Dual-Income Trap: Why Two Paychecks Aren’t Enough

Dual-income households, despite earning significantly, often find themselves financially strained due to taxes, childcare, and lifestyle inflation. This article explores why two paychecks may not be enough and how to rebuild financial margin for true security.

Dual-Income Trap: Why Two Paychecks Aren’t Enough

In today’s economic landscape, a dual-income household is often seen as the bedrock of middle-class stability. However, a closer examination reveals a more complex reality: for many, two incomes have become a necessity just to maintain a standard of living that a single income once afforded, leaving them with precarious financial margins. This phenomenon, often referred to as the “dual-income trap,” means that even households earning significantly above the national average can find themselves unable to cover unexpected expenses, highlighting a structural issue rather than individual financial mismanagement.

The Illusion of Prosperity

Consider a hypothetical couple earning a combined $128,000 annually, placing them in the top 25% of American households. Despite their responsible financial habits—driving modest, aging vehicles, packing lunches, and prioritizing decent schools for their children—a sudden furnace repair forced them to rely on a credit card. This scenario, far from being an anomaly, illustrates a widespread trend where two full-time incomes barely cover essential expenses and leave no buffer for emergencies. This situation is particularly disorienting for those who diligently follow conventional financial advice, earning good money yet finding little left over for savings or investments.

Historical Context: The Single-Income Advantage

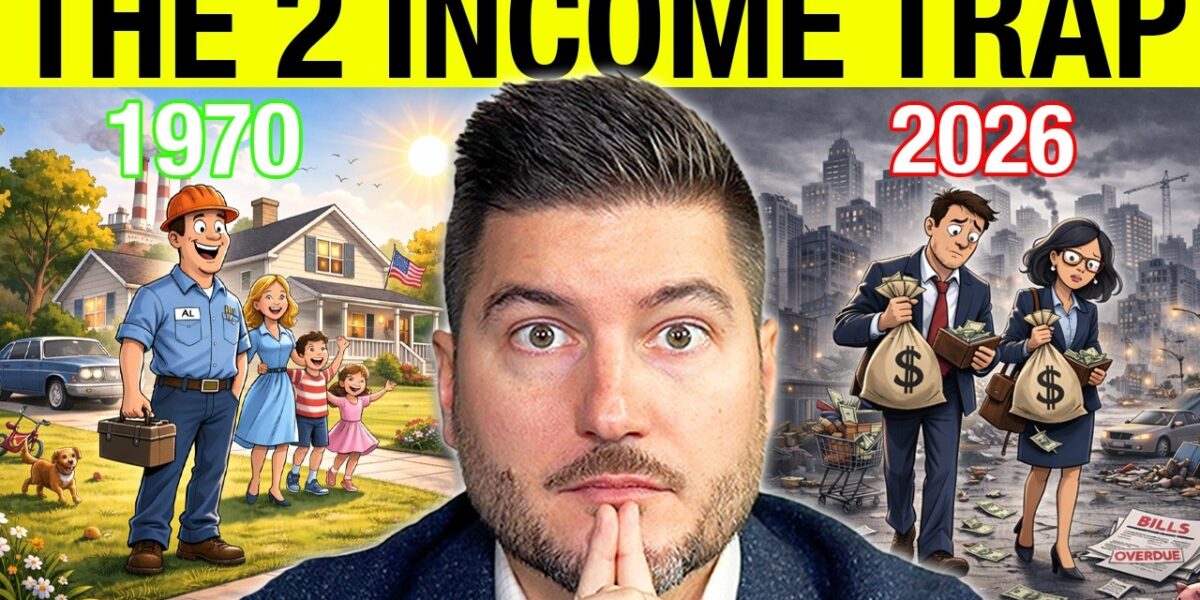

To understand the current predicament, one must look back to the 1970s. In that era, a single-income household, typically with the father as the primary earner and the mother managing the home, was often sufficient. A median single-income family could afford a median-priced home, dedicating around 25% of their income to housing—well within the recommended 30% threshold. This left room for other expenses, savings, and even vacations. Crucially, the non-working spouse served as a built-in financial reserve. Should the primary earner face job loss or illness, the other parent could enter the workforce, providing a vital safety net.

The Shift to Dual Incomes

Over the decades, female workforce participation has significantly increased, rising from approximately 43% in 1970 to over 57% today, with even higher rates among married mothers. This shift transformed the stay-at-home parent’s role from a financial reserve to an essential component of the household’s daily operational income. What was once an emergency backup plan became the standard operating procedure. Consequently, dual-income families now have both partners fully engaged in the workforce, leaving no one on the “bench” when unforeseen circumstances arise.

The Mechanics of the Trap

The core of the dual-income trap lies in how incomes are taxed and spent. When a second income is added to a household, it’s not taxed from the bottom up but rather stacked on top of the first income, pushing it into higher marginal tax brackets. This means a significant portion of the second income is immediately lost to federal, state, and payroll taxes. For instance, a $55,000 second income might only net around $37,500 after taxes due to higher marginal rates.

Beyond taxes, the costs associated with maintaining two careers escalate rapidly:

- Childcare: The national average for one child in daycare can exceed $15,000 annually, a cost that doubles in major metropolitan areas.

