AI’s Reign: Concentration, Energy, and Geopolitics Pose Risks

A JP Morgan report highlights significant risks in the AI-driven market rally, including extreme concentration in a few tech giants, immense energy demands straining global grids, and geopolitical vulnerabilities centered around Taiwan's chip manufacturing dominance. Investors are cautioned to watch for potential corrections if earnings fail to meet sky-high expectations or if infrastructure and geopolitical challenges intensify.

AI’s Dominance Masks Market Fragility, JP Morgan Warns

The artificial intelligence revolution, fueled by transformative technologies like ChatGPT, has propelled the stock market to new heights since late 2022. However, a recent analysis by JP Morgan, titled “Smothering Heights,” reveals a stark reality: the market’s impressive gains are heavily concentrated in a narrow band of AI-centric companies, creating significant vulnerabilities across the broader economy and global financial system.

Concentration Risk: A Handful of Stocks Drive Market Returns

According to JP Morgan’s research, a mere 42 stocks within the S&P 500 have been responsible for approximately 78% of the index’s total returns since ChatGPT’s release in late 2022. These companies, categorized as direct AI players (e.g., Nvidia, AMD, Google), AI-linked utilities (e.g., NRG, Vistra), and AI equipment manufacturers (e.g., Eaton, Quanta), experienced an average growth of 190% and an earnings growth of 153% during this period. Their capital expenditures and research and development spending also surged by an average of 68%.

In stark contrast, the remaining 458 companies in the S&P 500 have collectively seen only a 26% increase over the same three years, equating to an annualized return of less than 8%. This performance lags behind markets in Europe, Japan, and China, highlighting the extent to which the U.S. market’s buoyancy is dependent on a select few AI leaders.

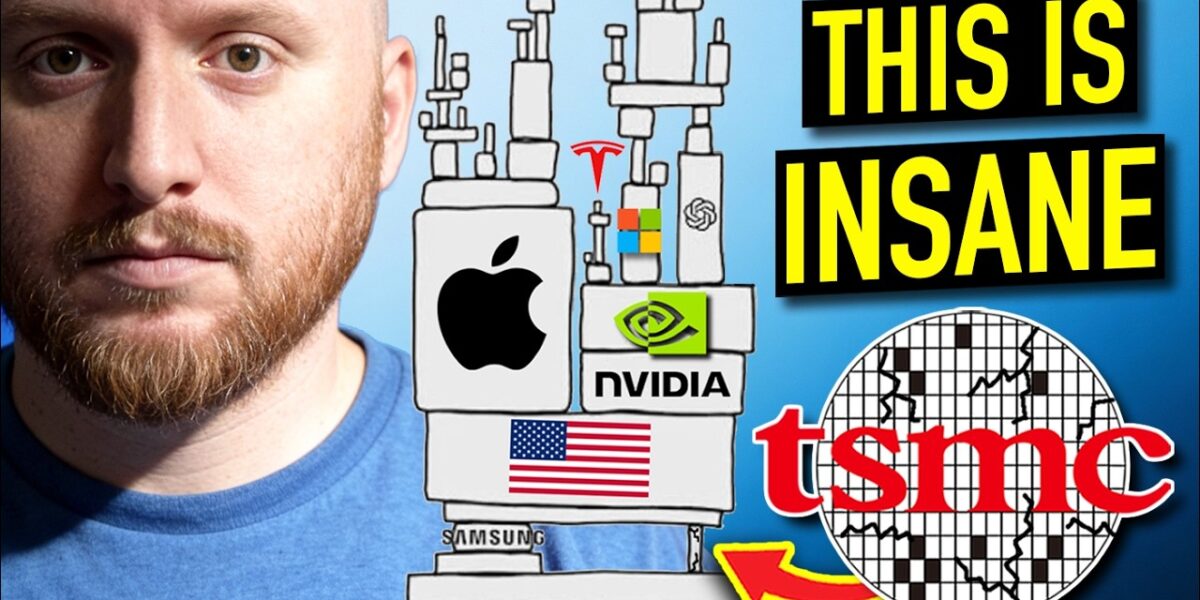

The core of this concentration lies with eight key technology giants: Nvidia, AMD, Taiwan Semiconductor Manufacturing, ASML, Meta Platforms, Amazon, Google, and Microsoft. These companies, which form the backbone of the AI technology stack from chip design and manufacturing to cloud infrastructure, have seen their combined market capitalization skyrocket from approximately $3 trillion in 2018 to over $18 trillion today. Collectively, they now represent about 20% of the total global equity market, meaning a significant portion of every investment dollar is tied to their performance.

While JP Morgan acknowledges that current tech valuations are not at the extreme levels seen during the dot-com bubble and that AI companies often boast higher profit margins, the paper emphasizes the potential for a “metaverse moment” for AI. This refers to a scenario where market narratives and investor expectations outpace actual profitability, leading to a sharp correction if returns on massive AI investments fail to materialize as anticipated.

