Equal Weight Funds: A Deeper Look at Risks

Equal weight index funds appear attractive for mitigating market concentration and high valuations, but they come with significant risks including higher volatility, increased turnover, and a systematic drag on momentum. Investors may find more efficient ways to achieve desired factor exposures.

The Allure and Pitfalls of Equal Weight Index Funds

In the quest for investment strategies that deviate from traditional market capitalization weighting, equal weight index funds have garnered considerable attention. Proponents argue they offer a solution to perceived issues like high valuations and market concentration inherent in cap-weighted indexes. However, a closer examination reveals that while equal weighting has historically shown strong performance, it introduces its own set of risks, costs, and inefficiencies that investors must carefully consider.

Understanding the Weighting Difference

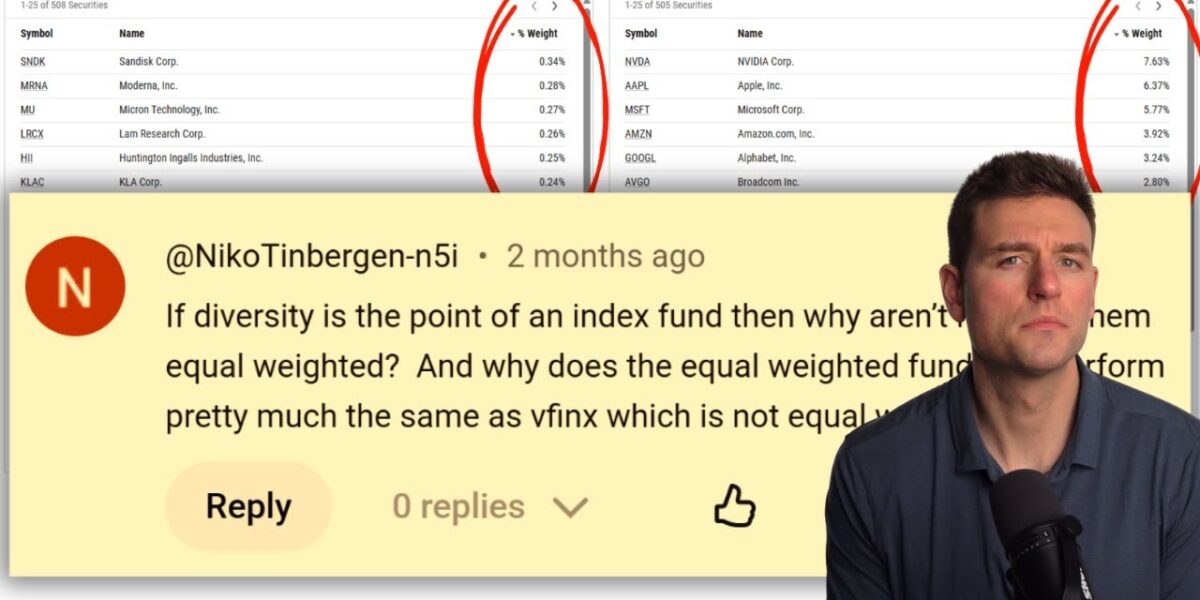

Market capitalization weighting, the standard for most major index funds, assigns a stock’s weight in the index based on its total market value (market capitalization). Larger companies, therefore, command a larger portion of the index. In contrast, an equal weight index fund, as the name suggests, allocates an equal percentage to every stock within the index, regardless of its size.

The logic behind market capitalization weighting is that it passively reflects the market’s collective judgment on company valuations. The market itself dictates the weights. This approach typically requires less frequent rebalancing as the index naturally adjusts with market movements. However, a common criticism, particularly relevant in recent market environments, is that this method can lead to significant concentration in a handful of the largest companies. This concentration, while not historically a strong predictor of future returns, can be a source of investor unease.

Equal Weighting: Performance and Perceived Benefits

Equal weight indexes aim to mitigate this concentration risk. By design, they cannot become overly concentrated in a few large stocks. Furthermore, historical data suggests that equal weighting has outperformed market capitalization weighting over extended periods. For instance, the Invesco S&P 500 Equal Weight ETF (RSP), since its inception in 2003, has shown performance nearly on par with the traditional S&P 500 ETF (SPY), albeit by a narrow margin over the full period.

The appeal of equal weighting is further amplified by current market conditions. With high valuations in the U.S. market relative to historical norms, investors are drawn to strategies that might offer exposure to less expensive segments of the market. Equal-weighted indexes, by underweighting the largest, often highest-valued companies and overweighting smaller ones, naturally exhibit lower aggregate valuations, often reflected in lower price-to-earnings (P/E) and price-to-book (P/B) ratios compared to their cap-weighted counterparts.

