Covered Calls: The Illusion of Income

Analysis reveals that covered call funds, despite their promise of passive income, systematically underperform underlying equities. These strategies cap upside potential, offer limited downside protection, and may lead to lower long-term wealth accumulation for investors.

Covered Calls: The Illusion of Income

The proliferation of covered call funds, particularly among retail investors, has raised concerns among financial professionals about their suitability and long-term impact on wealth accumulation. Despite marketing that emphasizes passive income, analysis suggests these products may systematically lower expected returns and increase risk compared to simply holding the underlying equities.

Understanding Covered Calls

A covered call strategy involves selling a call option on a stock that an investor already owns. This grants the buyer the right, but not the obligation, to purchase the stock at a specified price (the strike price) before the option expires. In exchange for selling this right, the investor receives a premium.

The payoff of a covered call strategy is contingent on the future price of the underlying stock. If the stock price remains below the strike price plus the premium received, the investor generally fares better than simply holding the stock, as they pocket the premium. However, if the stock price rises significantly above the strike price, the investor’s upside potential is capped. While they still profit from the stock’s appreciation up to the strike price plus the premium, they forgo any gains beyond that point. On the downside, the premium offers only a marginal buffer against losses, leaving the investor largely exposed to the stock’s price decline.

Performance Against Underlying Equities

Empirical data reveals a consistent pattern of underperformance when comparing covered call funds to their underlying equity benchmarks. For instance:

- The Global X S&P 500 Covered Call ETF has underperformed the iShares Core S&P 500 ETF by an annualized 3.15% since January 2014.

- The Global X S&P TSX 60 Covered Call ETF has lagged the iShares S&P TSX 60 ETF by 3.81% annually since March 2011.

- The BMO Covered Call Canadian Banks ETF has trailed the BMO Equal Weight Banks ETF by 2.86% per year since February 2011.

These figures assume the reinvestment of distributions, a critical factor given the high yields often advertised by covered call funds.

