Homeowners Stuck as Sales Hit 40-Year Low

The U.S. housing market is seeing its slowest sales pace in over 40 years, with only 4.7% of homeowners selling between 2023-2025. High prices and the "lock-in effect" of low mortgage rates are preventing both buyers and sellers from transacting. This slowdown impacts affordability, particularly for first-time buyers, and creates regional variations in market activity.

Homeowners Stuck as Sales Hit 40-Year Low

The U.S. housing market is experiencing a rare event, with home sales turnover dropping to its lowest point in over 40 years. From 2023 to 2025, only about 4.7% of existing homeowners sold their properties. This marks a significant slowdown, with buyer demand hitting record lows, according to data from Redfin. Homebuyers are largely staying on the sidelines because prices have become too high for many to afford.

The average sale price for an existing home in the U.S. reached $410,000 by the end of 2025. This price is more than double what it was just a decade ago. As a result, pending home sales and contract signings have sharply declined. Many homeowners find themselves in a difficult position, often referred to as being “stuck.” They are hesitant to sell because doing so would mean giving up their current, low mortgage interest rates.

The ‘Lock-In’ Effect Squeezes Market

This situation is largely driven by what experts call the “lock-in effect.” When homeowners secured mortgages at historically low interest rates in recent years, they are now reluctant to sell and buy a new home at current, much higher rates. Imagine having a great deal on a car loan; you wouldn’t want to trade it in for a new car with a much higher interest rate, would you? This is the same principle at play in the housing market.

For buyers, the high prices combined with elevated mortgage rates present a significant affordability challenge. Many potential buyers simply cannot qualify for a loan large enough to purchase a home at current market values, or they are priced out of the market altogether. This imbalance between sellers who are unwilling to give up low rates and buyers who cannot afford current prices has led to a significant drop in overall market activity.

Broader Economic Influences

Several economic factors are contributing to this market dynamic. Inflationary pressures and the Federal Reserve’s subsequent interest rate hikes have made borrowing money more expensive. While the Fed’s actions aim to control inflation, they have had a direct impact on mortgage rates, pushing them higher. This has cooled demand and made it harder for buyers to enter the market.

The low inventory of homes for sale is also a key factor. When fewer people are selling, there are fewer homes available for potential buyers. This scarcity can help keep prices elevated, even as demand softens. It creates a challenging environment where both buyers and sellers face unique obstacles.

Regional Differences and Who is Affected

The impact of this market slowdown is not uniform across the country. Areas that experienced the most significant price appreciation in recent years may see more pronounced effects. Buyers in these high-cost regions face the steepest affordability hurdles. Conversely, sellers in areas with less extreme price growth might find it easier to find a buyer, though they still face the challenge of their own mortgage rates.

This market dynamic primarily affects first-time homebuyers, who are often most sensitive to price and interest rate increases. It also impacts homeowners looking to move up or downsize, as they are caught in the lock-in effect. Real estate investors may also find opportunities limited due to lower transaction volumes and potentially higher financing costs.

Looking Ahead

The current housing market presents a complex puzzle. High prices, elevated mortgage rates, and the strong desire of existing homeowners to keep their low-rate loans have created a stalemate. While this situation is unusual, market conditions can change. Factors like future interest rate movements, new construction levels, and broader economic shifts will all play a role in shaping the housing market’s path forward.

Source: This hasn't happened since 1982… (YouTube)

Related Articles

Denver Housing Market Faces Steep Drop

Denver's housing market is facing a significant downturn, with home sales at a 10-year low and inventory surging. Rising prices have eroded affordability, prompting an exodus of residents. Experts predict further price drops, marking a potential major correction for the city.

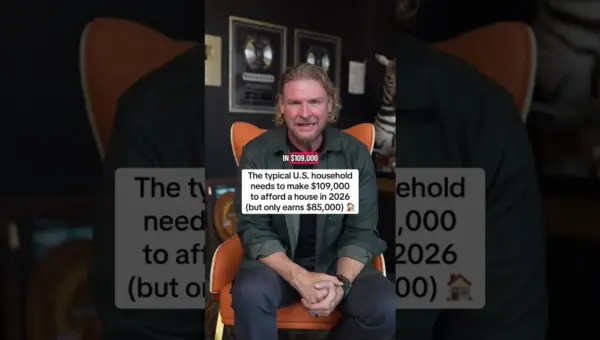

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.

Builders Cut Prices as New Home Sales Plummet

Home builders are facing their worst sales slump in 13 years, leading to aggressive price cuts and a surge in unsold inventory. This trend, mirroring the 2008 crisis, suggests a significant market correction is underway. The mortgage rate lock-in effect is currently propping up the existing home market, but future pressures may bring more inventory and negotiation opportunities for buyers.