First-Time Buyers Surge: 34% Share Hits 5-Year High

First-time homebuyers are making a significant comeback, reaching a 34% share of the market in February, the highest in five years. This surge coincides with modest affordability improvements and government efforts to cut housing regulations, though persistent supply shortages and rising interest rates continue to challenge the market.

First-Time Buyers Surge: 34% Share Hits 5-Year High Amid Modest Market Improvements

The U.S. housing market is exhibiting tentative signs of improvement for buyers, with first-time homebuyers reaching their highest share in five years. In February, this crucial demographic accounted for 34% of all purchasers, signaling a notable shift in market dynamics. This uptick occurs as affordability shows modest gains for the first time in three years, allowing immediate income households to once again afford a median-priced home. However, persistent challenges, including limited housing supply and rising interest rates, continue to temper a more robust rebound.

Government Efforts to Ease Regulatory Hurdles

In an effort to stimulate housing construction and improve affordability, the federal government has been actively working to cut red tape. These initiatives include reducing regulations that can slow down the permitting process for new homes. Specific measures involve lessening the impact of green construction requirements and streamlining historic preservation reviews. Experts acknowledge these federal efforts as progress, noting that while not the sole solution to the nation’s housing woes, they contribute to making it easier to build in the United States.

The administration’s focus extends to encouraging smaller banks to underwrite housing loans, aiming to broaden access to financing. By addressing federal regulations, the government seeks to remove barriers that have historically hindered new development and contributed to the ongoing housing shortage.

Market Metrics Show Mixed Signals

While first-time buyers are showing increased activity, the broader market presents a complex picture. Home prices saw only a slight increase of three-tenths of a percent in February, a stark contrast to the rapid appreciation seen in previous years. Furthermore, the time homes spend on the market is lengthening, a trend generally favorable to buyers as it indicates less intense competition.

The median existing home price experienced its smallest increase in 16 years, a development that could further bolster affordability. However, this positive trend is counterbalanced by rising interest rates. Rates, which dipped below 6% earlier in the year, have since moved higher, posing a significant challenge for prospective homeowners, particularly those relying on financing.

The Persistent Housing Shortage

A critical factor constraining a stronger market recovery is the persistent shortage of housing inventory. Estimates suggest the nation faces a deficit of approximately 4 million homes, with some analyses placing the gap closer to 1.4 million units. This imbalance between supply and demand continues to exert upward pressure on prices and limit choices for buyers.

Regional disparities exist in housing supply. The Western United States, for instance, has the smallest gap between housing needs and available supply compared to other regions. This means buyers in some areas face more acute shortages than in others.

Opportunities Emerge in Smaller Cities

Despite the national challenges, buyers are finding opportunities in smaller cities, often referred to as “blue-collar cities” or “old-fashioned” towns. These locations may offer more accessible price points and greater availability of homes, presenting a viable alternative for those priced out of larger metropolitan areas.

Market Impact

The surge in first-time homebuyers to 34% of the market, the highest in five years, indicates that affordability, despite its fragility, is improving enough to draw in a significant segment of new entrants. This demographic is crucial for sustained market health, as they represent future homeowners and contribute to demand. The modest price appreciation and longer market times further support the notion of a cooling, more buyer-friendly environment, at least in terms of price growth and negotiation power.

However, the specter of rising interest rates remains a significant headwind. Even as prices stabilize and inventory slowly increases, higher borrowing costs can quickly erode purchasing power, potentially reversing some of the recent affordability gains. The deep-seated housing shortage of millions of units is a long-term structural issue that will continue to influence market dynamics for years to come, preventing a rapid or dramatic price decline.

What Investors Should Know

For real estate investors, the current market presents a mixed outlook. The increased activity from first-time homebuyers suggests continued underlying demand for housing. However, the supply constraints and rising interest rates require careful consideration. Investors focusing on markets with more affordable entry points, potentially in smaller cities or areas less affected by severe inventory shortages, may find opportunities.

The government’s efforts to reduce regulatory burdens on construction could, over the long term, lead to increased supply. Investors might monitor sectors related to homebuilding, construction materials, and financial services that support mortgage lending. The Federal Reserve’s monetary policy, particularly regarding interest rates, will remain a critical factor influencing both buyer demand and investor returns. While the immediate data suggests a more balanced market, the structural deficit in housing supply and potential shifts in interest rates warrant a cautious and strategic approach.

Source: BUYER SURGE: First-time homebuyers hit HIGHEST share in years (YouTube)

Related Articles

Iran Talks Gain 10 Days, But Markets Remain Skeptical

Iran has secured a 10-day extension for negotiations, but financial markets remain unconvinced, showing little reaction to the news. Rising energy and borrowing costs, coupled with geopolitical tensions, continue to pressure global markets and consumer spending.

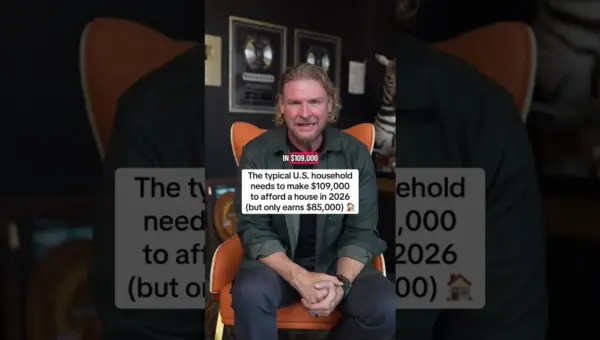

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.

Rate Hike Fears Spark Market Sell-Off, Geopolitics Add Fuel

Markets are reeling as a surprising shift in Federal Reserve expectations, with rate hikes now being priced in, combines with escalating Middle East tensions. This has triggered a liquidity crunch across assets, impacting everything from stocks to bonds and gold.