Interest Rates Surge, Squeezing Home Affordability

Rising interest rates have dramatically increased monthly mortgage costs, reducing home affordability nationwide. This shift impacts buyers, sellers, and investors, demanding a closer look at market dynamics and investment strategies.

Interest Rates Surge, Squeezing Home Affordability

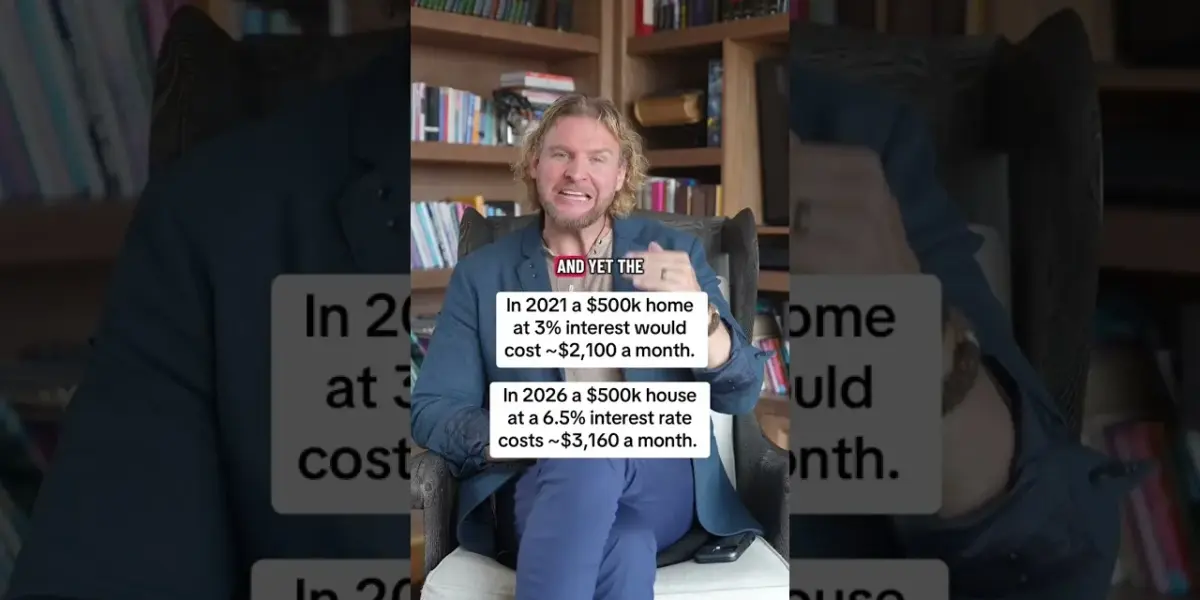

The landscape of homeownership has dramatically shifted, with rising interest rates significantly impacting monthly costs for prospective buyers. In 2021, a homeowner purchasing a $500,000 property with a 3% interest rate would have faced a monthly mortgage payment of approximately $2,100. Fast forward to today, and that same $500,000 home, assuming current market rates hover around 6.5%, would command a monthly payment of roughly $3,160. This represents a staggering increase of over $1,000 per month, a change driven solely by the cost of borrowing, not by any appreciation in the property’s value itself.

Affordability Crisis Deepens

This substantial decline in affordability has far-reaching consequences for the housing market. When the cost of owning a home becomes prohibitive for a larger segment of the population, the pool of eligible and willing buyers shrinks. This reduced competition among buyers can lead to a cooling of demand, prompting sellers to reconsider their pricing strategies and potentially adjust their expectations. Furthermore, home builders, facing slower sales, are increasingly likely to offer incentives to attract and secure new buyers, signaling a shift in market power.

Investor Perspective: Navigating the New Normal

For real estate investors, understanding these dynamics is crucial. The surge in interest rates fundamentally alters the calculus for property acquisition and management. Investors who are adept at analyzing how changes in interest rates reshape purchasing power and market competition are better positioned to identify opportunities and mitigate risks.

Understanding Key Investment Metrics

Several core real estate investment concepts become particularly relevant in a rising rate environment:

- Cash Flow: This refers to the net income generated from a rental property after all operating expenses (including mortgage payments, property taxes, insurance, and maintenance) are paid. In a market with higher interest rates, achieving positive cash flow becomes more challenging as mortgage expenses increase. Investors must carefully project and ensure that rental income adequately covers these higher costs.

- Capitalization Rate (Cap Rate): The cap rate is a measure of a property’s profitability, calculated by dividing the net operating income (NOI) by the property’s market value. A higher cap rate generally indicates a more attractive investment. With increased borrowing costs, the NOI can be compressed, potentially leading to lower cap rates unless property values adjust downwards significantly or rents rise substantially.

- Loan-to-Value (LTV) Ratio: This ratio compares the amount of a loan to the value of the asset purchased. Lenders use LTV to assess risk. In a market with higher interest rates, securing favorable LTV ratios might become more difficult, potentially requiring larger down payments from investors.

Broader Economic Influences

The current housing market is not operating in a vacuum. Broader economic factors, such as inflation and monetary policy, play a significant role. Central banks often raise interest rates to combat inflation. While this aims to stabilize the overall economy, it directly increases the cost of borrowing for mortgages, cars, and other significant purchases. This can lead to a general slowdown in consumer spending and investment, including in the real estate sector.

Regional Variations and Impact

The impact of rising interest rates is not uniform across the country. Regions that were previously experiencing rapid price appreciation and were already at the edge of affordability for many residents are likely to feel the pinch more acutely. Buyers in these markets may find their purchasing power significantly curtailed, potentially leading to a more pronounced slowdown or even price corrections. Conversely, more affordable markets might see a relative stabilization, as they were less susceptible to the extreme price run-ups and may remain within reach for a broader base of buyers. Sellers in highly competitive, expensive markets may need to be more flexible on price and terms, while those in more balanced or affordable regions might experience less pressure.

Investors will need to conduct granular analysis, understanding that local market conditions, job growth, and supply-demand dynamics will interact with the overarching trend of higher interest rates. The ability to adapt strategies, whether focusing on cash flow preservation, identifying undervalued assets, or exploring different property types, will be key to navigating this evolving real estate environment.

Source: The Housing Market Explained (YouTube)

Related Articles

Iran Talks Gain 10 Days, But Markets Remain Skeptical

Iran has secured a 10-day extension for negotiations, but financial markets remain unconvinced, showing little reaction to the news. Rising energy and borrowing costs, coupled with geopolitical tensions, continue to pressure global markets and consumer spending.

Home Affordability Crisis: Buyers Demand Falls

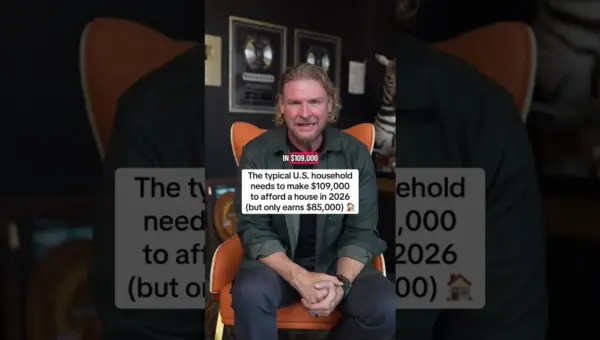

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.

Rate Hike Fears Spark Market Sell-Off, Geopolitics Add Fuel

Markets are reeling as a surprising shift in Federal Reserve expectations, with rate hikes now being priced in, combines with escalating Middle East tensions. This has triggered a liquidity crunch across assets, impacting everything from stocks to bonds and gold.