Covered Calls: The Deceptive Yield Trap

Covered call strategies, often marketed for their high distribution yields, present a deceptive income trap for investors. Analysis shows these strategies mechanically reduce expected returns, cap upside potential, and fail to deliver sustainable income, leading to consistent underperformance against underlying equities.

Covered Calls: The Deceptive Yield Trap

The allure of passive income is a powerful behavioral bias in investing, often leading investors to pursue strategies that promise high distributions. However, a closer examination of covered call strategies reveals that this pursuit of income can be a ‘devil’s bargain,’ leading to underperformance and increased risk for long-term investors.

Understanding Covered Calls and Distribution Yields

A covered call strategy involves owning an underlying equity and selling call options against it. Selling a call option grants the buyer the right, but not the obligation, to purchase the underlying asset at a predetermined price (the strike price) before the option expires. In return, the seller receives a premium. Covered call funds typically distribute this premium income to investors, marketing it as a high distribution yield.

While these distributions may feel like investment returns, they represent a fundamental misunderstanding of how covered calls function. The premium received is compensation for taking on a liability: the obligation to sell the underlying stock at the strike price if it rises above that level. This caps the potential upside gains while leaving the downside risk largely intact.

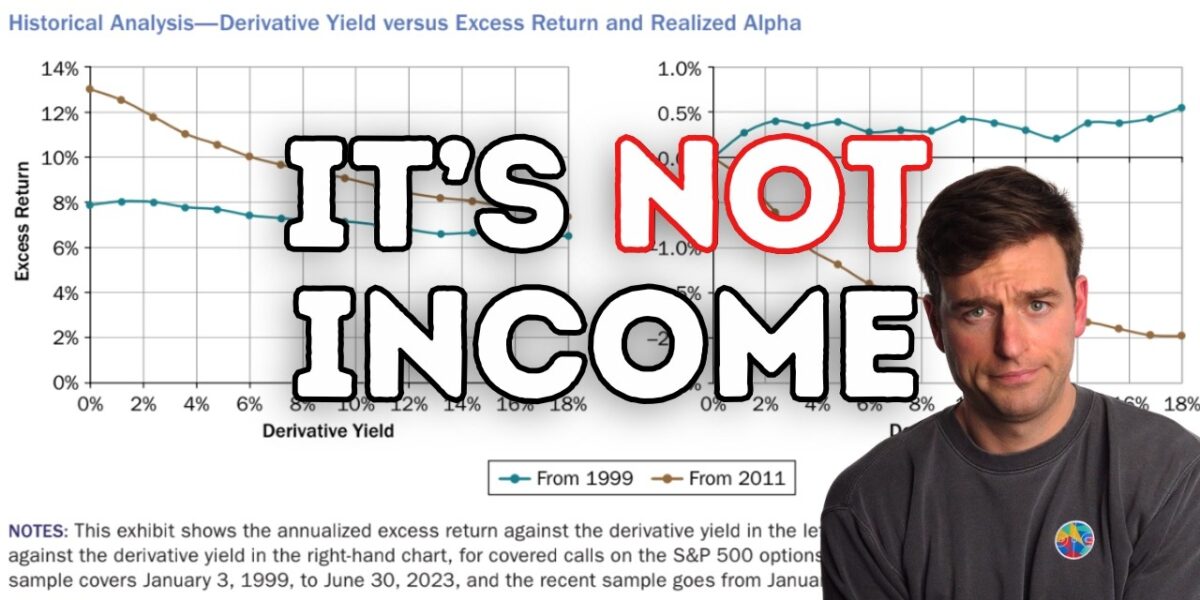

The Inverse Relationship Between Yield and Expected Returns

The core issue with covered call strategies, as highlighted by Ben Felix, Chief Investment Officer at PWL Capital, is the inverse relationship between distribution yields and expected total returns. Selling call options reduces an investor’s exposure to the underlying equity, measured by a concept called ‘delta.’ To generate higher income (higher distribution yields), investors or funds often sell options with lower strike prices, which have a higher delta. This means that a higher yield is mechanically linked to lower exposure to the underlying asset’s potential gains, thereby reducing expected total returns.

“Higher yields mechanically mean lower exposure to the underlying asset by being short a higher delta option and correspondingly it means lower expected returns.”

Total returns, which encompass both capital appreciation and income, are what ultimately matter for investors to meet their financial goals, such as purchasing necessities. Marketing high distribution yields as expected returns is not merely misleading; it is an indifference to the truth, as it ignores the inherent trade-off between yield and overall return potential.

Asymmetric Risk and the Elimination of Mean Reversion

For long-term investors, covered calls present a particularly risky profile due to their asymmetric nature. Investors retain most of the downside risk of owning the underlying stock but have their potential upside gains capped at the strike price. This means that during periods of market downturns, investors experience the full brunt of the losses, but during market recoveries, they miss out on a significant portion of the gains.

Historically, stocks have exhibited a degree of ‘mean reversion’ – a tendency to rebound after periods of poor performance. This characteristic has made equities, over the long term, less risky than bonds for investors relying on their portfolios for income. Covered calls, by capping upside potential, effectively eliminate this beneficial mean-reverting tendency. This can be particularly detrimental during market recoveries, which are crucial for compounding wealth over extended periods.

