House Hacking Fuels Multi-Home Ownership

House hacking, a strategy where homeowners live in one unit of a multi-unit property and rent out the others, is proving to be an effective way to acquire multiple homes with minimal initial capital. This method allows for mortgage payments to be offset by rental income, building equity and a track record for future investments.

House Hacking Fuels Multi-Home Ownership

Many people dream of owning multiple homes, but the high cost of real estate seems like a major roadblock. However, a strategy known as house hacking can make this dream a reality, even with limited funds. This approach allows individuals to purchase a property, live in one unit, and rent out the others to cover their mortgage payment. It’s a powerful way to build wealth and expand your real estate portfolio over time.

One investor shared how they acquired their first three homes using just $3,300 through house hacking. The key was using the equity built in one property to help finance the next purchase. This strategy shows that with smart planning, you don’t need a huge down payment to get started. It’s about using the property itself as a tool for further investment.

Building a Track Record

When this investor first started sharing their plans with friends and family, they faced skepticism. Many thought it was a foolish idea because they had no prior experience buying investment properties. This lack of a proven history made others doubt their capabilities, seeing them as unrealistic.

However, success breeds confidence, both for the investor and for those watching. The second property purchase, which also proved successful, began to shift perceptions. While some might have attributed the first success to luck, the second validated the strategy. When the third property was acquired and also succeeded, the doubt transformed into interest and even envy.

This experience highlights the importance of a track record in real estate. As you successfully manage properties and build equity, lenders and even your social circle begin to see you as a capable investor. This growing reputation can open doors to better financing options and more opportunities. Fear of Missing Out, or FOMO, becomes a powerful motivator for others to explore similar paths.

Understanding Key Real Estate Terms

For those new to real estate investing, a few terms are essential. Equity is the difference between what your property is worth and how much you still owe on the mortgage. It’s like the ownership stake you have in your home.

House hacking involves buying a multi-unit property (like a duplex or triplex), living in one unit, and renting out the others. The rental income from the other units helps pay down your mortgage, making your own housing costs much lower. Sometimes, it can even cover the entire mortgage payment.

Cash flow refers to the money left over from rental income after paying all property expenses, such as mortgage payments, property taxes, insurance, and maintenance. Positive cash flow means you’re making money each month from the property. This is a key indicator of a profitable investment.

Loan-to-Value (LTV) is a ratio lenders use to assess risk. It compares the loan amount to the property’s appraised value. A lower LTV, meaning you borrow less compared to the property’s value, often means better loan terms and lower interest rates.

Cap Rate, or capitalization rate, is a measure of a property’s profitability. It’s calculated by dividing the net operating income (income after expenses but before mortgage payments) by the property’s market value. A higher cap rate generally indicates a potentially better return on investment.

Broader Economic Influences

The current economic climate significantly impacts the housing market. Interest rates, for instance, play a crucial role. When interest rates are low, borrowing money to buy a home or investment property becomes cheaper, encouraging more purchases. Conversely, higher interest rates increase the cost of borrowing, which can slow down the market and reduce demand.

Inflation also plays a part. Rising costs for goods and services can affect people’s ability to save for down payments or afford higher monthly mortgage payments. For investors, inflation can also increase property operating costs, impacting cash flow.

Inventory levels—the number of homes available for sale—are another critical factor. Low inventory often leads to bidding wars and rising prices, benefiting sellers. High inventory can give buyers more choices and negotiating power, potentially stabilizing or lowering prices.

Regional Variations and Who Benefits

The impact of these market dynamics varies greatly by region. In high-cost urban areas, house hacking can be particularly attractive because rental income can more easily offset expensive mortgages. However, finding suitable multi-unit properties might be more challenging and competitive.

In more affordable suburban or rural areas, the initial investment might be lower, making it easier for first-time buyers to enter the market. The rental demand and potential cash flow, however, might differ based on local economic conditions and population density.

Buyers looking to enter the market can benefit from house hacking by reducing their personal living expenses. Sellers might find continued demand, especially for properties suitable for house hacking, if inventory remains tight in their area. Investors can use this strategy to scale their portfolios more efficiently, turning one property into a stepping stone for multiple acquisitions.

Ultimately, house hacking offers a practical pathway to homeownership and wealth building. By understanding the strategy, the key financial terms, and the broader economic context, more individuals can explore how to make it work for them.

Source: How We Bought 3 Homes with Just $3,300 Using House Hacking (YouTube)

Related Articles

Couple Balances Separate Finances, Builds Joint Wealth

Nathan and Crissi are navigating a complex financial landscape with separate accounts, newborn twins, and a new business. Their unique approach to wealth building involves adapting the Financial Order of Operations to align individual financial habits with shared goals for independence.

Buy, Live, Rent: Your Path to Real Estate Wealth

Discover a real estate strategy where you buy a home, live in it, and have tenants pay your mortgage. Learn how instant equity, rental income, and strategic partnerships can turn a small investment into significant wealth.

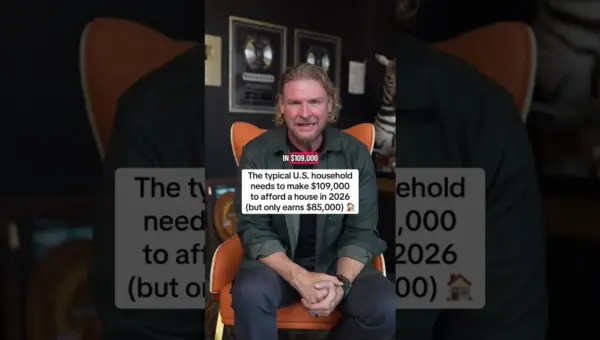

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.