Housing Market Freeze: Why Sales Are Down, Not Crashing

Contrary to alarming headlines, the housing market is experiencing a slowdown in sales, not a crash. This is primarily due to low inventory levels and a significant number of homeowners locked into historically low mortgage rates, creating a 'rate lock-in' effect that discourages selling and moving.

Housing Market Freeze: Why Sales Are Down, Not Crashing

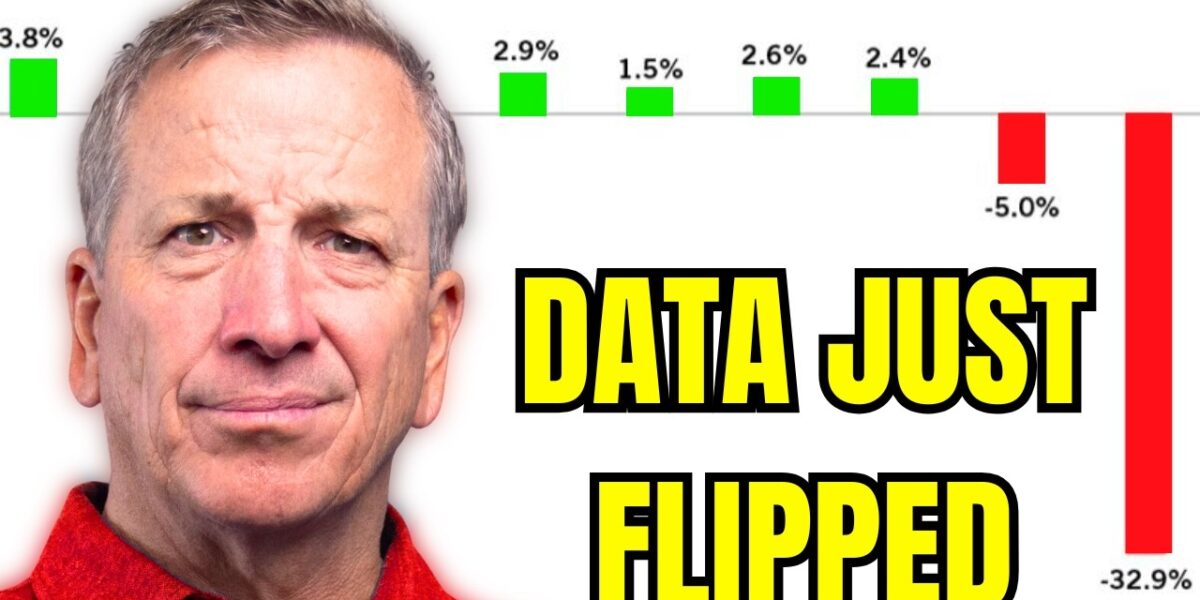

Headlines are abuzz with reports of a housing market freeze and the lowest sales in years. However, a closer examination of the data reveals a market characterized by low inventory and homeowners locked into historically low mortgage rates, rather than an impending crash. Experts suggest that focusing solely on transaction volume misses the broader picture, which is far more nuanced than a simple market correction.

Inventory Remains Historically Low

A key factor distinguishing the current market from previous downturns, such as the 2008 crisis, is the persistent shortage of housing supply. In 2008, the market was flooded with approximately 4 million homes on the Multiple Listing Service (MLS).

In stark contrast, the current MLS inventory has hovered around 1 million listings, significantly lower than pre-pandemic norms. The period between 2012 and 2022 saw the creation of nearly 16 million new households, yet only 8 million new homes were built, creating a substantial deficit.

While some regions may be experiencing a slight increase in inventory compared to 2019 levels, national figures remain historically low. This undersupply is a fundamental economic principle that counters the narrative of a market collapse.

High inventory levels, as seen in 2008, create buyer’s markets with abundant choices, driving prices down. Conversely, low inventory supports price stability, even if sales volume decreases.

The ‘Rate Lock-In’ Effect

A significant driver of the current market dynamic is the phenomenon known as the ‘rate lock-in.’ The vast majority of homeowners have mortgage rates well below current market rates, with a substantial portion locked in at under 3%. With current rates in the mid-6% range, homeowners face a significant financial disincentive to sell and move. Upgrading or even making a lateral move would mean taking on a new mortgage at a substantially higher interest rate, significantly increasing monthly payments.

