40% of Young Americans May Never Retire, Study Reveals

A concerning 40% of young Americans believe they will never retire, citing economic pressures like inflation and debt. This sentiment signals a potential shift in traditional retirement planning and highlights the urgent need for early financial literacy and savings strategies.

Young Americans Face Grim Retirement Outlook

A significant portion of young Americans are expressing deep skepticism about their ability to ever achieve traditional retirement, with a striking 40% indicating they expect to never retire. This stark figure, emerging from recent analyses, points to a growing chasm between financial aspirations and the perceived realities of economic security for younger generations. The sentiment suggests a fundamental shift in how millennials and Gen Z view their financial futures, potentially driven by a confluence of economic pressures and evolving lifestyle expectations.

Economic Headwinds and Shifting Priorities

The reasons behind this pessimism are multifaceted. Persistent inflation, stagnant wage growth relative to the cost of living, and the ever-increasing burden of student loan debt are significant factors. These economic realities make it exceedingly difficult for many young individuals to accumulate the substantial savings required for a comfortable retirement, which often necessitates tens of thousands, if not millions, of dollars depending on lifestyle and longevity.

Beyond these macroeconomic challenges, there’s also a discernible shift in cultural attitudes towards work and retirement. For some, the traditional model of working for 40 years and then ceasing all employment is becoming less appealing. Instead, there’s a growing interest in concepts like financial independence, early retirement (FIRE movement), or simply structuring one’s life to work in ways that are more fulfilling, even if it means not adhering to a strict retirement age.

“The traditional retirement model is being challenged. Young people are seeing the costs associated with a long retirement and questioning if it’s achievable or even desirable given other life goals.”

– Financial Analyst Observation

The Retirement Savings Gap

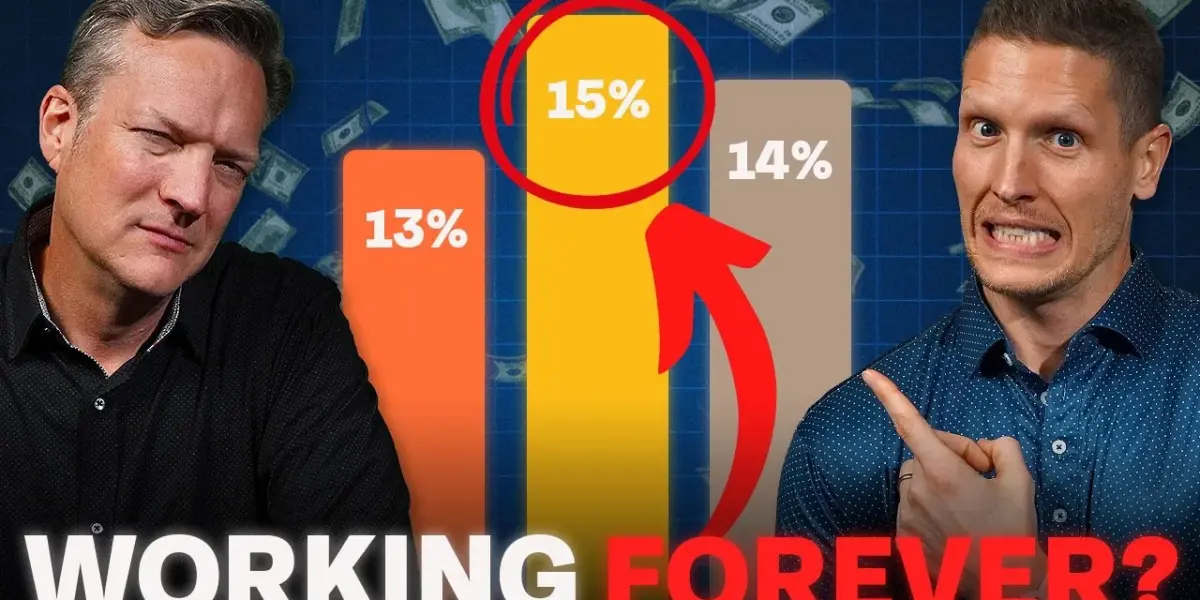

The sheer scale of retirement savings needed is a daunting prospect. Financial experts often recommend saving 15% of one’s income throughout their working lives to achieve a secure retirement. However, for many young Americans, competing financial priorities such as housing, education, and daily living expenses make it challenging to allocate such a significant portion of their income towards long-term savings.

