Covered Calls: A Costly Illusion for Investors

Covered call strategies, while appealing for their income generation, are criticized for hindering long-term wealth growth by limiting upside participation. Despite some downside protection, historical data and detailed analyses show these funds often underperform broader market indexes over time, making them a potentially costly illusion for investors.

Covered Calls: A Costly Illusion for Investors

In a financial landscape increasingly populated by complex products promising enhanced income and returns, covered call strategies are experiencing a resurgence, particularly in Canada. However, a growing chorus of market analysts, including Ben Felix, Chief Investment Officer at PWL Capital, warns that these instruments, while psychologically appealing, often lead investors astray, hindering long-term wealth accumulation despite their income-generating facade.

The Allure of Income vs. Long-Term Growth

The fundamental appeal of covered call strategies lies in their ability to generate income through the sale of call options on underlying assets. This income, often distributed as yield, is attractive to investors seeking regular payouts, especially in retirement. However, Felix argues that this perceived benefit comes at a significant cost: the suppression of long-term capital appreciation. He contends that the premiums generated by selling options, while providing a buffer in down markets, severely limit upside participation during market recoveries, ultimately leading to a diminished overall wealth trajectory.

“Capitalists respond to the actual demand for their products, not the demand that would exist if people were perfectly rational and truly understood their own best interests. Since people’s demands are driven by the benefits they perceive rather than the benefits they actually get, the financial system supplies too many products with exaggerated benefits and too few products with underappreciated benefits. And since perceived costs rather than actual costs drive people’s demands, the financial system supplies too many products with hidden costs.”

– John Campbell, Professor at Harvard, from his book ‘Fixed’

This quote encapsulates the core of Felix’s critique: the financial industry often caters to investor biases and perceived needs rather than promoting products that are truly beneficial for long-term financial health. Covered call funds, with their high fees and attractive yield distributions, are presented as a prime example of this phenomenon. While traditional actively managed funds have faced scrutiny for their high costs and underperformance, Felix observes a new wave of high-fee products, including covered call funds, being marketed by various creators, often without proper financial licensing.

Covered Calls in Market Downturns: A Double-Edged Sword

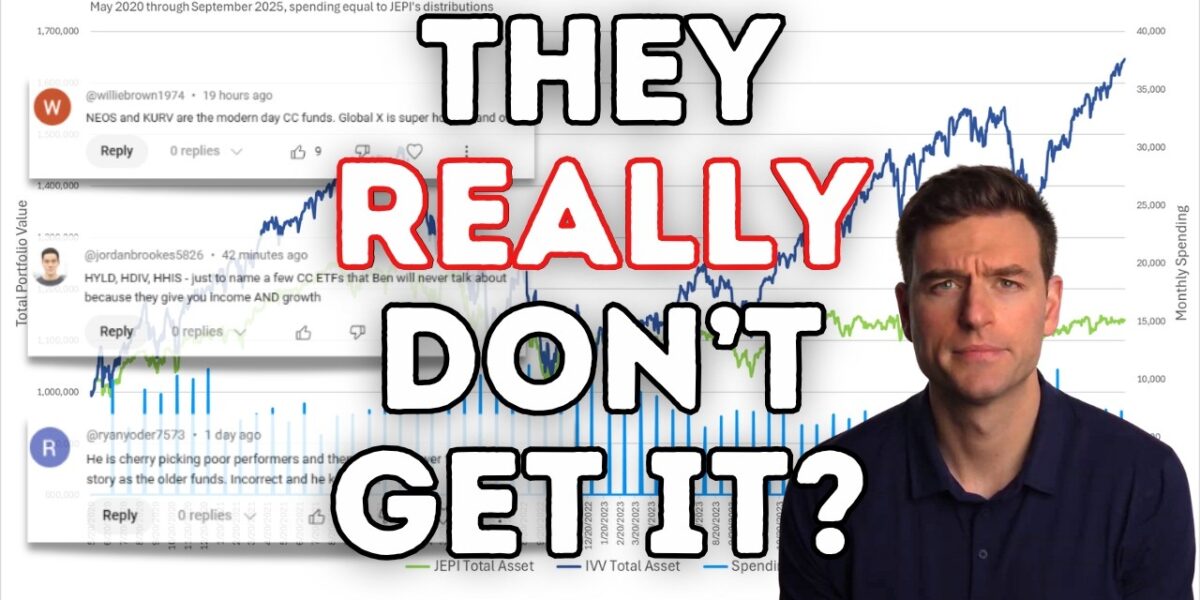

A common argument for covered call strategies is their ability to offer some protection during market downturns. Felix acknowledges this, citing historical data where covered call funds showed slightly reduced downside compared to their underlying benchmarks. For instance, an analysis of the Invesco S&P 500 BuyWrite ETF (Invesco S&P 500 BuyWrite ETF) from its inception in December 2007 through the Great Financial Crisis and subsequent market events, showed that while the covered call strategy offered a slight buffer, an investor in a plain S&P 500 index fund would have accumulated 3.88 times more wealth by the end of September 2025, assuming constant spending matched to the covered call fund’s distributions. This highlights that the option premiums provide a temporary cushion but do not negate the long-term drag on returns caused by capped upside.

