrutiny

The IRS is focusing on several common areas where taxpayers may make errors or attempt to claim deductions that are not fully justified. Being aware of these red flags can help individuals avoid increased scrutiny.

1. Home Office Deductions

Claiming a home office deduction requires careful documentation. If you work from home, you can deduct expenses related to that specific workspace. However, the deduction should only cover the area used exclusively for business. For instance, claiming a large portion of a one-bedroom apartment as a home office, especially if it includes shared family spaces like a kitchen table, can raise red flags. The IRS compares these claims against those of similar taxpayers. To protect yourself, accurately measure your office space and provide evidence that it is used solely for work. Good documentation is crucial for defending such claims.

2. Vehicle Deductions (Section 179)

The tax law allows for significant write-offs on certain heavy vehicles (over 6,000 lbs) under Section 179. This can permit a 100% deduction in the first year of purchase. For example, purchasing a luxury SUV for a business might seem like a straightforward deduction. However, the IRS requires proof that the vehicle is used 100% for business purposes. Personal use, such as trips to the grocery store, disqualifies the vehicle from a full deduction. Maintaining a detailed driving log that distinguishes between business and personal use is essential. Claiming a partial deduction based on documented business usage is a more defensible approach.

3. Cash-Based Businesses

Businesses that primarily deal in cash face increased scrutiny. If a cash-based business reports significantly lower revenue than comparable businesses in the same area, the IRS may suspect unreported income. The temptation to keep cash earnings out of bank accounts to avoid taxes is a common pitfall. Depositing all income and meticulously documenting all financial transactions is the best defense. While it might seem easier to avoid taxes on undeclared cash, the consequences of an audit, including fines and legal fees, can be far more costly.

4. Side Hustle Reporting

New regulations, like those under the One Big Beautiful Bill Act, require platforms such as Etsy, eBay, Venmo, Cash App, and PayPal to report transactions to the IRS. If a seller exceeds $20,000 in revenue or completes 200 transactions on a single platform within a year, the platform will issue a Form 1099 to both the seller and the IRS. It is important to remember that taxes are owed on all income, regardless of whether a 1099 is issued. Mixing personal and business transactions on platforms like Venmo can create confusion and increase audit risk. Maintaining separate business accounts for all side hustles and setting aside a portion of earnings for taxes is highly recommended.

5. Cryptocurrency Transactions

Starting with the 2025 tax year (filed in 2026), cryptocurrency exchanges will be required to report user transactions to the IRS. This means the IRS will have visibility into your crypto buying and selling activity. While exchanges will report the data, it is the taxpayer’s responsibility to calculate and report any capital gains or losses accurately on their tax return. Failing to report income from crypto transactions that the IRS knows about can trigger red flags and lead to audits. This applies to both centralized exchanges and increasingly to decentralized finance (DeFi) platforms and crypto wallets. Diligent record-keeping and accurate reporting are essential.

Higher Earners and Wealth Accumulation

The IRS has stated its intention to increase audit rates for individuals earning over $400,000 annually. While audit rates for those earning less than $400,000 are not expected to decrease, the focus on higher earners is intensifying. As individuals build wealth and diversify their investments and businesses, engaging a qualified accountant becomes increasingly important. While good accountants may have higher fees, they can save significant amounts in taxes, fines, and penalties, and reduce overall stress.

The Rise of AI in Tax Enforcement

The IRS is replacing some human roles with AI agents, which possess advanced capabilities. These AI systems can compare an individual’s tax return against those of similar taxpayers, automatically identifying anomalies in income growth or expense patterns. This comparative analysis is expected to enhance the IRS’s ability to detect discrepancies and increase the precision of audit targeting, even as the agency streamlines its human workforce.

Market Impact and Investor Considerations

The IRS’s move towards AI-driven audits and stricter compliance signals a more complex tax environment for individuals and businesses. Investors and those engaged in side hustles or cryptocurrency trading must be particularly vigilant. The increased reporting requirements from financial platforms and crypto exchanges mean that transparency is paramount. For those with significant income or complex financial dealings, investing in professional tax advice is no longer just a suggestion but a necessity to navigate the evolving landscape and avoid costly penalties. Staying informed through resources like financial newsletters can help individuals keep pace with these regulatory changes and make informed decisions.

Source: The 2026 IRS Crackdown Is Here (How To Not Get Audited) (YouTube)

Related Articles

Fraud Costs Billions: AI and Human Smarts Fight Back

The financial industry faces a massive $300 billion annual loss due to fraud, with false positives costing an additional $600 billion. Elevon's Director of Customer Data Security, Candace Preassenger, explains how advanced AI combined with human intelligence is crucial for fighting sophisticated fraudsters and improving customer experiences. Businesses must view security as a growth strategy, not just a compliance cost, to achieve better financial outcomes.

Standard Deduction Dominates: Simplify Your Taxes

A vast majority of taxpayers, 91%, are opting for the standard deduction, highlighting a trend towards tax simplicity. Recent legislative changes have increased the standard deduction threshold, making it the most advantageous choice for most individuals, especially those early in their financial careers.

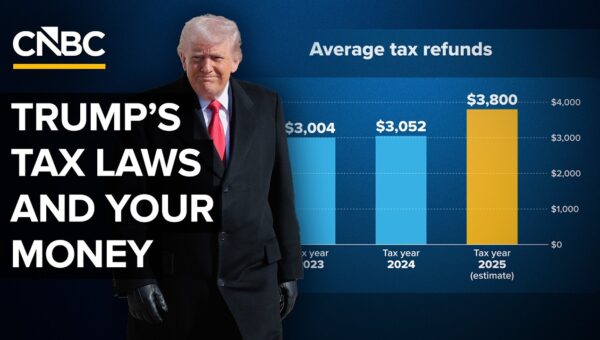

Trump Tax Law Boosts Refunds, But Stimulus Questions Linger

New tax legislation is set to increase average taxpayer refunds by an estimated $800 this year, reaching $3,800. While touted as historic cuts, many benefits are deductions, and economic stimulus hinges on consumer affordability amid rising costs.