- Transportation: Most dual-income households require two vehicles, incurring costs for car payments, insurance, fuel, maintenance, and depreciation, conservatively estimated at $8,500 per year.

- “Exhaustion Spending”: The sheer fatigue of managing full-time jobs, commutes, and childcare often leads to increased spending on convenience services like takeout, pre-prepared meals, and house cleaning, adding an estimated $7,500 annually.

After accounting for these expenses, the net gain from the second income can shrink dramatically. In the example provided, a $55,000 second income could leave as little as $6,500 per year, or roughly $3 per hour, once all associated costs are deducted. Adding a second child can eliminate this surplus entirely, potentially pushing the household into deficit.

Housing Costs and the Arms Race

The housing market plays a particularly insidious role. As dual-income households became the norm, their increased purchasing power drove up demand and prices, especially in desirable areas with good public schools. This created an “arms race” where two incomes became the minimum requirement to afford what one income once could. Median home prices have roughly doubled relative to inflation since 1970. Consequently, families stretch their budgets to secure homes in neighborhoods with good schools, often trading a higher mortgage payment for the equivalent of private school tuition over 30 years. Once this mortgage is secured, the trap snaps shut, locking the household into a payment structure that necessitates both incomes indefinitely.

The Zero Margin Reality

A 2019 Federal Reserve study highlighted the precarious financial state of many Americans, finding that 40% could not cover a $400 emergency expense without borrowing or selling assets. This statistic is alarming because it includes many middle- and upper-middle-class households with dual incomes, seemingly stable lives, and visible signs of prosperity. The lack of a financial cushion stems from a cost structure built on the flawed assumption of continuous, uninterrupted income flow. Unlike the single-income households of the past with their built-in shock absorbers, today’s dual-income families have exhausted their flexibility, leaving them vulnerable when life inevitably presents unexpected challenges.

Market Impact and Investor Considerations

The dual-income trap underscores a fundamental shift in economic security. What was once considered financial security—achieved through high earnings—is now increasingly defined by having options. The “freedom gap,” the difference between what a household earns and what it needs to survive, represents this crucial margin. Households that have closed this gap by committing both incomes to fixed costs and lifestyle inflation have little flexibility.

What Investors Should Know:

- Re-evaluate Financial Foundations: The traditional advice to maximize earning potential needs to be balanced with building a financial structure that can withstand shocks. This might involve intentionally living on one income’s worth of earnings and directing the second income towards savings, investments, and debt reduction.

- The Value of Margin: True financial security is not just about accumulating wealth but about maintaining flexibility. The ability to absorb unexpected expenses, reduce work hours, or change careers without catastrophic financial consequences is paramount.

- Long-Term Perspective: Building substantial savings, retirement funds, and investment portfolios from the “second income” can create a financial resilience that appears absent in many high-earning dual-income households. This approach prioritizes long-term options over immediate consumption.

- Appearance vs. Reality: Maintaining an appearance of wealth through larger homes or newer cars, funded by dual incomes that are already committed, does not equate to genuine financial security. True wealth lies in having choices and the ability to navigate life’s uncertainties.

Building a Resilient Future

The path forward requires a deliberate shift in financial strategy. For households trapped in the dual-income cycle, the goal is to reconstruct margin. This involves structuring fixed costs—mortgage, car payments, essential bills—to be manageable on a single income. It may necessitate lifestyle adjustments, such as purchasing a less expensive home or reducing vehicle expenses. The second income, freed from covering baseline costs, can then be directed towards building an emergency fund (3-6 months of expenses), maxing out retirement accounts, and investing in taxable accounts.

Over a 5-10 year period, this strategy can compound, leading to genuine financial security rather than just high earnings. The ultimate goal is to create a “freedom gap”—the margin that provides options: the ability for a partner to reduce hours, weather a medical crisis without panic, or pursue a career change. This mirrors the financial resilience often found in earlier generations who, despite earning less, possessed greater flexibility and the capacity to absorb economic shocks.

Ultimately, the families that thrive financially are not always those with the highest incomes, but those who maintain their options. By prioritizing margin and flexibility over immediate consumption and the appearance of prosperity, individuals can build a more secure and resilient financial future.

Source: Why Two Incomes Made the Middle Class Poorer (YouTube)

Related Articles

$100K Salary Illusion: Why You’re Not Richer

A $100,000 salary, once a symbol of financial achievement, now often leaves individuals feeling surprisingly strained. This article explores how inflation, taxes, psychological spending pressures, and a misunderstanding of income versus wealth contribute to this modern financial paradox, offering strategies to build a sustainable margin.

Mastering Wealth: The 5 Levels of Financial Progression

Building wealth follows a structured path, starting with the fundamental principle of living on less than you make. Experts identify five levels of financial progression, emphasizing discipline and strategic saving as keys to long-term security.

Standard Deduction Dominates: Simplify Your Taxes

A vast majority of taxpayers, 91%, are opting for the standard deduction, highlighting a trend towards tax simplicity. Recent legislative changes have increased the standard deduction threshold, making it the most advantageous choice for most individuals, especially those early in their financial careers.