Housing Market Cools: Prices Dip as Rates Climb

The U.S. housing market is cooling significantly, with prices falling for the first time in nearly 20 years. Rising mortgage rates, increased inventory, and affordability issues are driving down demand, while regional markets show mixed performance. Experts suggest a normalization after years of excess, emphasizing long-term fundamentals for investors.

Housing Market Cools as Prices Dip Amidst Rising Rates

The U.S. housing market is experiencing a significant downturn, with prices falling for the first time in nearly two decades. Data shows that 47 out of the top 50 cities are seeing weaker market conditions. Listing prices are now lower than they were at the start of the year, and searches for terms like “can’t sell a house” and “help with mortgage” have hit record highs. Home sellers now outnumber home buyers by over 600,000, and homes are taking the longest to sell in more than a decade as mortgage rates climb.

Interest Rates Drive Down Demand

Higher interest rates are a primary driver of the current housing market slowdown. As mortgage rates rise, a 1% increase can reduce a buyer’s purchasing power by 10%. For example, a $500,000 home at a 6% mortgage rate has the same affordability as a $450,000 home at 7%. This directly impacts how much buyers can afford, leading to decreased demand. This year, mortgage rates have climbed back to their highest levels in three months. As a result, 37% of home builders are cutting prices by an average of 6%.

Regional Market Divergence

While the overall market is cooling, some areas are impacted more than others. Cities like Miami and Austin are experiencing significant drops in demand, with Miami seeing 197% more sellers than buyers and Austin down 5.9% recently. These were some of the hottest markets during the pandemic, leading to increased construction and a subsequent oversupply when migration slowed and affordability worsened. Conversely, more affordable markets like Milwaukee and parts of the Northeast are still seeing price growth due to higher demand relative to supply. Milwaukee, for instance, has seen prices rise 10% year-over-year.

Inflation and Construction Costs Add Pressure

Inflation and rising construction costs are further complicating the housing market. Higher oil prices, for example, can indirectly push up mortgage rates as investors demand higher returns on bonds. Additionally, the cost of building materials has surged, with aluminum up 39% and steel up 20% over the past year. These increased costs are passed on to buyers, further reducing affordability. Even when headline home prices show modest increases, when adjusted for inflation, many homes have actually lost purchasing power.

Affordability Crisis Deepens

The combination of high home prices and rising mortgage rates has created an affordability crisis. For a median-priced home of $398,000 with a 6.25% mortgage rate and 20% down payment, the monthly payment is around $1,954 before taxes and insurance. To qualify for this payment, a household needs to earn approximately $106,000 annually, leaving the average American family significantly short. A mere 0.25% increase in mortgage rates could price an additional 1.4 million potential buyers out of the market.

Potential Solutions and Their Limitations

Several proposals aim to address the housing affordability issue. One idea is a $200 billion mortgage buyout program, intended to lower mortgage rates. While it caused a temporary dip of about 0.2% in rates, its impact is minimal on the overall mortgage market and it’s a one-time injection. Banning institutional investors from buying single-family homes is another suggestion, but these investors make up less than 1% of the market, so their removal would have little effect. Portable mortgages, allowing homeowners to transfer their existing low-rate mortgages to a new home, could unlock inventory but face resistance from banks holding low-rate loans. Developing affordable housing on federal land is a long-term prospect that could take 5-10 years to materialize.

What Investors Should Know

While a widespread housing crash is unlikely due to high seller equity, the era of easy money in real estate is over. Buyers need to conduct thorough research, focus on location, and carefully assess prices and long-term costs. Builders are offering incentives, sometimes up to 14%, which could present opportunities for those with a long-term outlook. For those not buying, renting, saving the difference, and investing in index funds is a viable strategy as the market normalizes. The current market, while showing signs of slowing, represents a normalization after years of excess, emphasizing the importance of focusing on fundamentals and long-term prospects rather than short-term hype.

Condominiums Face Unique Challenges

Condominiums are currently facing particularly harsh conditions. There are 83% more condos listed than buyers, and HOA fees and insurance costs are skyrocketing, especially in Florida where average premiums are nearly $3,200 annually. Because condos typically don’t appreciate as quickly as single-family homes, they are often the first to feel the impact when the market turns.

Market Forecasts Vary

Predictions for the remainder of the year vary. Redfin anticipates a 1% increase in home prices, while the National Association of Realtors expects a 4% gain. Zillow has revised its forecast to a 0.7% increase, and J.P. Morgan predicts zero appreciation. When accounting for inflation, most of these forecasts suggest negative real returns for housing prices this year.

Source: WTF Just Happened To The Housing Market?! (YouTube)

Related Articles

Markets Wobble as Geopolitics Shift Dramatically

Global markets are showing volatility as geopolitical tensions rise, with the Nasdaq nearing correction territory. Concerns over consumer spending, rising costs, and the nation's fiscal health are intensifying. Analysts debate whether current events represent short-term market noise or a fundamental "reinvention of geopolitics" with long-term implications.

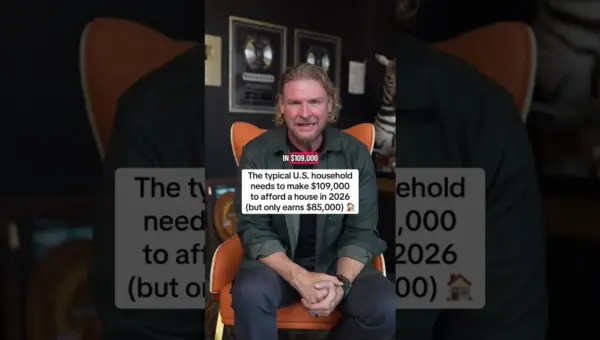

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.

Global Shortages Hit Helium, Fertilizers Amid War

Global shortages are expanding beyond oil and gas, now impacting critical materials like helium and fertilizers. These supply disruptions threaten tech manufacturing and food production, raising concerns about inflation and economic growth. The situation signals a widening global supply shock with significant market implications.