Car Payments Surging Past Savings: A Financial Wake-Up Call

More than one in five new car shoppers in Q4 2025 committed to monthly payments of $1,000+, a trend that may be outpacing consumer savings. This financial imbalance raises concerns about consumer debt and long-term wealth-building.

New Car Affordability Crisis: Monthly Payments Eclipse Savings for Many

A stark financial reality is emerging for American car buyers, with a growing number of consumers committing to monthly payments that significantly outpace their savings. Data from Edmonds reveals a concerning trend in the fourth quarter of 2025, where more than one in every five new car shoppers agreed to monthly payments of $1,000 or more. This figure, described as “insane” by market observers, highlights a potential misalignment in financial priorities, where the pursuit of new vehicles is overshadowing fundamental savings goals.

The $1,000 Car Payment Threshold: A Sign of Financial Strain

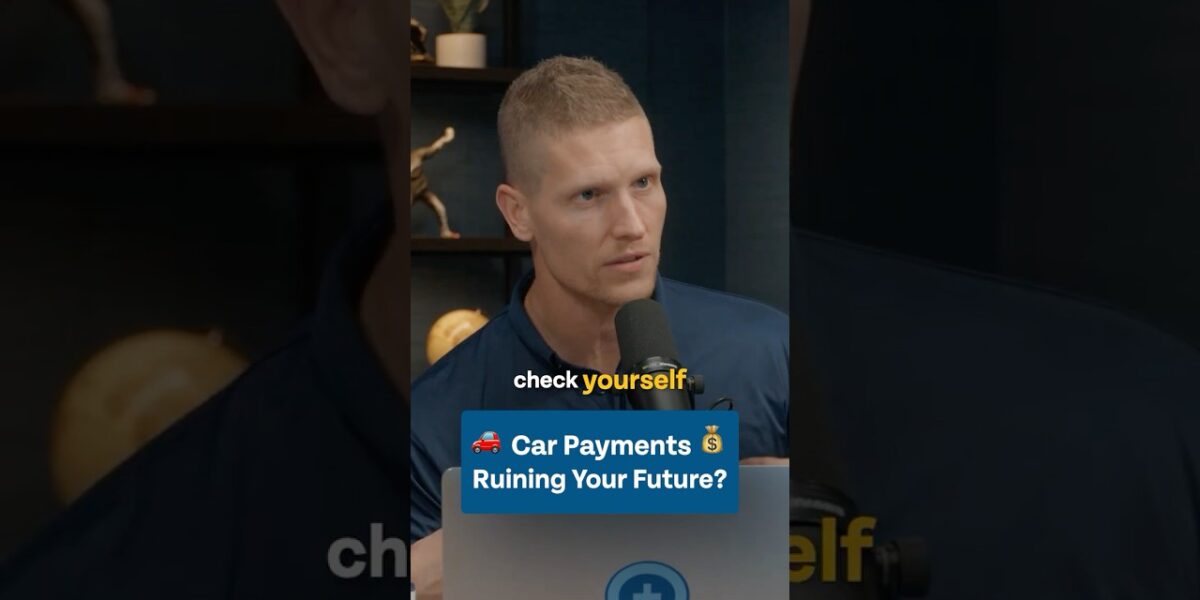

The benchmark of a $1,000 monthly car payment has become a significant indicator of financial pressure. For a substantial segment of the market, this commitment is not only a large outgoing expense but also a critical point of comparison against their ability to save and invest. Financial experts emphasize a fundamental principle: an individual’s monthly savings—across all accounts, including Roth IRAs, 401(k)s, and taxable brokerage accounts—should ideally exceed their car payment. When this dynamic is reversed, it signals a potentially precarious financial order, where debt obligations are prioritized over wealth accumulation.

“You should always check yourself to make sure is the amount that I’m saving on a monthly basis, the amount that’s going into my Roth, that’s going into my 401k, that’s going into my taxable brokerage account, is that amount more than my car payment? And if it’s not, we would argue that you have things in the wrong order.”

Underlying Factors Driving Elevated Car Payments

Several macroeconomic factors have contributed to the surge in new car prices and, consequently, monthly payments. Persistent supply chain disruptions, elevated raw material costs, and strong consumer demand, fueled in part by pandemic-era savings and low interest rates (though this has shifted), have all played a role. While interest rates have risen significantly since their lows, the underlying demand for vehicles, coupled with the premium placed on new models, continues to push payment figures higher. The average transaction price for new vehicles has seen substantial increases over the past few years, directly translating into higher financing costs for consumers, especially for those opting for longer loan terms to keep monthly payments seemingly manageable.

Market Impact and Investor Considerations

The trend of high car payments has several implications for the broader market and individual investors:

- Consumer Spending: A significant portion of disposable income being allocated to car payments can reduce spending on other goods and services, potentially impacting sectors like retail, hospitality, and entertainment.

- Savings and Investment Rates: If savings are consistently falling short of car payments, it directly hinders the ability of consumers to build emergency funds, invest for retirement, or achieve other long-term financial goals. This can lead to a slower growth in investment portfolios and reduced capital available for market participation.

- Automotive Sector Dynamics: While manufacturers and dealerships may benefit from higher revenue per vehicle, the long-term sustainability of sales at these payment levels is questionable. It could lead to increased repossessions or a shift towards the used car market if affordability becomes a more pressing issue.

- Interest Rate Sensitivity: As interest rates remain elevated, the cost of financing these high-value vehicles increases, exacerbating the affordability challenge. This makes consumers more sensitive to further rate hikes and potentially more cautious about taking on new debt.

What Investors Should Know

For investors, this trend underscores the importance of consumer financial health as a key driver of economic activity. The ability of consumers to save and invest is directly linked to their capacity to weather economic downturns and contribute to market growth. Therefore, monitoring trends in consumer debt, savings rates, and major expenditure categories like automotive financing provides valuable insights into the overall economic landscape.

The current situation suggests a potential normalization or even contraction in demand for new, high-priced vehicles if economic conditions tighten further or if consumers become more financially constrained. This could present opportunities in sectors that cater to more budget-conscious consumers or in the used car market. Conversely, a sustained period of high car payments could indicate a segment of the population that is financially leveraged, making them more vulnerable to economic shocks.

Ultimately, the adage “Check yourself before you wreck yourself,” popularized on social media and echoed by financial commentators, serves as a crucial reminder for consumers. Prioritizing financial stability and ensuring that savings outpace major debt obligations like car payments is paramount for long-term financial well-being and for maintaining a healthy, sustainable economy.

Source: Before You Buy That Car, Check This First (YouTube)

Related Articles

Tax Gains Could Boost Wallets, Offset Gas Price Pain

New tax legislation aims to put more money directly into Americans' pockets, potentially offsetting concerns over rising gas prices. Proponents highlight that no one objects to having more personal income to spend as they see fit.

Millions Lack Emergency Savings: A Financial Health Check

Less than half of Americans can cover a $1,000 emergency from savings, a Bankrate survey found. Building an emergency fund of 3-6 months of living expenses is a key sign of financial health. This savings buffer protects against unexpected costs and supports long-term financial goals.

5 Signs You’re Winning With Money

Achieving financial success involves more than just a high income. Key indicators include having monthly financial margin, maintaining an emergency fund, investing consistently, controlling lifestyle spending, and experiencing financial peace of mind. A solid financial plan ties these elements together.