Housing Market Fears: Separating Fact from Fiction

Alarming charts suggesting a housing market collapse are misleading due to limited data. While the market is undergoing a correction, understanding economic factors and regional variations is key for buyers, sellers, and investors.

Navigating the Current Housing Landscape: Beyond the ‘Scary’ Charts

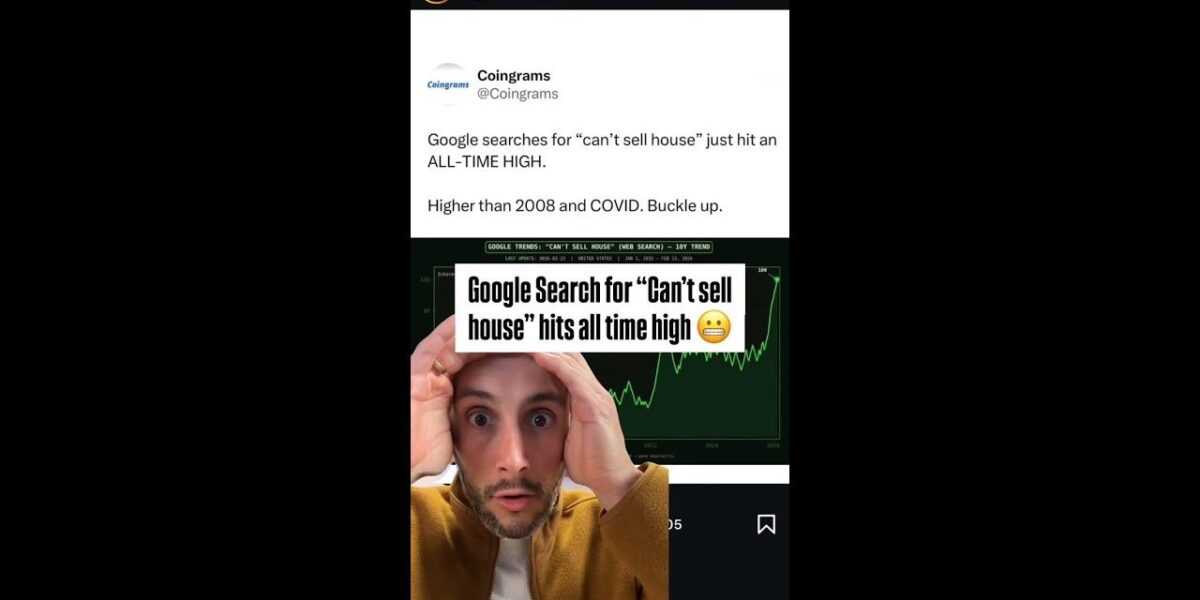

Recent online discourse has been dominated by a seemingly alarming chart suggesting a dire state of the housing market, with some proclaiming it worse than the 2008 financial crisis and the COVID-19 pandemic. However, a closer examination reveals that this widely circulated data may be misleading, designed to incite fear rather than provide accurate market analysis. While it’s true that selling a home can be challenging in the current environment, and we are indeed experiencing a housing correction, understanding the nuances of market data is crucial for informed decision-making.

The Misleading Chart: A Closer Look at Data Limitations

The chart in question, frequently shared across social media platforms, purports to show an all-time high in Google searches for terms like “can’t sell your house.” This surge in search interest is presented as evidence of an impending market collapse, drawing parallels to historical downturns. However, a critical flaw in this narrative becomes apparent upon closer inspection: the chart’s data often begins as recently as 2015.

This limited timeframe makes it impossible to accurately compare the current situation to events like the 2008 crisis, which predates the chart’s scope. Claims that this data represents the “worst of all time” or is “worse than 2008” are, therefore, unsubstantiated and potentially deliberate fear-mongering.

Understanding Housing Corrections vs. Market Crashes

It is important to distinguish between a housing correction and a market crash. A housing correction is a period of declining home prices that typically occurs after a significant period of rapid appreciation. This is a natural part of the real estate cycle, often driven by factors such as rising interest rates, increased inventory, and shifting economic conditions.

During a correction, selling a home may take longer, and buyers may find themselves in a stronger negotiating position. This is the scenario many experts believe the market is currently experiencing.

A market crash, on the other hand, is a more severe and rapid decline in asset values, often accompanied by widespread economic distress, such as high unemployment and financial instability. While a crash is a possibility in any market, the current evidence does not strongly suggest that a crash is imminent. The housing market is influenced by a complex interplay of economic factors, and while challenges exist, they do not automatically equate to a systemic collapse.

The Impact of Interest Rates and Economic Factors

Several broader economic factors are contributing to the current housing market dynamics. Rising interest rates, implemented by central banks to combat inflation, have a direct impact on housing affordability.

Higher mortgage rates increase the monthly cost of homeownership, potentially pricing out some buyers and reducing demand. For instance, a homebuyer seeking a $400,000 mortgage at 3% interest would have a significantly lower monthly payment than if they were to secure the same loan at 7% interest.

Inflation itself also plays a role. When the cost of goods and services rises, consumers have less disposable income, which can affect their ability to save for down payments or afford higher mortgage payments.

Employment levels and wage growth are critical indicators. A strong job market generally supports housing demand, while rising unemployment can weaken it.

Regional Variations and Who is Most Affected

The housing market is not monolithic; it varies significantly by region. Some areas that experienced extreme price growth during the pandemic may now be more susceptible to price corrections. Conversely, markets with strong local economies and consistent demand may prove more resilient.

Buyers in the current market may find more opportunities, with increased inventory and potentially more room for negotiation. However, they must contend with higher borrowing costs.

Sellers may need to adjust their expectations, as the rapid appreciation seen in recent years may have slowed or reversed. Homes may take longer to sell, and pricing strategies are more critical than ever.

Investors are closely watching metrics such as capitalization rates (cap rates) and cash flow. Cap rates, which represent the potential return on investment for a property, are influenced by rental income and property value.

In a correcting market, investors may seek properties with stronger cash flow potential to mitigate risks. The loan-to-value (LTV) ratio, which compares the loan amount to the property’s value, also remains a key consideration for financing and risk assessment.

Looking Ahead: A Market in Transition

While the current housing market presents challenges, and periods of decline are uncomfortable, they are also a natural and often necessary part of a healthy economic cycle. The “scary” charts that lack proper context should be viewed with skepticism.

Instead, focus on understanding the underlying economic drivers, the distinction between corrections and crashes, and the specific dynamics of your local market. By doing so, individuals can make more informed decisions, whether they are looking to buy, sell, or invest in real estate.

Source: This “Scary” Chart Is Fooling Investors (YouTube)

Related Articles

Median Home Price Now Out of Reach for Median Income

The median home price in the U.S. has now surpassed what the median household income can afford, creating a significant barrier to homeownership. Analysis shows a required salary of over $112,000 for the median home price, far exceeding the median income of $84,000. This affordability gap challenges the traditional dream of owning a home for many Americans.

BlackRock CEO Urges Crypto Buyers to ‘Buy the Dip’

BlackRock CEO Larry Fink is strongly advocating for investors to 'buy the dip' in cryptocurrencies, citing Bitcoin and Ethereum as key areas of interest. He believes digital assets and tokenization are early indicators of massive growth in global capital markets. Fink's endorsement highlights institutional confidence in crypto's long-term potential.

Powell’s Fed Exit Looms: Warsh Poised for Top Job

Kevin Warsh is reportedly set to become the next Federal Reserve Chair, with his confirmation hearing scheduled soon. This potential leadership change at the central bank signals a new direction for U.S. economic policy.