Inflation Surge Threatens Housing Market Stability

Inflation is surging again, with prices jumping significantly in a single month. This rise, driven by oil and shipping costs, is expected to keep mortgage rates high and slow down the housing market. Consumers and investors alike will feel the financial pressure.

Inflation Surge Threatens Housing Market Stability

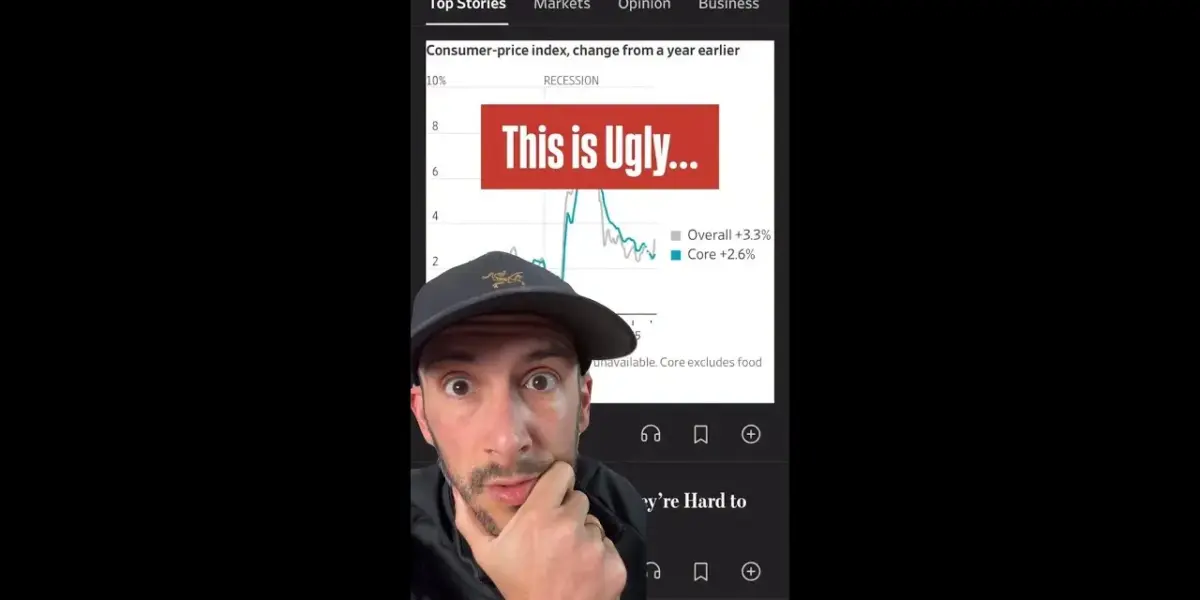

Inflation is heating up again, a troubling sign for homeowners, potential buyers, and the broader economy. The latest figures show inflation jumped from 2.4% to 3.3% in just one month. While this rise was partly expected, it signals that higher prices may be here to stay, potentially worsening the situation for many Americans.

The main driver of this recent increase is soaring gasoline prices. Many have noticed the significant jump at the pump, especially since the conflict in Iran began. Even with a ceasefire in place, oil prices remain about 50% higher than before the war. The Strait of Hormuz, a critical shipping route, is also seeing very little traffic. In the two days following the ceasefire, only 12 ships passed through, a stark contrast to the 135 ships per day typically seen before the conflict. This means oil prices are far from returning to normal, impacting costs across the board.

Oil’s Ripple Effect on Prices

Oil is a key ingredient in countless products, including plastics. As oil prices stay elevated, the cost of plastic goods will likely climb. Furthermore, the increase in shipping costs will make imported goods more expensive for American consumers. Evidence of this can be seen in the Producer Price Index (PPI), which tracks the cost of producing goods. The PPI rose by 7% in a single month, indicating that businesses are facing higher expenses. These increased costs have not yet fully translated to what consumers pay, suggesting further price hikes are on the horizon.

Food and Tariffs Add to Inflationary Pressures

The cost of food is also expected to rise, particularly for imported items. This is partly because 30% of the world’s fertilizer, essential for food production, passes through the Strait of Hormuz. Additionally, existing tariffs continue to significantly influence inflation and pricing within the United States. These combined factors suggest that inflation will remain higher than anticipated.

Impact on the Housing Market and Economy

While a return to the 9% inflation rates seen in 2022 is not expected, the current upward trend will strain Americans already feeling financial pressure. Higher inflation typically leads to higher mortgage rates. This, in turn, slows down the housing market by making it more expensive for people to borrow money to buy homes. The entire economy feels the impact as consumer spending may decrease and business investment could become more cautious. This inflationary environment creates challenges for economic growth and financial stability.

Regional Differences and Who is Most Affected

The effects of persistent inflation are felt differently across regions and demographics. Areas with a higher cost of living may experience a more pronounced impact on household budgets. Buyers looking to enter the housing market will face higher borrowing costs, potentially delaying their purchase plans or forcing them to seek less expensive properties. Sellers might see slower sales or need to adjust their price expectations. Investors will need to carefully evaluate the potential for returns in a market influenced by rising costs and interest rates. Those relying on fixed incomes or whose wages do not keep pace with rising prices will find their purchasing power diminished.

Understanding Key Economic Concepts

To better understand these market dynamics, it’s helpful to know a few terms. Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. Mortgage rates are the interest rates charged on loans used to buy property. When these rates go up, monthly mortgage payments increase, making housing less affordable. The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output. It can be an early indicator of consumer price changes.

For real estate investors, concepts like Capitalization Rate (Cap Rate) and Loan-to-Value (LTV) are important. The cap rate is a quick way to determine the potential return on an investment property. It’s calculated by dividing the net operating income (income after expenses but before debt payments) by the property’s market value. A higher cap rate generally indicates a potentially better return. For example, if a property generates $10,000 in net income and is worth $100,000, its cap rate is 10%. Loan-to-Value (LTV) is the ratio of the loan amount to the value of the property. A lower LTV, meaning you borrow less compared to the property’s value, often means lower risk for lenders and potentially better loan terms for the borrower. For instance, a $100,000 loan on a $125,000 property has an LTV of 80%.

Cash flow refers to the net amount of cash remaining from rental income after paying all operating expenses and debt payments. Positive cash flow means the property generates more income than it costs to run, providing a steady stream of profit. Negative cash flow means the expenses exceed the income, requiring the owner to cover the difference.

As inflation continues to be a concern, understanding these economic factors and their impact on the housing market is crucial for making informed decisions.

Source: Warning: The Inflation Crisis is NOT Over 🚨 (YouTube)

Related Articles

Young Buyers: Buy Two Homes Before 30

Young buyers can acquire two homes before age 30 using a strategy that leverages low down payments and rental income. This method turns a first-time buyer's residence into an investment property, generating cash flow while securing a second home.

Buy This First Rental Property in 2026

Aspiring real estate investors should focus on single-family homes or small multi-family units needing light cosmetic work for their first rental property. Key strategies include targeting C-class neighborhoods, avoiding major repairs, and adhering to the 1% rule for cash flow.

Buttigieg: Trump’s Policies Drive Up Costs for Americans

Former Secretary of Transportation Pete Buttigieg argues that Donald Trump's policies and rhetoric are actively increasing costs for ordinary Americans. He contrasts this with typical administrations that aim to lower inflation, stating that current policies exacerbate economic hardship across various sectors. Buttigieg also addresses Trump's controversial statements, calling them a dangerous erosion of trust.