Home Affordability Crisis: Buyers Demand Falls

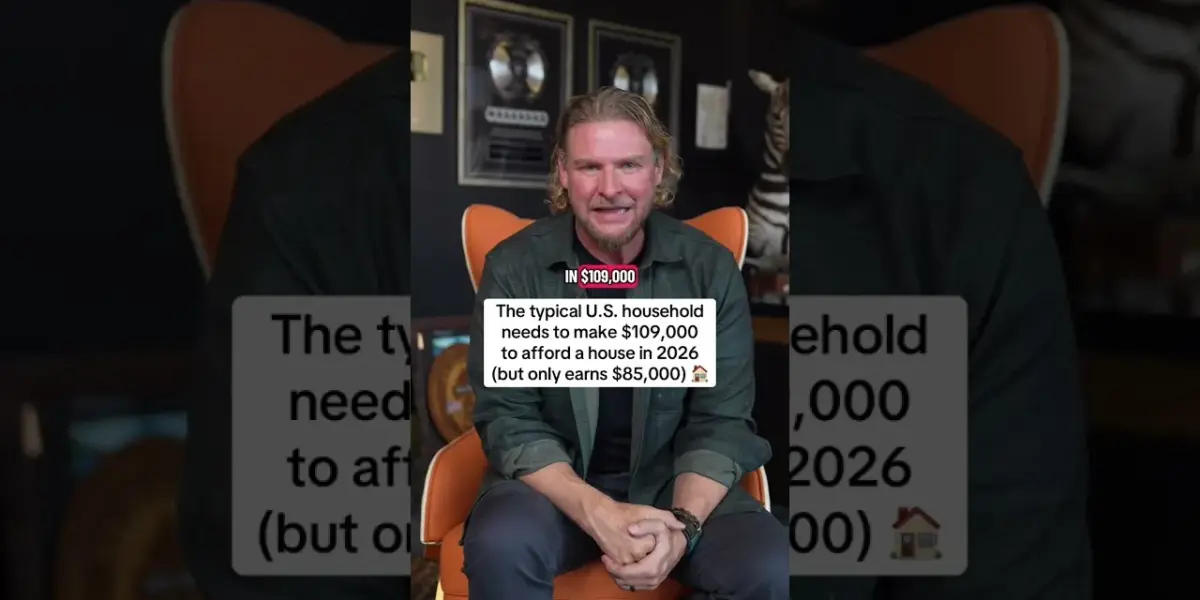

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.

Home Affordability Crisis: Buyers Demand Falls

The dream of homeownership is slipping away for many Americans. A new analysis shows that the typical U.S. household needs to earn $109,000 per year to afford a home. However, the median household income is currently only $85,000. This significant gap creates one of the biggest affordability challenges seen in decades.

This situation echoes tough times in the past. We saw similar affordability pressures during the housing bubble of the mid-2000s. It also brings to mind the early 1980s, a period marked by very high mortgage rates, sometimes reaching 18%. When buying a home becomes this difficult, many potential buyers step back.

This pause in buying activity leads to a deep recession in demand. It’s like a buyer strike, one of the largest in history. As a result, homes may sit on the market longer. This shift can create opportunities for savvy investors who watch these trends closely. They look for situations where reduced competition from hesitant buyers might lead to more flexible sellers.

Understanding Affordability Challenges

Affordability is measured by how much of a household’s income is needed to cover housing costs. This includes mortgage payments, property taxes, and insurance. When home prices rise faster than incomes, or when interest rates climb, affordability drops.

For example, if a home costs $300,000 and a buyer needs a mortgage, the monthly payment depends heavily on the interest rate. A higher interest rate means a larger monthly payment, making the home less affordable. This is why the current gap between income and the required earnings for homeownership is so concerning.

Broader Economic Factors at Play

Several economic factors contribute to this affordability crisis. Inflation can drive up the cost of goods and services, including construction materials. This can increase the price of new homes. At the same time, central banks may raise interest rates to combat inflation. Higher interest rates directly increase the cost of borrowing money for a mortgage.

When mortgage rates go up, even slightly, the monthly payments for buyers increase significantly. This makes it harder for people to qualify for loans or afford the payments on their desired homes. The combination of high prices and increased borrowing costs creates a double whammy for potential buyers.

Impact on Buyers and Sellers

This affordability crunch affects different groups in various ways. For first-time homebuyers, it can be incredibly discouraging. Saving for a down payment is harder, and qualifying for a mortgage becomes more challenging. Many may have to delay their plans or settle for smaller, less desirable homes.

For existing homeowners looking to sell, the market may feel slower. With fewer buyers able to afford homes, sellers might need to be more patient. They may also need to be more flexible on price or terms to attract offers. This can be a difficult adjustment for sellers accustomed to a fast-moving market.

Regional Differences and Investor Outlook

The impact of this affordability crisis is not uniform across the country. Some areas with already high home prices and incomes may see a sharper slowdown. Other regions with more moderate prices might remain more resilient, though still impacted by rising rates.

Investors who understand these market dynamics can look for opportunities. When demand cools, some sellers become more motivated. This can lead to better negotiation possibilities for investors with the capital to act. They might find properties where they can achieve positive cash flow, meaning the rental income covers all expenses and leaves a profit. However, careful analysis of local markets and property performance is crucial.

Looking Ahead

The current housing market faces significant affordability hurdles. The gap between what households earn and what they need to buy a home is widening. This is leading to a slowdown in buyer demand. As the market adjusts, both buyers and sellers will need to adapt to the changing conditions. Investors will likely continue to monitor the situation for potential opportunities, but caution and thorough research are always advised.

Source: The typical U.S. household needs to make $109,000 to afford a house in 2026 (but only earns $85,000) (YouTube)

Related Articles

Iran Talks Gain 10 Days, But Markets Remain Skeptical

Iran has secured a 10-day extension for negotiations, but financial markets remain unconvinced, showing little reaction to the news. Rising energy and borrowing costs, coupled with geopolitical tensions, continue to pressure global markets and consumer spending.

Buy, Live, Rent: Your Path to Real Estate Wealth

Discover a real estate strategy where you buy a home, live in it, and have tenants pay your mortgage. Learn how instant equity, rental income, and strategic partnerships can turn a small investment into significant wealth.

Rate Hike Fears Spark Market Sell-Off, Geopolitics Add Fuel

Markets are reeling as a surprising shift in Federal Reserve expectations, with rate hikes now being priced in, combines with escalating Middle East tensions. This has triggered a liquidity crunch across assets, impacting everything from stocks to bonds and gold.