Stagflation Fears Grip Housing Market

Stagflation fears are rising as a troubling economic scenario reminiscent of the 1970s looms. This means higher prices coupled with job losses, potentially impacting the housing market significantly. Investors and buyers should prepare for challenges ahead.

Stagflation Fears Grip Housing Market

A troubling economic scenario, known as stagflation, is casting a shadow over the housing market. This condition means prices for everyday goods keep climbing while job losses mount. The last time this happened was in the 1970s, and many see worrying signs of a repeat performance.

The early 1970s saw a perfect storm brew for the economy. First, the U.S. dollar was detached from the gold standard. This move gave the government more power to print money, which helped fuel rising prices. Soon after, the U.S. became involved in a conflict in the Middle East. This led to a sharp increase in oil prices, making everything from gas to transportation more expensive.

To fight this inflation, the Federal Reserve had to raise interest rates. Higher rates make borrowing money more costly for businesses and individuals. This action slowed down the economy, pushing it into a deep recession. The result was an economy with rising prices and falling employment – a difficult situation for most people.

Today’s Echoes of the Past

Now, history seems to be rhyming. Following the pandemic, significant money printing contributed to a surge in inflation. More recently, in 2026, a new conflict in the Middle East has caused oil prices to jump rapidly. This mirrors the oil shocks of the past, creating similar pressures on the cost of living.

The major concern today is how the Federal Reserve will respond. To combat the current inflation, they might need to raise interest rates, not lower them as many hoped. If this happens, especially if the Middle East conflict continues, it could trigger another economic slowdown or recession. This is the core of stagflation fears: rising prices combined with a struggling economy.

Impact on Housing and Investors

For the housing market, this scenario presents significant challenges. Rising interest rates make mortgages more expensive, reducing buying power for potential homeowners. This can lead to fewer sales and potentially stagnant or falling home prices in some areas. Investors who rely on rental income might face higher operating costs due to inflation, while also seeing slower rent growth if the economy weakens.

Consider the concept of cash flow in real estate investing. Cash flow is the money left over from rental income after paying all expenses, like mortgage payments, property taxes, and maintenance. In a stagflationary environment, rising expenses could eat into this cash flow, making properties less profitable. For example, if a landlord’s insurance costs go up by 15% and their maintenance costs rise by 10%, but they can only increase rent by 3% due to economic weakness, their cash flow shrinks.

Another key term is the loan-to-value (LTV) ratio. This compares the amount of a loan to the value of the property. Lenders use LTV to assess risk. If property values start to fall during an economic downturn, a high LTV could put borrowers in a difficult position, potentially owing more than their home is worth.

Cap rates, or capitalization rates, are also important for investors. They measure the potential return on a real estate investment property. A cap rate is calculated by dividing the net operating income (income after expenses but before debt payments) by the property’s current market value. For instance, a property earning $30,000 in net operating income and valued at $500,000 has a cap rate of 6% ($30,000 / $500,000). In an uncertain economy, investors might demand higher cap rates to compensate for increased risk, meaning they would expect to pay less for the same income stream.

Regional Differences and Broader Economy

The effects of potential stagflation won’t be felt equally across the country. Areas with economies heavily reliant on industries sensitive to oil prices, like transportation or manufacturing, could suffer more. Conversely, regions with diverse economies or those less affected by energy costs might fare better. Buyers in high-cost-of-living areas could find themselves particularly squeezed by higher mortgage rates and persistent inflation.

The Federal Reserve’s actions are crucial. If they raise rates too aggressively to fight inflation, they risk triggering a sharp recession. If they are too slow, inflation could become entrenched, making it harder to control later. This balancing act is delicate and has major implications for borrowing costs, job growth, and overall economic stability.

As the economic outlook remains uncertain, both homeowners and investors should monitor inflation data, interest rate movements, and geopolitical events closely. Understanding these complex economic forces is key to making informed decisions in the current housing market climate.

Source: Stagflation Warning 1970s Crisis Repeating in 2026 (YouTube)

Related Articles

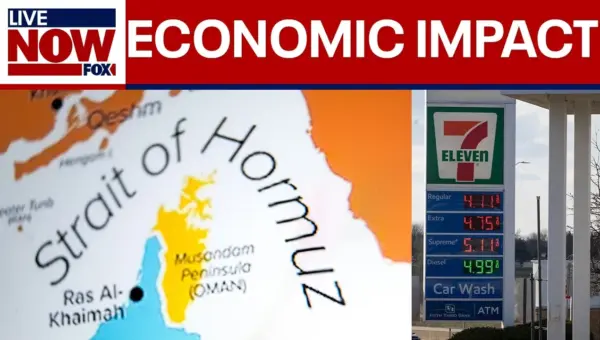

Trump Orders Strait of Hormuz Blockade, Risks Global Oil Shock

President Trump has ordered the U.S. Navy to blockade the Strait of Hormuz, a critical global oil transit point, sparking fears of soaring energy prices and inflation. This strategic move aims to exert pressure on Iran and China, while also addressing domestic economic concerns ahead of midterm elections.

Buy Low, Sell High: Counter-Cyclical Real Estate Strategy

Discover the counter-cyclical real estate strategy: buying properties when others are selling at steep discounts. Learn how to identify opportunities in down markets and achieve long-term gains by going against the crowd.

Fed May Restart Printing Money Amid Oil Price Surge

The Federal Reserve may restart quantitative easing (QE) to combat rising oil prices, potentially increasing its $9 trillion balance sheet. This move aims to inject money into the economy but carries the risk of worsening inflation.