The Volatility Risk Premium: A Limited Savior

One theoretical benefit of selling options is the ‘volatility risk premium’ (VRP). Options are often priced with an implied volatility that is higher than the actual realized volatility of the underlying asset. Option sellers can, in theory, earn a premium for taking on the risk that realized volatility might exceed implied volatility. While back-tested covered call strategies have appeared attractive in recent years, the VRP has not been sufficient to offset the reduction in equity exposure since approximately 2011.

Furthermore, covered call funds are typically marketed based on their distribution yields, not their exposure to the VRP. This marketing approach, especially when juxtaposed with the inverse relationship between yield and expected returns, is seen as particularly problematic.

Empirical Evidence: Live Fund Performance

The theoretical concerns are borne out by the performance of actual covered call exchange-traded funds (ETFs). A review of several ETFs with at least a 10-year history demonstrates consistent underperformance compared to their underlying equity benchmarks:

- The BMO Covered Call Utilities ETF (launched Oct 2011) has trailed its underlying equity ETF by an annualized 2.6 percentage points since inception. It has underperformed in over 70% of three-year rolling periods.

- The BMO Covered Call Canadian Banks ETF (launched Jan 2011) has underperformed its underlying ETF by an annualized 2.71 percentage points since inception, outperforming in less than 1% of rolling three-year periods.

- The Global X S&P/TSX 60 Covered Call ETF (launched Mar 2011) has trailed its benchmark by 3.65 percentage points since inception and has underperformed in 92% of three-year rolling periods.

These figures highlight that even in relatively stable market conditions, covered call strategies consistently lag their benchmarks over the long term. The underperformance is exacerbated when underlying equities experience sharp downturns followed by recoveries, precisely the scenarios where capping upside is most damaging.

The Perils of Maximizing Yield

Strategies that aggressively target higher yields, such as those employing lower strike prices or selling at-the-money options, amplify the negative effects. For example, Hamilton ETFs’ US Equity Yield Maximizer ETF targets a 12% distribution yield and has underperformed an S&P 500 ETF by an annualized 4.48% over its short history.

Single-stock covered call ETFs, such as TSLY, which writes covered calls on Tesla, showcase the most extreme examples. TSLY boasts a distribution yield of over 48% but has underperformed Tesla by more than 20 percentage points annualized since its inception in November 2022. This starkly illustrates the inverse relationship between ultra-high yields and expected returns.

Costs and Investor Beware

Beyond the inherent performance drag, covered call funds typically incur higher fees and transaction costs than their underlying equity counterparts. The average management expense ratio (MER) for a sample of covered call ETFs (excluding single-stock funds) was 0.63%, with an additional 0.16% for trading expenses. This compares to an average MER of 0.25% and 0% trading expenses for funds holding only the underlying equities.

Investors are paying a premium for a strategy that limits upside potential and retains significant downside risk, while offering distributions that are often unsustainable and not true income. The notion of borrowing money at a lower interest rate to invest in a covered call fund with a high distribution yield is particularly perilous, as the capital depletion can occur rapidly when distributions are not supported by genuine returns.

Market Impact and What Investors Should Know

The proliferation of covered call strategies, particularly those marketed aggressively on high yields, poses a significant risk to retail investors. These products can create a false sense of security and income generation, masking the underlying erosion of capital over the long term.

- High Distribution Yields are Not Guaranteed Income: Premiums from selling options are not the same as bond interest or dividends. They come with liabilities that reduce total expected returns.

- Capped Upside, Uncapped Downside: Covered calls limit your ability to participate in market rallies while leaving you exposed to significant losses.

- Eliminates Mean Reversion: This strategy removes a key characteristic that historically has made stocks less risky over the long term.

- Underperformance is the Norm: Real-world data from numerous covered call ETFs shows consistent underperformance against their underlying benchmarks over extended periods.

- Higher Fees: Investors pay more for a strategy that offers inferior risk-adjusted returns.

For long-term investors focused on wealth accumulation and preservation, covered calls are generally ill-suited. The strategy offers little beyond what could be achieved by simply holding the underlying equity and a portion of cash, but with the added disadvantage of capped upside. The pursuit of high distribution yields through covered calls can lead investors into a deceptive trap, sacrificing long-term growth for the illusion of immediate income.

Source: Covered Calls: A Devil's Bargain (YouTube)

Related Articles

AI Disruption: Boom or Bust for Markets?

A new analysis presents two starkly different futures for the economy driven by AI: a potential 40% market crash and widespread job losses, or an era of unprecedented abundance. The debate highlights the profound uncertainty surrounding AI's ultimate economic impact.

Navigating Real Estate: Avoiding High-Risk Markets

High regulatory burdens, particularly concerning eviction laws, can pose significant risks for real estate investors. Understanding these market dynamics is crucial for protecting investments and ensuring sustainable returns.

BlackRock Warns of Looming Retirement Crisis

BlackRock CEO Larry Fink warns that most Americans are unprepared for a looming retirement crisis, needing $2.1 million for comfortable retirement. With 62% having less than $150,000 saved, and 401(k)s often underperforming and charging high fees, individuals face a significant savings gap.