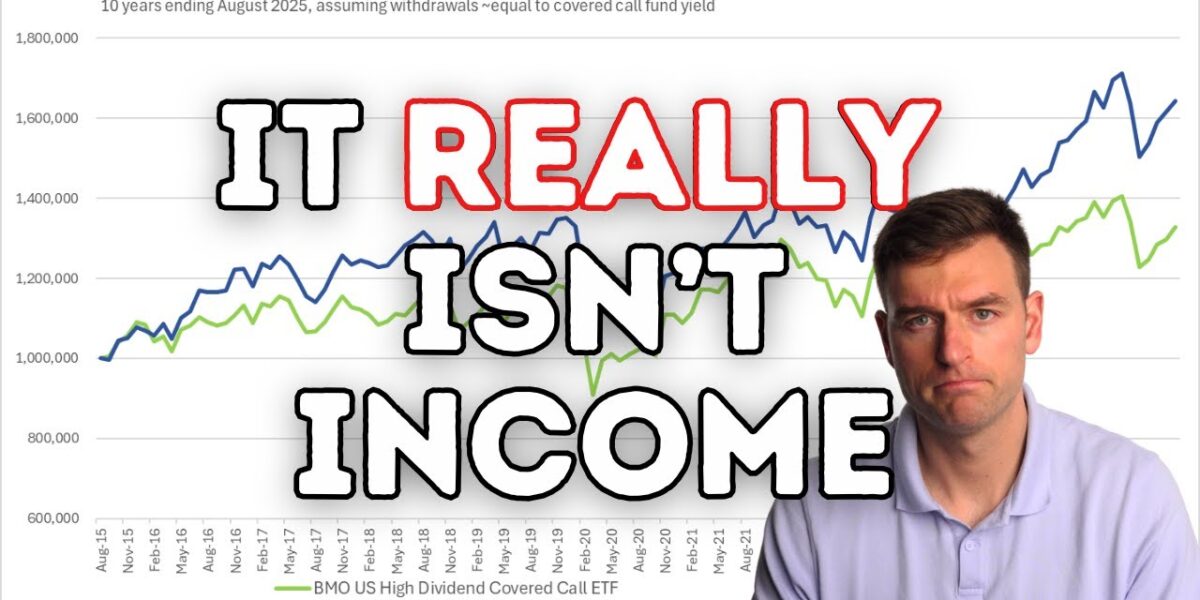

Withdrawal Analysis for Income-Oriented Investors

A common argument in favor of covered calls is their ability to generate income for investors who need to draw from their portfolios. To test this, a 10-year withdrawal analysis was conducted, comparing covered call funds with their underlying equity counterparts. In this model, investors withdrew the same dollar amount each month from both types of portfolios. The covered call investor received income primarily through fund distributions, while the underlying equity investor funded withdrawals through a combination of dividends and share sales.

The results indicated that even when funding consumption needs, investors in underlying equities consistently ended up with more capital. After 10 years, the underlying equity portfolios held, on average, 26% more capital than their covered call counterparts, despite identical monthly spending. This suggests that the perceived income from covered calls comes at a significant cost to total wealth accumulation.

Implied Costs and Risk Exposure

The underperformance of covered call strategies can be quantified by estimating the implied costs. Analysis suggests that to match the ending wealth of the underlying equity portfolios, investors would have effectively paid an implicit fee ranging from 1.5% to 2.7% for the covered call strategy.

Furthermore, covered calls alter risk exposure by capping upside potential while leaving downside risk largely intact. This asymmetric risk profile is akin to holding a significant portion of a portfolio in cash. Simulations indicated that holding cash allocations between 19% and 36% in a traditional equity portfolio could yield similar ending wealth outcomes as a covered call strategy, with the added benefit of reduced downside risk exposure.

Broader Market Data and Enhanced Products

An examination of 20 Canadian-listed covered call ETFs with comparable underlying equity ETFs further corroborated these findings. On average, these covered call funds underperformed their benchmarks by an annualized 3.25%, with a median underperformance of 2.96%. Only two out of the 20 funds managed to outperform, and these were technology-focused funds with short track records and imperfectly matched underlying portfolios.

The analysis also touched upon ‘enhanced’ covered call funds, which employ leverage in addition to the covered call strategy to boost yields. While leverage amplifies both gains and losses, these enhanced funds have generally underperformed the underlying equities, particularly during downturns. In scenarios where investors are comfortable with leverage and volatility, directly leveraging the underlying equity is shown to be a more effective strategy than leveraging a covered call strategy.

The Role of Financial Advice and Information Sources

Concerns have been raised about the marketing of covered call funds, with some content creators promoting these products being sponsored by the very companies that issue them. This creates a potential conflict of interest that investors should be aware of.

Professional financial advisors emphasize that wealth management encompasses more than just income generation. Key areas include goal setting, asset allocation, cash flow planning, insurance, product selection, and tax efficiency. While covered calls might appear to address cash flow planning, they do so at the expense of long-term total returns and can introduce unnecessary complexity and risk.

Conclusion

For long-term investors, covered call funds appear to offer an illusion of income at the cost of reduced long-term returns and potentially increased risk. The strategy caps upside potential without providing commensurate downside protection, undermining the power of compounding and mean reversion inherent in equity markets. Investors seeking income are generally better served by creating their own income streams through dividends and strategic share sales from a diversified portfolio of underlying equities.

Source: Was I Wrong About Covered Calls? (YouTube)

Related Articles

AI Disruption: Boom or Bust for Markets?

A new analysis presents two starkly different futures for the economy driven by AI: a potential 40% market crash and widespread job losses, or an era of unprecedented abundance. The debate highlights the profound uncertainty surrounding AI's ultimate economic impact.

Navigating Real Estate: Avoiding High-Risk Markets

High regulatory burdens, particularly concerning eviction laws, can pose significant risks for real estate investors. Understanding these market dynamics is crucial for protecting investments and ensuring sustainable returns.

BlackRock Warns of Looming Retirement Crisis

BlackRock CEO Larry Fink warns that most Americans are unprepared for a looming retirement crisis, needing $2.1 million for comfortable retirement. With 62% having less than $150,000 saved, and 401(k)s often underperforming and charging high fees, individuals face a significant savings gap.