The compounding power of early investment is a cornerstone of successful retirement planning. Yet, those starting late, or not saving consistently, miss out on crucial years of growth. This deficit can snowball, requiring much larger contributions later in life or leading to the realization that traditional retirement might be out of reach.

Sectoral and Index Performance Context

While the broader market, including indices like the S&P 500, has seen significant growth over the long term, this growth hasn’t always translated into accessible wealth for everyone. The increasing cost of assets, such as real estate and stocks, means that entry points are higher than ever. Furthermore, sectors that typically offer higher returns often come with higher volatility, making them less attractive to risk-averse individuals or those with limited capital to invest.

The narrative of “get rich quick” is often contrasted with the slow, steady accumulation required for retirement. However, the reality for many young Americans is that they are not seeing the kind of wealth creation necessary to bridge the gap between their current financial situation and their retirement goals. This is particularly true for those in lower-paying sectors or those whose careers have been impacted by economic downturns.

What Investors Should Know

The sentiment that 40% of young Americans may never retire is a wake-up call for individuals and a signal to financial institutions. For young people, it underscores the urgent need to prioritize financial literacy and start saving and investing as early as possible, even if it’s with small amounts. Understanding the power of compound interest and exploring diverse investment vehicles are crucial steps.

For older generations and policymakers, this trend highlights potential future challenges, such as a larger dependent population and a strain on social safety nets. It also suggests a potential increase in demand for financial advisory services and retirement planning tools tailored to individuals who may need to work longer or pursue alternative income streams in their later years.

Long-Term Implications

The long-term implications of this trend are profound. If a significant portion of the population doesn’t retire, it could lead to:

- A prolonged period of workforce participation, potentially impacting job markets and career progression for younger workers.

- Increased demand for flexible work arrangements and lifelong learning opportunities.

- Greater reliance on alternative income sources, such as part-time work, gig economy jobs, or personal businesses during what would traditionally be retirement years.

- Potential shifts in consumer spending patterns and economic growth models.

The expectation of never retiring is not necessarily a negative outlook for all. Some may embrace this as an opportunity to pursue passion projects or entrepreneurial ventures indefinitely. However, for the majority, it signals a significant concern about financial security and the ability to enjoy a period of rest and leisure after decades of work. Addressing the root causes of this sentiment—through improved financial education, economic policies that support wealth building, and accessible investment opportunities—will be critical for the financial well-being of future generations.

Source: X% of Young Americans Expect To NEVER Retire… (YouTube)

Related Articles

Odell’s $100M Warning: Shumpert’s Savings Secret Revealed

Odell Beckham Jr. warns that $100 million isn't a lifetime guarantee, highlighting the financial struggles many athletes face post-career. Iman Shumpert's early savings strategy is lauded as a key to financial longevity.

Melo’s $7.5K Dinner Bill: How Carmelo Anthony Taught Shumpert Financial Literacy

Iman Shumpert recounts how Carmelo Anthony taught him a valuable financial lesson by making him pay a $7,500 dinner bill, only to surprise him with $10,000 in cash the next day. The discussion also touches on NBA hazing, toughest players to guard, and media circus.

30-Somethings Overlook Key Tax Strategy

Financial experts highlight the critical importance for individuals in their 30s to strategically manage three distinct tax "buckets": tax-free, tax-deferred, and after-tax accounts. Overlooking this strategy can lead to missed opportunities for significant long-term tax savings.