This ‘trapped equity’ is estimated to be in the tens of trillions of dollars nationwide. For a crash to occur, a significant increase in distressed sellers would be necessary, a scenario that does not align with current data.

In 2008, approximately 30% of sellers were distressed, often due to adjustable-rate mortgages and little to no down payments, forcing them to sell regardless of price. Today, distressed sellers represent a mere 2% of the market, a figure within the normal range.

Seller Equity and Confidence

Unlike in 2008, when many homeowners were underwater on their mortgages, today’s sellers are largely in a strong equity position. This equity provides a financial cushion, allowing them to weather economic uncertainties or hold out for favorable sale prices. The concept of being ‘underwater’ means owing more on a mortgage than the home is worth, a situation few homeowners currently face.

The lack of seller distress is a critical factor. Sellers who are not compelled to sell will not accept significantly lower prices.

While some markets, like Austin, Texas, and Tampa, Florida, have seen price reductions, this is often a correction in markets that experienced rapid, unsustainable price run-ups. Many other areas, particularly in the Midwest, have not seen such dramatic increases and are unlikely to experience significant price drops.

Affordability and Interest Rates

While headlines often blame high mortgage rates for the affordability crisis, the impact is often overstated. A full percentage point drop in interest rates on a $500,000 home would only reduce the monthly payment by approximately $250.

Historically, current rates are not exceptionally high; they are closer to the long-term average. Experts do not anticipate rates returning to the historic lows seen in the recent past.

For buyers, the strategy may involve locking in a rate that makes sense now and refinancing later if rates decrease. However, homeowners with sub-4% rates are unlikely to move unless absolutely necessary, as even refinancing often leads to higher payments compared to their current situation. This reluctance to move, coupled with the desire to maintain low payments, keeps inventory low.

The Job Market’s Subtle Influence

Beyond housing-specific metrics, the broader economic landscape, particularly the job market, plays a key role. While overall unemployment remains relatively low, there are subtle indicators of potential shifts.

Excluding the healthcare sector, job growth in other areas has been stagnant or even negative. The increasing adoption of AI and automation may lead to greater efficiencies within businesses, potentially reducing the need for human labor in certain sectors.

However, significant job losses, coupled with a lack of government intervention, would be required to create the kind of seller distress that triggers a major market correction. Given the government’s historical tendency to intervene during economic downturns, a repeat of the 2008 scenario appears unlikely. The current market is more characterized by a slowdown in transaction volume rather than a fundamental collapse in property values.

Regional Variations and Investor Considerations

The housing market is not monolithic. While national trends suggest stability, specific regions may experience localized corrections due to factors like overbuilding or economic shifts.

Investors looking at the current market should consider the implications of low inventory and high rates on cash flow for rental properties. Some investors may be forced to sell if their properties are no longer cash-flowing, but this is not indicative of a widespread market collapse.

For homeowners, the current environment highlights the benefit of having locked in low-interest rates. While moving may be financially challenging, options like renting out a current home to offset costs while renting elsewhere are becoming more common. The market is currently defined by homeowners choosing to stay put due to favorable financing, leading to fewer transactions but not necessarily a decline in home values.

Source: WTF Is Happening To The Housing Market?! (YouTube)

Related Articles

Median Home Price Now Out of Reach for Median Income

The median home price in the U.S. has now surpassed what the median household income can afford, creating a significant barrier to homeownership. Analysis shows a required salary of over $112,000 for the median home price, far exceeding the median income of $84,000. This affordability gap challenges the traditional dream of owning a home for many Americans.

Buy Below Median for Safer Investment Returns

Buying investment properties above the median home price carries significant risk of financial loss, even at a discount. Smart investors focus on lower-priced homes to ensure positive cash flow and insulate themselves from market downturns.

AI Spots Top 5 Housing Markets for Investors

Artificial intelligence identifies top real estate investment markets like Charlotte, Dallas-Fort Worth, Raleigh-Durham, Columbus, and Indianapolis. While AI highlights growth, experts caution that appreciation may slow, and finding cash flow requires careful analysis, especially in competitive markets.