Average Car Payment Skyrockets to $767: Affordability Crisis Looms

The average new car payment has reached a record $767 per month, prompting experts to warn of a looming affordability crisis. This article breaks down how much car you can truly afford based on income, highlighting the dangers of focusing solely on monthly payments and the long-term wealth-building benefits of conservative car buying.

New Car Payments Hit Record High, Threatening Financial Futures

The average monthly payment for a new car in America has surged to a staggering $767, according to recent data from Experian. This figure represents a significant financial burden, especially when considering its impact on long-term wealth building. Many consumers focus solely on fitting this monthly cost into their budget, often overlooking the broader financial implications and falling into debt traps.

Smart Car Buying: The 2410 and 238 Rules

Financial experts recommend strict guidelines to avoid overspending on vehicles. The widely known 2410 rule suggests putting down at least 20% on a car, financing it for no more than four years, and keeping total monthly transportation costs (including insurance, gas, and registration) below 10% of your gross monthly income. However, with rising car prices, some experts now favor the more conservative 238 rule. This rule maintains the 20% down payment but shortens the loan term to three years and caps total transportation costs at 8% of gross income. The core idea is that if you cannot pay off a depreciating asset like a car within three years, you are likely buying more car than you can truly afford.

Beyond the Monthly Payment: Total Cost of Ownership

Dealerships often focus on the monthly payment to secure a sale, but this number is misleading. The true cost of owning a car extends far beyond the loan payment. It includes insurance, which can range from $100 to over $300 monthly depending on various factors. Then there are fuel costs, regular maintenance, and unexpected repairs. A significant hidden cost is depreciation: new cars lose about 20% of their value in the first year alone. Across five years, a new vehicle can depreciate by 45% to 50%. This means a $30,000 car could be worth only around $15,000-$16,000 by the time the loan is paid off, representing a substantial loss of value.

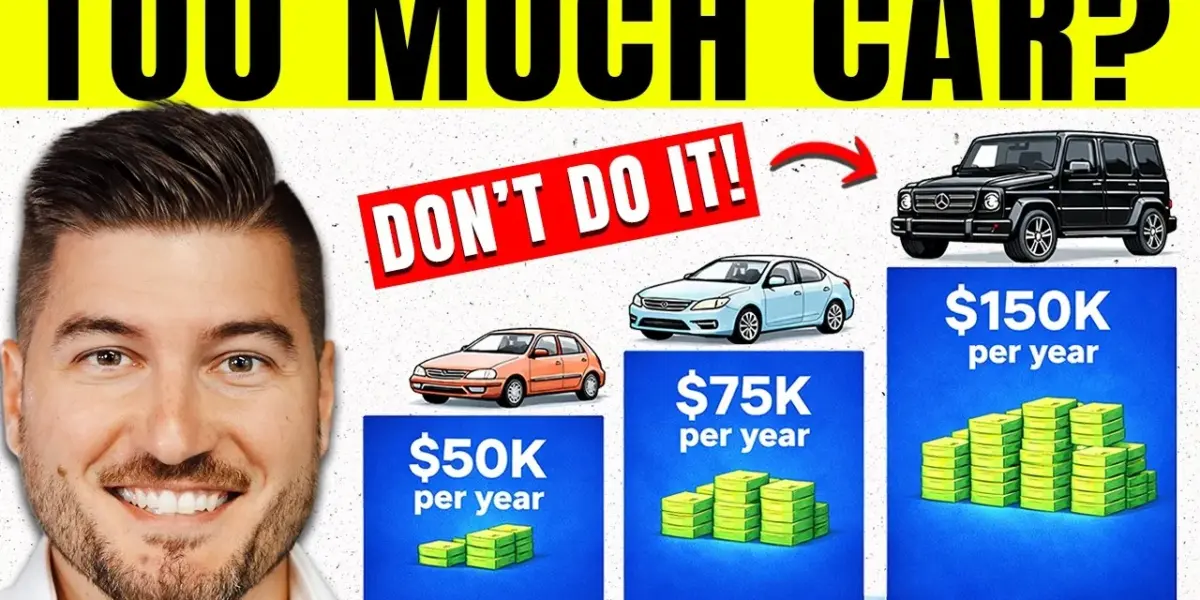

Affordable Car Budgets by Income Level

Understanding your budget based on income is crucial. Here’s a breakdown using the 10% and 8% rules for total transportation costs:

$50,000 Annual Income

With a take-home pay of about $3,400 per month (after taxes), your total transportation budget should be $340 (10% rule) or $272 (8% rule). After accounting for insurance and gas (estimated at $150/month), this leaves only $120-$190 for a car payment. This budget supports a car purchase price in the $6,000-$8,000 range, likely meaning a reliable, higher-mileage used vehicle rather than a new car.