To illustrate this point further, Felix walks through a detailed example comparing an investment in the JPMorgan Equity Premium Income ETF (JAPI) against the iShares Core S&P 500 ETF (IVV). Over a period including market declines and recoveries, the JAPI investor, by spending all monthly distributions, maintained a constant number of shares. In contrast, the IVV investor matched this spending by taking dividends and selling shares. While the IVV investor had to sell more shares during a downturn, their remaining shares grew in value faster during the subsequent recovery, leading to greater overall wealth accumulation. The critical takeaway is that the number of shares multiplied by their price determines wealth, and covered calls, by limiting upside, diminish this equation over the long run.

The Myth of Enhanced Income and Earlier Retirement

The notion that covered calls enable higher sustainable spending in retirement or allow for earlier retirement with less savings is a misconception, according to Felix. He argues that the only scenario where this might appear true is if investors are psychologically unable to access their own capital otherwise. Fundamentally, covered calls reduce expected returns, which inherently lowers the potential for sustainable long-term spending. The income generated is not a net gain but rather a reallocation that sacrifices future growth potential.

Performance Data: A Consistent Pattern of Underperformance

Felix addresses numerous comments suggesting he analyzed the wrong funds, presenting data on a range of US and Canadian listed covered call ETFs. The findings are largely consistent:

- NEOS S&P 500 High Income ETF (SPYI) trailed the Vanguard 500 Index Fund by 4.61% annualized since August 2022.

- NEOS NASDAQ 100 High Income ETF (QQQI) trailed the Invesco NASDAQ 100 ETF by 2% annualized since January 2024.

- JPMorgan NASDAQ Equity Premium Income ETF (JPQ) trailed the Invesco NASDAQ 100 ETF by an annualized 4.36% since May 2022. While JPQ showed some resilience in the 2022 downturn, its advantage was short-lived.

- Amplify CWP Enhanced Dividend Income ETF (DIVO), compared to the Vanguard Dividend Appreciation Index Fund ETF, underperformed by an annualized 51 basis points since December 2016.

- Hamilton Enhanced US Covered Call ETF (HYLD), a Canadian-listed ETF with 25% leverage, underperformed a Canadian dollar-hedged S&P 500 ETF by 0.9% annualized since February 2022.

- Hamilton Enhanced Multi Sector Covered Call ETF (HDIV), despite claims of beating the S&P TSX60, underperformed a reconstructed index fund portfolio matched to its underlying equities, even with HDIV’s 25% leverage.

- Harvest Diversified High Income Shares ETF (HHIS), a concentrated portfolio with leverage, showed that its underlying stocks, when adjusted for leverage, significantly outperformed the fund, isolating the negative impact of covered calls.

Felix emphasizes that short-term outperformance by actively managed or complex strategies is often unsustainable and should be viewed with extreme caution, especially when cheaper, lower-cost alternatives exist.

Market Impact and What Investors Should Know

The proliferation of covered call funds, often marketed by unlicensed content creators, poses a significant risk to investors who may not fully grasp the associated costs and long-term implications. These products exploit psychological biases, particularly the desire for income, while obscuring the detrimental impact on expected returns and overall wealth accumulation. Investors are urged to look beyond the advertised yields and understand the trade-offs involved. The core principle remains that long-term investment success hinges on maximizing expected returns and minimizing costs, a goal that covered call strategies, by their nature, compromise.

Felix’s ongoing commentary on covered calls stems from a desire to provide clarity in a complex financial marketplace. By dissecting these products with fundamental analysis and performance comparisons, he aims to empower investors to make more informed decisions, steering them towards low-cost, diversified index funds that are more likely to support long-term financial goals.

Source: Covered Calls: What People (Still) Get Wrong (YouTube)

Related Articles

401(k) Changes Poised to Reshape Retirement Savings

The SECURE Act 2.0 is introducing significant changes to 401(k) plans, including enhanced catch-up contributions and automatic enrollment features. These updates aim to boost retirement savings for millions of Americans. Employers will also have new options regarding Roth contributions.

Market Volatility and Investor Strategies in Focus

A financial commentator discussed market volatility, the impact of AI and crypto, and career paths in finance during a birthday Q&A. Insights were shared on passive investing, the role of technology, and historical perspectives on money.

Beyond Flips: The Power of Long-Term Real Estate

While house flipping and quick deals offer immediate financial appeal, a long-term real estate investment strategy centered on rental properties unlocks significant wealth-building potential through passive income, tax advantages, and leverage.