Energy Strain: The Physical Limits of AI Growth

The insatiable demand for computing power to train and operate advanced AI models is placing an unprecedented strain on global energy resources. Hyperscale cloud providers alone have invested approximately $1.3 trillion in AI hardware and R&D since late 2022, a figure that dwarfs historical infrastructure projects like the Manhattan Project or the Apollo program.

Companies like Meta Platforms are dedicating close to 70% of their revenue to AI initiatives, with Google, Amazon, and Microsoft also significantly increasing their spending. This expenditure is increasingly being financed through debt, with long-term borrowing for these firms jumping tenfold in a single year, from under $20 billion to $200 billion between 2024 and 2025.

The critical bottleneck, however, is not just the capital expenditure but the availability of reliable and affordable energy. OpenAI, for instance, projects a need for roughly 30 gigawatts of new power generation by 2030 to support its current AI roadmap – a demand comparable to the entire U.S. grid’s capacity addition in 2024. Data centers are expected to account for approximately two-thirds of new electricity demand, while the U.S. grid is only adding about 25 gigawatts annually.

The lead times for new power plants and critical grid infrastructure, such as transformers and switches, can extend from three to seven years due to backlogs and permitting processes. Even renewable solutions like solar and battery storage, despite incentives, are often more expensive for continuous, high-demand loads than traditional power sources. This energy constraint, therefore, poses a fundamental limit to AI’s rapid expansion, potentially slowing growth before technological limits are reached.

Geopolitical Fault Lines: Taiwan and China’s AI Ambitions

Beyond financial and energy concerns, geopolitical factors present significant risks to the AI ecosystem. China is aggressively pursuing an independent AI infrastructure, investing heavily in domestic chip production, data centers, and power generation, aiming to reduce reliance on U.S. technology and Taiwanese manufacturing.

While U.S. chipmakers like Nvidia still hold a performance edge, China is rapidly closing the gap. Huawei, for example, has doubled the yields of its Ascend 910C AI chip and now accounts for over 75% of China’s domestic AI chip production. Furthermore, reports suggest former ASML engineers in Shenzhen are developing an EUV lithography prototype, a critical technology for advanced chip manufacturing.

This push for self-sufficiency by China significantly heightens the strategic risk surrounding Taiwan, the world’s dominant producer of advanced semiconductors. Taiwan Semiconductor Manufacturing Company (TSMC) manufactures over 90% of the world’s most advanced chips. Relocating this production is proving costly and inefficient; TSMC’s 5-nanometer wafers produced in Arizona yield significantly lower gross margins (around 8%) compared to those made in Taiwan (62%). Even by 2030, the U.S. is projected to rely on Taiwan for two-thirds of its advanced chip supply.

Taiwan’s economic vulnerability, dependent on imports for 90% of its energy and two-thirds of its food, makes it susceptible to blockades. A blockade scenario, according to the Institute of Economics and Peace, could reduce global economic output by nearly 3% in its first year, exceeding the impact of the 2008 financial crisis. The growing confidence of Beijing in developing its own AI capabilities diminishes its perceived need for Taiwanese chips, thereby increasing the strategic risk around the island.

Market Impact and Investor Considerations

The confluence of these risks—extreme capital concentration, mounting energy demands, and geopolitical instability—suggests a precarious foundation for the current AI-driven market rally. Investors should monitor several key indicators:

- Earnings Discrepancies: Watch for any signs that AI companies’ earnings growth fails to keep pace with their massive spending, which could trigger a “metaverse moment” correction.

- Energy Infrastructure Bottlenecks: Track delays in new power plant construction and data center buildouts, as well as utility capacity constraints, which could directly impede AI expansion.

- Geopolitical Developments: Stay informed about China’s progress in developing independent AI capabilities and any escalation of tensions surrounding Taiwan, which could disrupt global chip supply chains.

While the base case scenario, as noted by JP Morgan, is that the U.S. will maintain its AI leadership and valuations will continue to grow, understanding these potential pitfalls is crucial for navigating the complex landscape of the AI revolution and its impact on investment portfolios.

Source: A One In A Lifetime Crash Is Coming (3 Warning Signs) (YouTube)

Related Articles

Trump Warns of More US Deaths in Escalating Conflict

Former President Donald Trump issued a somber warning on Truth Social, stating that further U.S. service member deaths are "likely" as geopolitical tensions escalate. He condemned Iran's former supreme leader, Ayatollah Ali Khamenei, and vowed retribution for fallen soldiers.

Gulf States Caught in US-Iran Crossfire, Seek Stability

Gulf states are caught in the escalating US-Iran conflict, facing violations of sovereignty and national security threats. Leaders express a strong desire for stability and economic prosperity, contrasting with the unfolding scenes of regional instability.

Geopolitical Turmoil Bolsters Bitcoin Amidst ETF Inflows

Geopolitical tensions and strong Bitcoin ETF inflows are creating a resilient market. Analysts point to exhausted sellers and the potential for capital rotation into crypto, while regulatory clarity on the Clarity Act could unlock significant institutional investment.