Shift Focus From Income to Assets to Build Wealth

Chasing income, avoiding financial math, spending before investing, misusing debt, and prioritizing appearances are common traps that prevent wealth building. Shifting focus to acquiring income-producing assets and adopting disciplined financial habits are key to achieving long-term financial freedom.

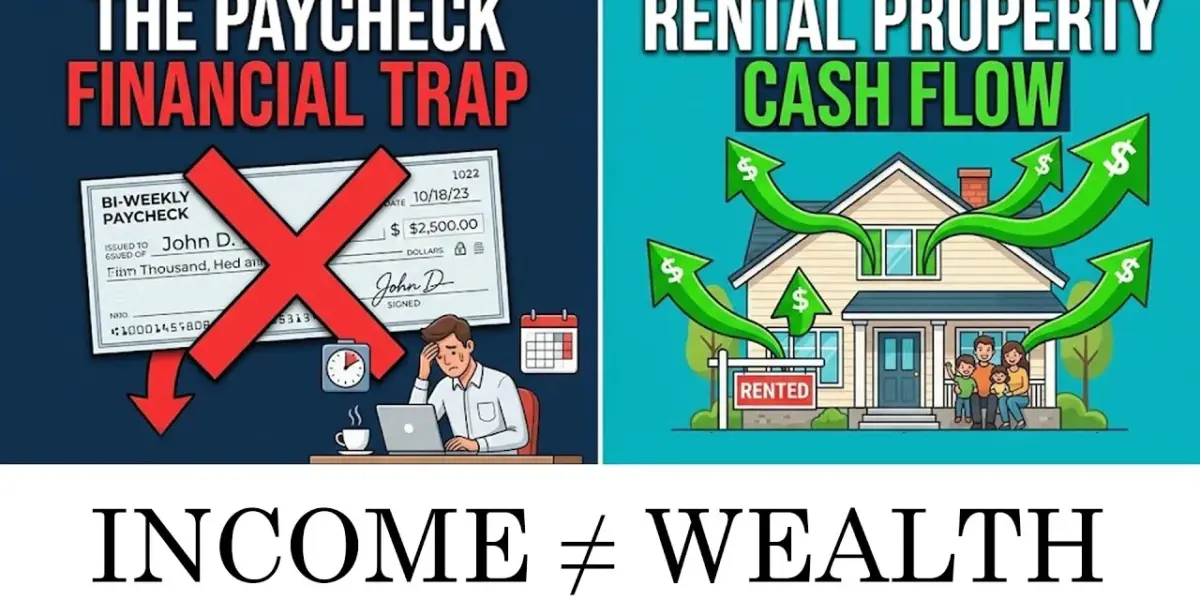

Wealth Building Hinges on Assets, Not Just Income

Many hardworking individuals find themselves financially stuck, even with good salaries and retirement savings. The year 2023 highlighted how inflation can expose weak financial plans and rising interest rates can reveal problems with debt. The core issue? Most people are still following outdated economic rules. True wealth building today relies on a simpler math and a shift in behavior, moving focus from chasing income to acquiring income-producing assets.

1. Income vs. Assets: The Wealth Trap

A common mistake is chasing income – always seeking raises, promotions, or side hustles. While earning more feels good, it doesn’t automatically lead to wealth. The key difference lies in what happens when you stop working. If the money stops, it’s income. If the money keeps coming in without your active labor, that’s wealth. Consider a $10,000 raise: often, this extra income is spent, leaving no lasting financial gain. In contrast, a rental property, once purchased, can generate consistent monthly income from rent, working for you even when you’re not. Wealthy individuals prioritize assets like real estate, businesses, or investments that generate passive income and appreciate over time. This shift requires moving away from the ‘trading time for dollars’ mindset.

2. The Critical Need for Financial Math

Many people lack a clear financial plan because they haven’t done the math. Vague goals like needing “a million dollars” aren’t actionable. To retire comfortably, one must calculate current lifestyle costs, project them over expected retirement years, and account for inflation. For example, a $6,000 monthly lifestyle ($72,000 annually) could require over $2 million for 30 years of retirement, even before inflation. With a 3% annual inflation rate, that $72,000 could jump to $100,000 within 15 years, significantly increasing the total needed. Fortunately, tools like AI can help run these complex calculations, making it easier to determine your personal financial target. Ignoring these numbers leads to panic later in life, as time, the most valuable asset, is lost.

3. Investing First, Spending Second

The pressure to keep up with the Joneses often leads to spending money before investing it. A bonus check might be earmarked for investments, but then immediate wants like new car tires, braces for children, or home upgrades take priority. This spending-first habit drains funds, leaving little for wealth-building. The wealthy reverse this order: they invest first, automating a portion of their income (e.g., 20%) into assets before spending. They then learn to live on the remaining 80%. This principle, known as “paying yourself first,” ensures that investments are prioritized over immediate consumption, leading to long-term financial freedom rather than lifestyle inflation.

4. Good Debt vs. Bad Debt

Debt itself isn’t inherently bad; its misuse is the problem. ‘Bad debt’ is borrowing money for depreciating assets like cars or vacations. Financing a $40,000 car at 7% might result in paying back $47,000 over five years, while the car’s value plummets to $20,000, representing a significant loss. ‘Good debt,’ however, is used to acquire income-producing assets. For instance, borrowing $160,000 at 7% for a $200,000 rental property can be beneficial. If a tenant pays the mortgage and the property appreciates, the debt is serviced by income and the asset grows in value. Over five years, such an investment could generate tens of thousands in cash flow and appreciation, far outweighing the loss on a depreciating car. Wealthy individuals use debt strategically to build assets, not to fund consumption.

5. Building Wealth vs. Looking Wealthy

A common pitfall is prioritizing the appearance of wealth over actual wealth. Spending money on luxury items, expensive cars, or designer clothes to impress others, especially when funded by debt, creates a facade. True wealth is built quietly and authentically. Many financially successful individuals live below their means, drive reliable paid-off cars, and invest the difference. Their wealth is reflected on their balance sheet, not just their outward appearance. Focusing on proving wealth often leads to a performance, not genuine financial freedom. The goal should be to build assets that provide security and options, not to impress others with possessions.

The Path to Wealth: Behavior Over Intellect

Ultimately, becoming wealthy is less about intelligence and more about consistent behavior and habits. By shifting focus from chasing income to acquiring assets, performing necessary financial calculations, prioritizing investments, using debt wisely, and building real wealth instead of merely appearing wealthy, individuals can change their financial trajectory. These are not complex strategies but rather different habits from the norm. Committing to these behaviors allows compounding to work its magic over time, leading to genuine financial freedom and security.

Source: Why Most People Stay Broke (YouTube)

Related Articles

First $10K Ignites $400K Growth in 30 Years

Starting with just $10,000 and saving $200 monthly can grow to over $400,000 in 30 years, thanks to compound interest. This highlights the critical importance of early investment and consistent saving for long-term wealth building.

5 Wealth Killers Drain Billions Annually

High-interest debt, lifestyle creep, overspending on housing, delayed investing, and get-rich-quick schemes are costing Americans billions. Experts outline strategies to avoid these five major wealth killers and build lasting financial security.

Passive Income Fuels Wealth: Real Estate’s Role

Building wealth requires making money work for you, often through passive income. Real estate offers a proven path to generating this income via rental properties. Understanding key terms and market dynamics is crucial for success.