Housing Market Shifts: Navigating the New Normal

The housing market's resilience is tested by fluctuating interest rates, but a 2008-style crash remains unlikely due to stronger foundations. Understanding market cycles and key financial metrics is crucial for navigating current opportunities.

Housing Market Shifts: Navigating the New Normal

The question on many minds: is a repeat of the 2008 housing crisis on the horizon? While the specter of a major downturn often surfaces, the current real estate landscape presents a fundamentally different picture than the one that led to the 2008 collapse. Understanding these differences, alongside the impact of fluctuating interest rates and evolving buyer behavior, is crucial for homeowners and investors alike.

Lessons from 2008: A Fragile Foundation

The 2008 housing crisis was a product of a market built on shaky ground. Predatory lending practices were rampant, with notoriously lenient standards that allowed individuals to secure mortgages they couldn’t truly afford. ‘Heartbeat loans’ and widespread adjustable-rate mortgages (ARMs) meant that a significant portion of homeowners were exposed to rising interest rates, leading to mass defaults and foreclosures when property values began to decline.

Today’s Market: Stronger Foundations and Shifting Dynamics

The structure of the housing market today is vastly different. A substantial majority of homeowners are currently benefiting from fixed-rate mortgages, many secured at historically low interest rates. This provides a significant buffer against rising rates and has contributed to a substantial increase in homeowner equity. Unlike the subprime lending of the past, current lending standards are generally more stringent, reducing the risk of widespread defaults due to unaffordable loan payments.

Interest Rates: The Primary Driver of Demand

While the lending environment has improved, interest rates are now playing a far more significant role in shaping buyer demand than the lending practices of the past. When mortgage rates fall, we often see a swift re-entry of buyers into the market, eager to capitalize on lower borrowing costs. Conversely, when interest rates remain elevated, demand typically cools, and the available inventory of homes for sale begins to climb. This ebb and flow of demand and supply creates distinct opportunities and challenges for different market participants.

Investor Strategies in a Cyclical Market

Savvy real estate investors understand that markets are inherently cyclical, moving through periods of expansion, slowdown, and recovery. The current environment, characterized by fluctuating interest rates and shifting demand, presents a prime example of this dynamism. Investors who are prepared for both scenarios – periods of high demand and periods of slower activity – are best positioned for success.

This preparation involves meticulous analysis of deals, focusing on key financial metrics such as capitalization rates (cap rates), loan-to-value ratios (LTV), and projected cash flow. Cap rates, for instance, represent the annual return on investment for a property based on its net operating income. A higher cap rate generally indicates a more profitable investment. LTV, or loan-to-value ratio, is the percentage of a property’s value that is financed by a loan. Lower LTVs typically signify less risk. Cash flow is the net income generated by a property after all expenses, including mortgage payments, property taxes, and maintenance, are paid. Positive cash flow is essential for sustainable real estate investment.

Regional Variations and Who is Most Impacted

The impact of these market shifts is not uniform across the country. Regions that experienced rapid price appreciation during periods of low interest rates may see a more pronounced slowdown as rates rise. Buyers in these areas might face higher monthly payments, potentially reducing their purchasing power. Conversely, markets with more stable price growth and lower inventory levels might remain more resilient.

Sellers in areas with high demand and low inventory may still command strong prices, though they may need to adjust expectations compared to the peak of the market. For buyers, elevated rates can make affordability a significant hurdle, but a rise in inventory could offer more choices and negotiation power. Investors need to conduct thorough due diligence, focusing on local market conditions, economic drivers, and the specific financial viability of each potential acquisition.

Looking Ahead: Preparedness is Key

While a 2008-style crash appears unlikely due to a more stable market foundation and responsible lending, the real estate market will continue to evolve. Interest rate fluctuations, economic conditions, and demographic shifts will all play a role. The most successful approach for homeowners and investors is one of continuous learning and strategic adaptation, preparing for the inevitable cycles of the market rather than predicting catastrophic events.

Source: Is there another 2008 housing crash inevitably coming our way? 📉 🏠 (YouTube)

Related Articles

Iran Talks Gain 10 Days, But Markets Remain Skeptical

Iran has secured a 10-day extension for negotiations, but financial markets remain unconvinced, showing little reaction to the news. Rising energy and borrowing costs, coupled with geopolitical tensions, continue to pressure global markets and consumer spending.

Buy, Live, Rent: Your Path to Real Estate Wealth

Discover a real estate strategy where you buy a home, live in it, and have tenants pay your mortgage. Learn how instant equity, rental income, and strategic partnerships can turn a small investment into significant wealth.

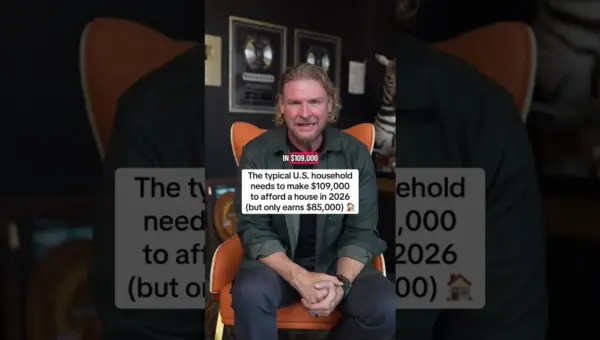

Home Affordability Crisis: Buyers Demand Falls

The typical American household needs $109,000 to afford a home, but only earns $85,000, creating a major affordability crisis. This demand slowdown echoes past market downturns and presents challenges for buyers and opportunities for investors.