The Trade-offs: Risks and Inefficiencies

Despite these apparent advantages, equal weighting comes with significant trade-offs:

Increased Volatility and Risk Exposure

Equal-weighted indexes tend to exhibit higher volatility. Data indicates that the 15-year standard deviation for an equal-weight S&P 500 index is notably higher than for a market-cap-weighted index. Beyond volatility, equal weighting often leads to greater exposure to factors like small-cap and value stocks. While these factors can be beneficial, the extreme over- and underweights in an equal-weighted portfolio can be considered riskier than the concentration in large-cap stocks found in cap-weighted portfolios.

Sector Skew and Bets

Equal weighting can lead to material differences in sector exposures compared to market capitalization-weighted indexes. For example, an equal-weighted S&P 500 index might significantly underweight technology and overweight industrials. These sector tilts can be viewed as unintended bets on specific sectors, which can be difficult for investors to manage and may not align with their overall investment objectives.

Rebalancing Costs and Turnover

Maintaining equal weights necessitates more frequent and aggressive rebalancing. When a smaller company grows significantly or a larger company shrinks, the index must trade to restore the equal weighting. This results in substantially higher portfolio turnover. The Invesco S&P 500 Equal Weight ETF, for instance, has demonstrated average annual turnover more than ten times higher than its market-cap-weighted counterpart. This high turnover incurs significant explicit and implicit trading costs, which are ultimately borne by the fund’s investors.

Systematic Bet Against Momentum

Perhaps one of the most significant, yet less discussed, drawbacks of equal weighting is its inherent nature as a negative momentum strategy. Momentum investing is based on the observation that stocks that have performed well recently tend to continue to do so, and vice versa. To maintain equal weights, an equal-weighted index must systematically sell recent winners (which have grown larger) and buy recent losers (which have shrunk). Statistical analysis, such as multi-factor regressions, reveals that equal-weighted S&P 500 funds exhibit significant negative loadings on the momentum factor, alongside positive loadings on size and value factors.

Alternative Approaches: Dimensional Fund Advisors

For investors seeking exposure to factors like small-cap and value stocks without the drawbacks of equal weighting, strategies offered by firms like Dimensional Fund Advisors (DFA) present an alternative. DFA funds aim to systematically target these desired factor exposures through a more intentional and controlled approach.

These strategies, such as the Dimensional US Core Equity 1 Fund (available through financial advisors and as an ETF), offer similar factor tilts to equal-weighted funds but with key differences:

- Controlled Sector Exposure: DFA caps sector weight differences to avoid large, unintended sector bets.

- Momentum Management: Unlike equal-weighted funds, DFA’s trading rules are designed to avoid selling recent winners and buying recent losers, thus mitigating negative momentum exposure.

- Minimized Turnover: By using market capitalization weights as a starting point and applying modest tilts, DFA funds achieve lower portfolio turnover compared to equal-weighted strategies. This reduces trading costs and inefficiencies.

While backtested data and live fund performance suggest that DFA’s approach can achieve similar factor exposures with potentially better risk management and lower costs, it’s crucial to remember that backtests are not guarantees of future results and do not fully capture real-world implementation costs.

Market Impact and Investor Considerations

Equal-weighted index funds offer an appealing alternative for investors concerned about market concentration and high valuations. The historical outperformance and current market dynamics make them seem like a logical choice. However, the increased volatility, higher turnover, trading costs, and systematic bet against momentum are significant factors that can detract from long-term returns.

Investors looking to gain exposure to smaller and cheaper stocks—a historically rewarded strategy—may find more efficient pathways than broad equal weighting. Strategies that intentionally tilt towards these factors while managing sector exposures, minimizing turnover, and avoiding a systematic drag from momentum may offer a more robust solution for achieving desired investment outcomes over the long term.

The strong past returns of equal weighting are largely explained by tilts towards smaller and lower-priced stocks rather than some magic from equal weights. The implication for investors is that if you want to tilt towards smaller and lower-priced stocks, which is a reasonable thing to want to do, you can do it without introducing all of the downsides of equal waiting.

Source: The Problem with Equal Weight Index Funds (YouTube)

Related Articles

US Housing Markets Facing Declines and Risks

Several US housing markets are experiencing significant price declines and rising inventory, leading to increased risk for homeowners and investors. From Asheville, NC, to Austin, TX, these areas are grappling with market corrections and underwater mortgages.

Alberta Separatism: Economic Realities vs. Grand Promises

Proponents of Alberta separatism promise fiscal utopia, but economic analysis reveals significant risks and unaddressed costs. Examining the arguments around transfer payments, the Canada Pension Plan, and the practicalities of secession highlights the complex financial realities confronting the movement.

Jane Street’s Bitcoin ETF Role Sparks Price Manipulation Fears

Powerful trading firm Jane Street, one of four APs for BlackRock's Bitcoin ETF, faces scrutiny over alleged daily Bitcoin price manipulation. Past regulatory actions and a lawsuit over the Terra collapse add weight to these concerns, highlighting the risks of investing in crypto via traditional financial products.