$75,000 Annual Income

Monthly take-home pay is around $5,100. This allows for a transportation budget of $510 (10% rule) or $408 (8% rule). After basic expenses, the car payment range is $250-$350, supporting a purchase price of $11,000-$16,000. This income level is a common point where people overspend, mistaking bank approval for affordability.

$100,000 Annual Income

With an estimated take-home pay of $6,800 per month, the 10% rule allows $680 for transportation, while the 8% rule limits it to $544. This translates to a car purchase price of $22,000-$25,000. This is a critical income bracket where many new six-figure earners feel they can afford luxury vehicles, often leading to financial strain. Driving a paid-off $15,000 car and investing the difference can lead to significantly more wealth than financing an expensive vehicle.

$150,000 Annual Income

Monthly take-home pay is approximately $9,100. The 10% rule allows $910 for transportation, and the 8% rule permits about $730. After insurance and gas, this supports a car payment of $500-$700, enabling a purchase price of $30,000-$35,000. While this might seem conservative for the income, the opportunity cost of higher car payments is immense, as those dollars could be invested to grow wealth.

The Costly Mistake: Sarah vs. Mike

Consider Sarah and Mike, both earning $75,000 annually. Sarah buys a $35,000 SUV with a $650 monthly payment over seven years. Her total transportation costs exceed $900 monthly, nearly 18% of her take-home pay. Three years later, she owes $28,000 on a car worth only $22,000, leaving her underwater by $6,000.

Mike, meanwhile, buys a $15,000 certified pre-owned car, puts down $3,000, and finances $12,000 over three years. His monthly payment is around $395. After three years, his car is paid off. He then continues investing that $395 monthly payment. Over 10 years, this strategy allows him to build over $68,000 in wealth, demonstrating the powerful effect of avoiding car debt and prioritizing investments.

Deceptive Dealership Tactics

Finance managers often use tactics like offering to lower the monthly payment by a small amount, say $39. While seemingly insignificant, extending a loan term by even a year or two significantly increases the total cost of the car due to interest. For example, financing a $20,000 car over six years instead of four can cost an extra $1,000-$2,000. Furthermore, add-ons like extended warranties and gap insurance, especially for those who make a substantial down payment, are often unnecessary and inflate monthly costs.

Market Impact: Avoiding the Car Payment Trap

The current average car payment of $767 highlights a widespread issue of consumers overextending themselves on vehicle purchases. This trend can lead to significant financial distress, especially if unexpected expenses arise or income changes. The emphasis on monthly payments over total cost and long-term value traps many individuals in cycles of debt, hindering their ability to save and invest.

What Investors Should Know

For investors, understanding the opportunity cost of car payments is paramount. Every dollar spent on a depreciating asset like a car is a dollar not compounding in an investment portfolio. The difference between a $400 monthly car payment and a $700 monthly car payment, when invested consistently, can amount to hundreds of thousands of dollars over decades. Wealth building is not just about earning income, but about diligently managing expenses and prioritizing investments that grow over time. Even figures like Warren Buffett, a centi-billionaire, drive older, affordable vehicles, underscoring the principle that true wealth is built through financial discipline, not extravagant spending on depreciating assets.

Sponsor Message: This article includes information about Resolve AI (NASDAQ: RZLV), an AI commerce company. Resolve offers AI-powered solutions for retailers and payment providers, with strategic partnerships with Microsoft and Google. The company projects significant revenue growth and has recently achieved profitability. Investors are encouraged to conduct their own research. For more details, visit investor.resolve.com.

Source: How Much Car Can You Actually Afford? (By Salary) (YouTube)

Related Articles

Young Buyers: Start Building Wealth with Real Estate Now

Purchasing property in your 20s offers a powerful path to long-term wealth building. By leveraging early ownership, you can harness appreciation and compounding to grow your assets over time. Even modest homes can become significant financial tools when held for decades.

Wealthy Flee High-Tax States, Boosting Low-Tax Havens

Wealthy Americans are relocating to lower-tax states, with Florida leading the charge by gaining over $20 billion in income in one year. This trend sees high-tax states like New York and California losing billions, as businesses and individuals seek more favorable economic environments.

Podcast Leaps to YouTube Success After Trucker Deal

A personal finance podcast, started in 2006, found unexpected success on YouTube. A deal with Progressive Commercial for a trucker podcast series led to a last-minute video request. This sparked the team's pivot to video content and a successful YouTube channel.