Builders Slash Prices, Signaling Market Shift

Major home builder Lennar has cut prices by 24% due to a significant buildup of unsold inventory, signaling a market correction. With a 9.7-month supply of homes, builders are offering deep discounts and mortgage incentives, especially in oversupplied regions. Buyers may find new opportunities, but the extent of future price drops remains uncertain.

Builders Slash Prices, Signaling Market Shift

America’s second-largest home builder, Lennar, has sent a clear signal about the U.S. housing market. The company recently announced significant price cuts, slashing prices by 24% from their peak in 2022. This move comes as builders face a growing surplus of unsold homes.

Inventory Overload Forces Builder Action

The primary driver behind these price reductions is a substantial buildup of inventory on builder lots. As of early 2026, the market is experiencing a 9.7-month supply of homes. This level is considered heavy correction territory, meaning there are far more homes available than buyers are currently purchasing.

This oversupply forces builders like Lennar to take action. They are not only lowering the sticker price of homes but also offering significant incentives. These can include deep discounts on the purchase price and attractive mortgage rate buydowns to help make homes more affordable for buyers.

Price Drops and What They Mean

The average price for a new Lennar home has dropped from $491,000 to $370,000. This 24% net price reduction accounts for both outright price cuts and the value of incentives like mortgage rate buydowns. These incentives can significantly lower a buyer’s monthly payments, especially in a high-interest-rate environment.

Regional Hotspots and Buyer Impact

The impact of this market shift is felt most acutely in certain regions. States highlighted in red on a recent map show the highest levels of inventory and building permits. These areas are likely to see the most aggressive pricing strategies from builders.

Buyers in these oversupplied markets may find themselves with more negotiating power and better deals. However, the question remains about how much further prices might fall. This uncertainty can make it difficult for buyers to time their purchase perfectly.

Understanding Market Dynamics

This situation highlights a common real estate cycle. When demand is high and inventory is low, prices tend to rise quickly. Builders respond by constructing more homes to meet that demand. However, if demand cools or interest rates rise, inventory can pile up, leading to price corrections.

For potential buyers, understanding these market dynamics is key. While falling prices might seem appealing, it’s important to consider long-term value and affordability. Factors like local job growth, population trends, and overall economic health play a crucial role in housing market stability.

Investors often look at metrics like cap rates (capitalization rates) to assess potential returns. Cap rate is calculated by dividing the net operating income of a property by its current market value. A higher cap rate generally suggests a better potential return on investment. However, in a market with falling prices, predicting future income and value becomes more challenging.

Another important concept is loan-to-value (LTV) ratio. This is the amount borrowed compared to the value of the property. A lower LTV, meaning a larger down payment, can lead to better loan terms and less risk for both the buyer and the lender. High LTV loans can be riskier, especially if property values decline.

Cash flow refers to the net income generated from a rental property after all expenses are paid. Positive cash flow means the property is making money each month. In a market where prices are falling, maintaining positive cash flow can become more difficult if rents do not keep pace with mortgage payments and other costs.

Broader Economic Influences

The housing market doesn’t exist in a vacuum. Broader economic factors significantly influence its direction. High interest rates, for example, make mortgages more expensive, reducing buyer purchasing power and cooling demand. Inflation can increase the cost of building materials and labor, impacting builder profitability.

Job market strength is also critical. When people have secure jobs and rising incomes, they are more likely to buy homes. Conversely, economic uncertainty or job losses can lead to fewer home sales and potential price declines. The current economic climate, with its mix of steady employment in some sectors and inflation concerns, creates a complex environment for housing.

Looking Ahead

The aggressive pricing strategies from major builders like Lennar suggest a significant shift in the housing market. While this presents potential opportunities for buyers, especially in oversupplied regions, it also signals a period of adjustment. Understanding local market conditions and broader economic trends will be crucial for anyone looking to buy, sell, or invest in real estate in the coming months.

Source: 2008-style housing warning from Lennar (cheap houses hitting market) (YouTube)

Related Articles

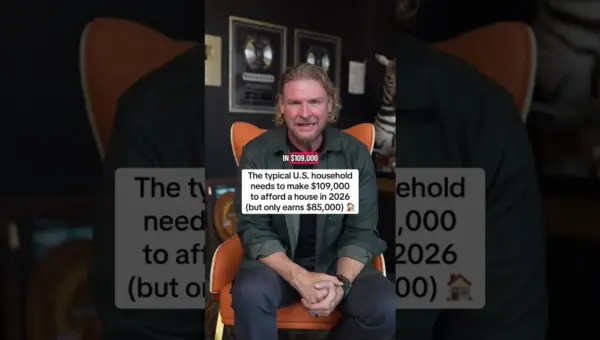

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.

Builders Cut Prices as New Home Sales Plummet

Home builders are facing their worst sales slump in 13 years, leading to aggressive price cuts and a surge in unsold inventory. This trend, mirroring the 2008 crisis, suggests a significant market correction is underway. The mortgage rate lock-in effect is currently propping up the existing home market, but future pressures may bring more inventory and negotiation opportunities for buyers.

Housing Market Cools: Prices Dip as Rates Climb

The U.S. housing market is cooling significantly, with prices falling for the first time in nearly 20 years. Rising mortgage rates, increased inventory, and affordability issues are driving down demand, while regional markets show mixed performance. Experts suggest a normalization after years of excess, emphasizing long-term fundamentals for investors.